Annuitant

An entity that is entitled to collect a series of payments made on an interval basis

Who is an Annuitant?

An annuitant is an entity that is entitled to a series of payments on an interval basis. Annuitants are often investors or retirees receiving their pension payments.

Primarily, financial institutions and life insurance companies utilize an annuity payment structure to provide income on a periodic basis. Annuities often begin with a lump-sum payment by the annuitant, and contractually obligated cash flows for the stated period.

Summary

- An annuitant is an entity that is entitled to a series of payments on an interval basis.

- Fixed annuities, variable annuities, life annuities, and fixed index annuities are four common types of annuities.

- Payments, interest rates, and length of time are all major factors in evaluating an annuity’s cash flow.

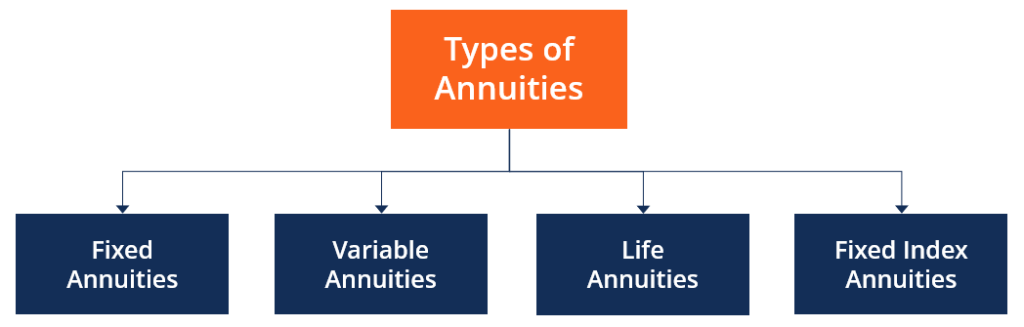

Types of Annuities

1. Fixed Annuities

These are annuities that provide fixed payments. The increased security afforded by fixed payments leads to a lower rate of return. This type of annuity is commonly used in payment plans. Several publicly traded securities offer fixed annuities.

2. Variable Annuities

Variable annuities allow the annuitant to select a portfolio of investments that pay income aligned with the portfolio’s performance. Since income is not guaranteed, annuitants require greater compensation given the risk. This increase in risk can lead to the annuity not producing a predictable set of cash flows.

Defined contribution plans are a type of pension plan that defines how much the employer contributes to it but does not guarantee a fixed payment amount. This is a common practical example of a variable annuity.

3. Life Annuities

Life annuities provide fixed payments to annuitants until their death. Defined benefit plans, where employers promise to pay pensioners a fixed amount each term, is a life annuity. Actuaries are responsible for determining the size of this benefit and calculate the span of this investment based on the predicted actuarial life of the annuity.

4. Fixed Index Annuities

In a fixed index annuity, payments made to annuitants vary depending on the performance of an index fund, like the Dow Jones Index or the S&P 500. This is very similar to a variable annuity and can be applied similarly in a defined contribution pension plan.

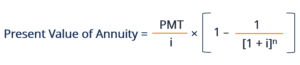

General Annuity Theorem

Where:

- PMT: Payment

- i: Discount Rate

- n: Number of payments

Factors Impacting Annuity Valuation

1. Payments

The payments in an annuity are the contractual cash flows promised in an annuity. The payments can differ in terms of timing and amount, depending on the annuity product held by the annuitant.

For example, variable annuities provide cash flows varying on the success of the underlying investment. Therefore, cash flows vary on a term-to-term basis. On the contrary, defined benefit plans for retirees come with a specified cash flow – contractually obligated pension payments made to the annuitant.

2. Discount Rate

The discount rate is the rate at which future cash flows are discounted. The higher the discount rate used, the lower the present value of the annuity. Generally, the discount rate is the risk-free rate of return. The risk-free rate is often based on U.S Treasury bond yields.

3. Number of Periods

The number of periods indicates the number of contractual payments remaining. The further in the future that cash flow will be received, the less it will be worth today.

Valuation of Annuities

1. Annuity Due

In an annuity due, payments are made at the beginning of each period. Generally, annuitants who enter an annuity-due contract are individuals who require cash inflow immediately.

2. Ordinary Annuity

In an ordinary annuity, payments are made at the end of each period. Annuity products are attractive because they embrace tax-deferral benefits.

Annuity – Example

Consider a technology company that recently obtained a license to provide software to a large corporation. The two companies agree that the large corporation will pay the technology company $100 million each year for six years.

Today is January 1, 2018, and payments are made at the end of each year. Prevailing interest rates in the economy are 10%.

Assuming:

- Ordinary Annuity

- Discount Rate: 10%

- Number of Periods: 6

- Cash Flow: $100 million

How are Annuitants Taxed?

The exclusion ratio refers to the portion of an investment’s return that is not taxed. It is a percentage of the total payout that equates the initial investment. This means that the initial principal returns to the annuitant tax-free and taxes are paid on the profits from the investment. Annuities are fully taxed over the period the annuitant outlives their actuarial life expectancy.

Annuities can grow tax-deferred, with the implication being that earnings are not taxed until they are paid out. This allows the investment to grow without being reduced by tax payments.

If you purchase an annuity with pre-tax dollars, payments from the annuity are fully taxable as income. Therefore, if you purchase an annuity with pre-tax dollars, there is no exclusion ratio. If you buy an annuity with after-tax income, taxes must be paid strictly on earnings. In this scenario, the exclusion ratio would be the principal.

More Resources

CFI is the official provider of the Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to transform anyone into a world-class financial analyst.

In order to help you become a world-class financial analyst and advance your career to your fullest potential, these additional resources will be very helpful: