Accounts Receivable

Revenue that has not been paid for with cash yet

Over 1.8 million professionals use CFI to learn accounting, financial analysis, modeling and more. Start with a free account to explore 20+ always-free courses and hundreds of finance templates and cheat sheets.

What is Accounts Receivable (AR)?

Accounts Receivable (AR) represents the credit sales of a business, which have not yet been collected from its customers. Companies allow their clients to pay for goods and services over a reasonable extended period of time, provided that the terms have been agreed upon. For certain transactions, a customer may receive a small discount for paying the amount due to the company early.

The average AR days measure is an important part of forecasting changes in non-cash working capital in financial modeling.

Why do Companies have Accounts Receivable?

Some businesses allow selling on credit to make the payment process easier. Take, for example, a phone provider. The provider may find it hard to collect payment perpetually every time someone makes a call. Instead, it will bill periodically at the end of the month for the total amount of service used by the customer. Until the monthly invoice has been paid, the amount will be recorded in accounts receivable.

Allowing purchases on credit also encourages more sales. Customers are more likely to buy items if they can pay for them at a later date.

For someone working in FP&A, equity research, or investment banking, it’s important to understand the cash conversion cycle – the amount of time it takes a company to convert its inventory into sales and then cash – as it provides important information on the company’s cash flow.

Risks of Outstanding Accounts Receivable Balances

There are several risks associated with carrying a large AR balance, including:

- Uncollected debt – High A/R that goes uncollected for a long time is written off as bad debt. This situation occurs when customers who purchase on credit go bankrupt or otherwise do not pay the invoice.

- Cash flow deficiencies – A business needs cash flow for its operations. Selling on credit may boost revenue and income, but it offers no actual cash inflow. In the short term, it is acceptable, but in the long term, it can cause the company to run short on cash and have to take on other liabilities to fund operations.

AR’s Impact on Cash Flow and Financial Modeling

When a company has an accounts receivable balance, it means that a portion of revenue has not been received as cash payment yet. If payment takes a long time, it can have a meaningful impact on cash flow. For this reason, in financial modeling and valuation, it’s very important to adjust free cash flow for changes in working capital, which includes AR, accounts payable, and inventory.

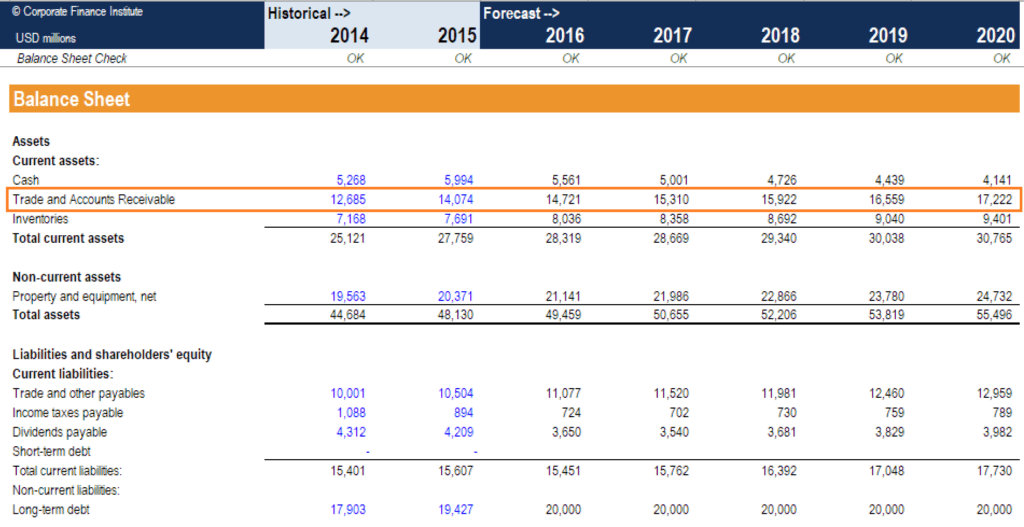

In the example below, you can see how AR is portrayed on the balance sheet in one of CFI’s financial models.

Source: CFI Financial Modeling Course.

Watch the video tutorial below to learn more about accounts receivable and accounts payable:

Additional Resources

Thank you for reading this guide to Accounts Receivable (AR) and how it impacts a company’s cash flow. CFI is the official provider of the Financial Modeling and Valuation Analyst (FMVA)® certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and advancing your career as a financial analyst, check out the following additional CFI resources:

Free Accounting Courses

Learn accounting fundamentals and how to read financial statements with CFI’s free online accounting classes.

These courses will give the confidence you need to perform world-class financial analyst work. Start now!

Building confidence in your accounting skills is easy with CFI courses! Enroll now for FREE to start advancing your career!