Revolving Debt

A line of credit that corporations can borrow from and pay back as needed

Over 1.8 million professionals use CFI to learn accounting, financial analysis, modeling and more. Start with a free account to explore 20+ always-free courses and hundreds of finance templates and cheat sheets.

Overview of Revolving Debt

A revolving debt (a “revolver,” also sometimes known as a line of credit, or LOC) does not feature fixed monthly payments. It differs from a fixed payment or term loan that has a guaranteed balance and payment structure.

Instead, the payments of revolving debt are based on the balance of credit every month. Interest payments are calculated likewise; payments are based on the interest rate and balance and are often computed daily.

Applying for Revolving Debt

Revolving debt is applied for in similar ways to credit cards. In fact, a credit card can be seen as a type of revolving debt.

Before granting the line of credit to an applicant, a bank or institution will consider the applicant’s ability to repay and service the debt. Often, this means taking a look at the credit score, financial stability, job, and income of the borrower.

For businesses, banks and financial institutions may look at company financials, such as the income statement, the statement of cash flows, and the balance sheets. There are several financial metrics that can be used with these statements to determine the business’ ability to pay.

There are various types of revolvers, including signature loans, credit cards, and home equity lines of credit. As stated above, the most common form of revolving debt is the credit card, whether it be for an individual or a corporation.

Credit cards are effectively the medium or tool that lets a borrower access a revolving debt account. Minimum payments are generated depending on the balance of the card, and any remaining credit is usable in the next month. Payments reduce interest and increase the available credit, while purchases increase interest and reduce credit.

Because of this accessibility and liquidity, revolvers often come with higher interest rates than traditional term loans. Furthermore, different types of revolving debt facilities offer different rates. A personal line of credit will have lower rates than credit cards, and a home equity line of credit will have lower rates than the personal line. The latter arises due to the backed security involved in home equity LOCs.

Benefits of a Revolving Debt

Revolving debt is useful for individuals and businesses that need to borrow funds quickly and as needed. A person or business that experiences sharp fluctuations in cash income may find a revolving line of credit a convenient way to pay for daily or unexpected expenses. They also allow the flexibility of buying items now and paying for them later.

Dangers of Revolving Debt

If used carelessly, revolving debt can spiral out of control.

Individuals, companies, and countries are at risk for financial difficulty if they have taken on too much debt. Also, borrowing too much and/or not paying on time will hit one’s credit report with potentially negative information. Bad credit ratings send a negative signal to banks and can pose problems in the approval of new loan applications.

Falling into debt over and over again can lead to some major problems such as loss of cash flow, loss of time, and also loss of opportunities.

Applications in Financial Modeling

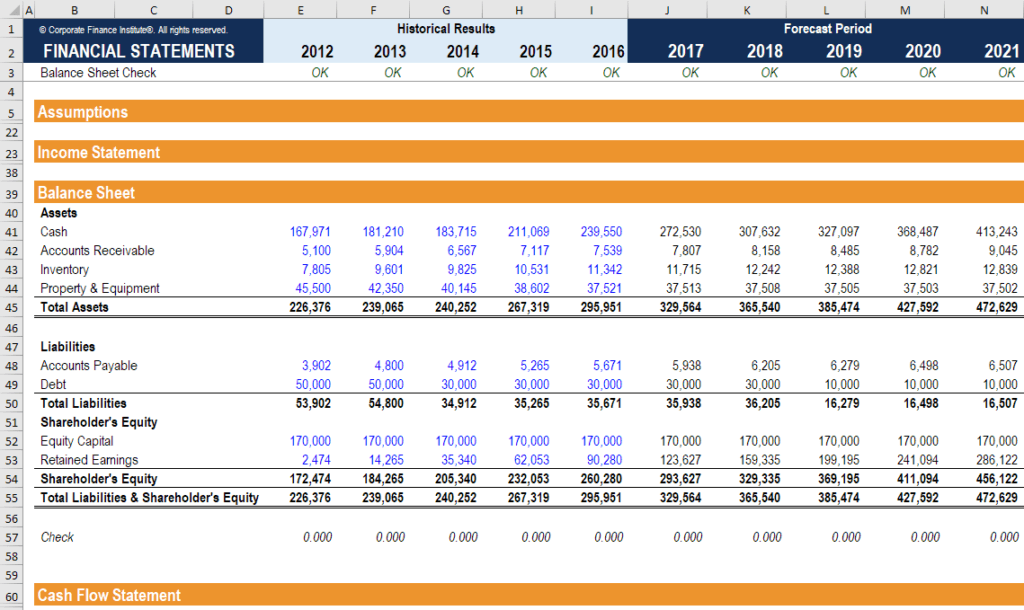

For financial analysts performing financial modeling, building in a revolver can be a very important exercise. Instead of having the model run into a negative cash position, the model will automatically draw on a revolver that has been set up.

Learn more with CFI’s financial modeling courses.

Additional Resources

Learn more about how revolving debt works and how to manage it with the following CFI resources: