Interest Rate Differential (IRD)

A charge that applies if a borrower pays off the entirety of the mortgage before its maturity date

Over 1.8 million professionals use CFI to learn accounting, financial analysis, modeling and more. Start with a free account to explore 20+ always-free courses and hundreds of finance templates and cheat sheets.

What is an Interest Rate Differential (IRD)?

An interest rate differential is a charge that applies if a borrower pays off the entirety of the mortgage before its maturity date. Most mortgages that are given at major lending institutions charge either the interest rate differential or three months of payment interest.

Generally, a lender will use the IRD if the interest rate on a homebuyer’s mortgage is higher than their current interest rate, or they signed the mortgage less than five years ago. It is a tool for lending institutions to make up the lost payments that they could have gained on the funds had they lent them elsewhere.

It is an important concept to understand for every homebuyer, especially those who receive a cash windfall and are thinking about paying off their mortgage early. The IRD is often passed along as a fee in order to mitigate the opportunity cost of a bank potentially having to loan out the money that accrues a lower rate of interest.

Interest rate differentials are also used to calculate future currency exchange rates and understand the premium or discount futures hold to current market rates. Simply put, it measures the differences in interest rates.

Summary

- An interest rate differential (IRD) is a charge that applies if a homebuyer pays off the entirety of the mortgage before its maturity date.

- It can also be used to calculate future exchange rates on currency and understand the premium or discount futures hold to current market rates.

- The IRD is the interest fee remaining on the current payments for both rates, and the remainder is said to be the IRD.

Interest Rate Differentials: Why are they Important?

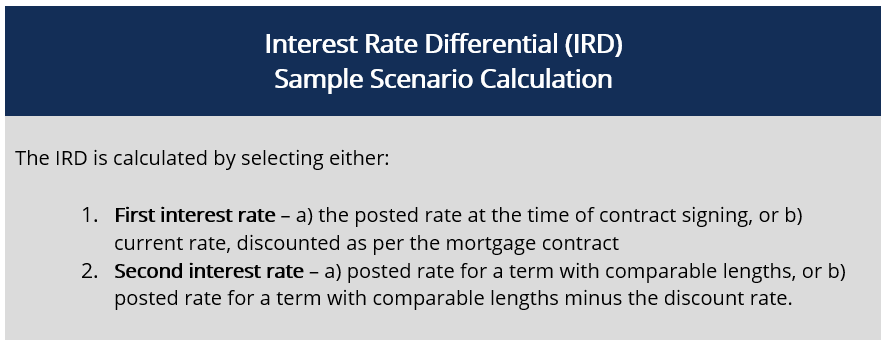

Typically, an IRD is calculated one of two ways and uses two different interest rates. The IRD is essentially the interest fee remaining on your current payments for both rates, and the remainder is said to be the IRD. For futures, if one security (like a Treasury note) earns an interest rate of 8% and another earns an interest rate of 6%, the IRD is 2%. The below infographic represents a sample IRD calculation for mortgages:

Key Considerations

Deciding whether or not to pay off a loan early is based on several factors. Paying off debt before the interest can be collected is not the ideal outcome for the institution lending money, and thus fees, including interest rate differential payments, will likely be required.

This is because in the instance that interest rates fall, the bank must now lend the money out to an individual at a lower level of interest. Thus, they are losing the interest that was originally loaned out at a higher rate.

This opportunity cost is detrimental to lenders’ financial forecasts and projected cash flows. Further, if interest rates have now declined, they must now loan the money out at a lower rate and miss out on the spread between both rates.

Thus, penalizing rates like that IRD are usually applied for those looking to pay off their loans quicker than the period than originally signed up for. However, paying the IRD can still be beneficial as future loan payments will now all be foregone.

More Resources

CFI offers the Certified Banking & Credit Analyst (CBCA)® certification program for those looking to take their careers to the next level. To keep learning and advance your career, the following resources will be helpful: