Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Created by temporary differences between book accounting and tax accounting rules

Over 1.8 million professionals use CFI to learn accounting, financial analysis, modeling and more. Start with a free account to explore 20+ always-free courses and hundreds of finance templates and cheat sheets.

A deferred tax liability (DTL) or deferred tax asset (DTA) is created when there are temporary differences between book (IFRS, GAAP) tax and actual income tax. There are numerous types of transactions that can create temporary differences between pre-tax book income and taxable income, thus creating deferred tax assets or liabilities. While tax, in itself, is a complicated matter to analyze, deferred tax assets and liabilities add another layer of complexity in tax accounting.

To understand what is driving these deferred taxes, it is helpful for an analyst to examine the tax footnotes provided by the company. Often, a company will outline what major transactions during the period have made changes to the balances of deferred tax assets and liabilities. Companies will also reconcile effective tax rates in these footnotes.

Understanding changes in deferred tax assets and deferred tax liabilities allows for improved forecasting of cash flows.

Below are just some major classes of information to look for in footnotes. Understanding this information should allow an analyst to make sense of the changes in deferred tax balances. These transactions are sometimes apparent in the income statement or balance sheet.

Information relating to the creation of DTAs and/or DTLs includes some of the following:

The most notable creation of a deferred tax liability is due to differences between how depreciation is calculated by an appropriate tax authority vs GAAP or IFRS accounting.

Tax authority: Many tax authorities allow and/or require accelerated depreciation on newly acquired property, plant and equipment.

GAAP/IFRS: Unlike tax authorities, GAAP/IFRS rules give accountants freedom to select from multiple methods of depreciation. However, accountants typically use straight-line depreciation when preparing financial statements.

Accelerated depreciation allows for a higher depreciation expense early in an asset’s useful life, thus lowering the company’s taxable income and cash taxes. However, straight-line depreciation expense will be lower relative to accelerated depreciation and will show the company being more profitable, relative to its tax statements. Thus, a deferred tax liability is created with the recognition that this is a temporary difference and the company will end up paying more in taxes in the future.

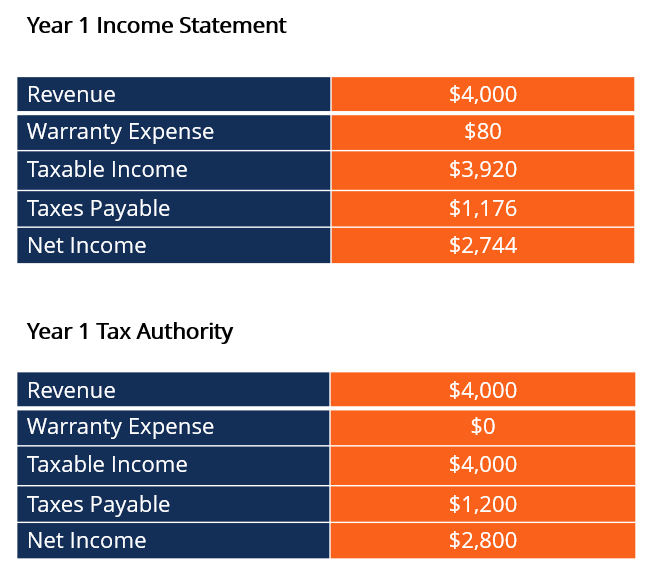

The tax rate for the year is 30%, and the company estimates warranty expense will be 2% of its revenue. Therefore, the company will report taxable income of $3,920 ($4,000 – $80 = $3,920) on its financial statements. However, many tax authorities will not allow a tax deduction for warranty expense; thus, the company will be taxed on the full amount of revenue (in this simple example).

Assuming the tax rate is 30%, the difference in taxes payable for book and tax purposes is $24 ($80 * 30%). Since this is considered a temporary timing difference between book and tax accounting (assuming the company correctly estimated its future warranty expense), the company would create a DTA of $24 to reflect the fact that its actual tax burden going forward will be lower since it effectively “prepaid” taxes.

Due to the accounting principle of conservatism, it is important for management to make good estimates and judgments when it comes to deferred tax assets. In other words, there needs to be a prospect that the deferred tax asset will be utilized in the future. For example, if a carryforward loss is allowed, a deferred tax asset will be present on the company’s financial statements (due to losses in previous years). In such a situation, a deferred tax asset needs to be documented if and only if there will be enough future taxable profits to service the tax loss.

If the company is not profitable enough in the future, the value of the deferred tax asset will be impaired. Therefore, the company will create a contra asset account known as a valuation allowance. The valuation allowance reduces the value of the deferred tax asset if the company estimates it will not be able to utilize its DTAs. An increase in the valuation allowance results in an increase in a company’s tax expense on its financial statements.

After understanding the changes and causes of the deferred tax balance, it is important to also analyze and forecast the effect this will have on future operations. For example, deferred tax assets and liabilities can have a strong impact on cash flow. An increase in deferred tax liabilities or a decrease in deferred tax assets is a source of cash. Likewise, a decrease in the DTL or an increase in the DTA is a use of cash.

Analyzing the change in deferred tax balances should also help to understand the future trend these balances are moving towards. Will the balances continue growing, or is there a high likelihood of a reversal in the near future?

These trends are often indicative of the type of business undertaken by the company. For example, a growing deferred tax liability could signal that a company is capital-intensive. This is because the purchase of new capital assets often comes with accelerated tax depreciation that is larger than the decelerating depreciation of older assets.