Get Certified for

Capital Markets (CMSA®)

From equities, fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

This article outlines what contango and backwardation are, why they matter, and how investors interpret them.

Over 1.8 million professionals use CFI to learn accounting, financial analysis, modeling and more. Start with a free account to explore 20+ always-free courses and hundreds of finance templates and cheat sheets.

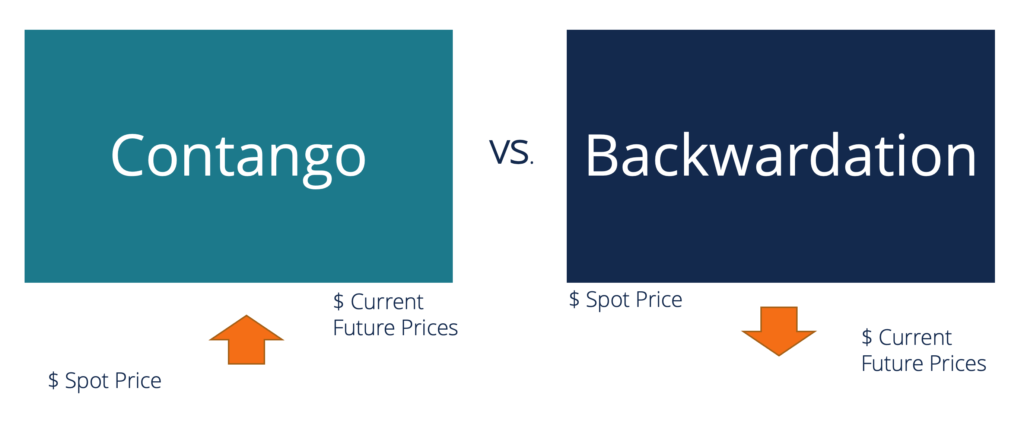

Contango and backwardation are terms used to describe the observed difference between the spot, or cash, price and futures prices for a commodity. The curve has two dimensions, and plots time across the horizontal axis and delivery price of the commodity across the vertical axis. This guide will break down the key differences between Contango vs Backwardation.

Contango describes an upward sloping curve where the prices for future delivery are higher than the spot price (e.g., the price of gold delivered in 1 year is $1,400/oz and the spot price is $1,200/oz). Contango is common in the gold industry, where the commodity is non-perishable and there are storage costs.

Contango exists for multiple reasons including inflation, carry costs (storage and insurance), and expectations that real prices will be higher in the future.

Backwardation describes a downward sloping curve where the prices for future delivery are lower than the spot price (e.g., the price of oil delivered in 3 months is $40/bbl and the spot price is $50/bbl).

Backwardation exists for various reasons, including short-term events that can cause the spot price to rise above future prices. For example, if a major drought causes wheat crops to suffer then the spot price may spike up above the future prices, when growing conditions are expected to be normal again.

The futures curve can be used as price inputs when building a financial model for a commodities company. The curve can be used as a “scenario” or “price deck” in the model, which is common in the mining industry, for example.

There are many jobs in finance that require knowledge of contango and backwardation. Explore our Career Map to find the perfect career path for you in corporate finance.

Thank you for reading this guide to Contango vs Backwardation. To keep learning and developing your financial analyst career path, check out these additional resources: