Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The cost incurred by an organization to compensate employees and contractors for work performed over a specific time period

Wage expense refers to the cost incurred by an organization to compensate employees and contractors for work performed over a specific time period.

The difference between wages and salaries is often poorly understood. Understanding the difference between wage expense and salary expense allows an analyst to better forecast the costs of an organization.

Example: The following illustrates the amount paid to an employee by an organization over the past three months. Is it an example of wage expense or salary expense?

Answer: Given the variable nature of the payment each month, the above is an example of wage expense.

There are three main types of wage expenses:

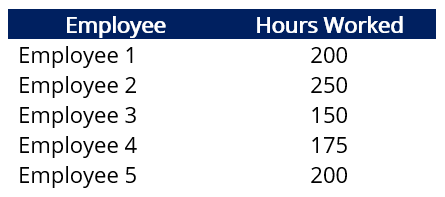

Background Information: A company currently employs five individuals. Employees 1 and 2 are each paid $6,000 per month, while Employees 3, 4, and 5 are paid $15 per hour. The following shows the number of hours worked by each employee for the month of January:

Question: Determine the wage expense and salary expense for the month of January.

Answer: Employees 1 and 2 are each paid $6,000 per month (salary). The salary expense for the month of January is $12,000. Employees 3, 4, and 5 are paid $15 per hour. In aggregate, they worked 525 hours. The wage expense for the month of January is 525 x $15 = $7,875.

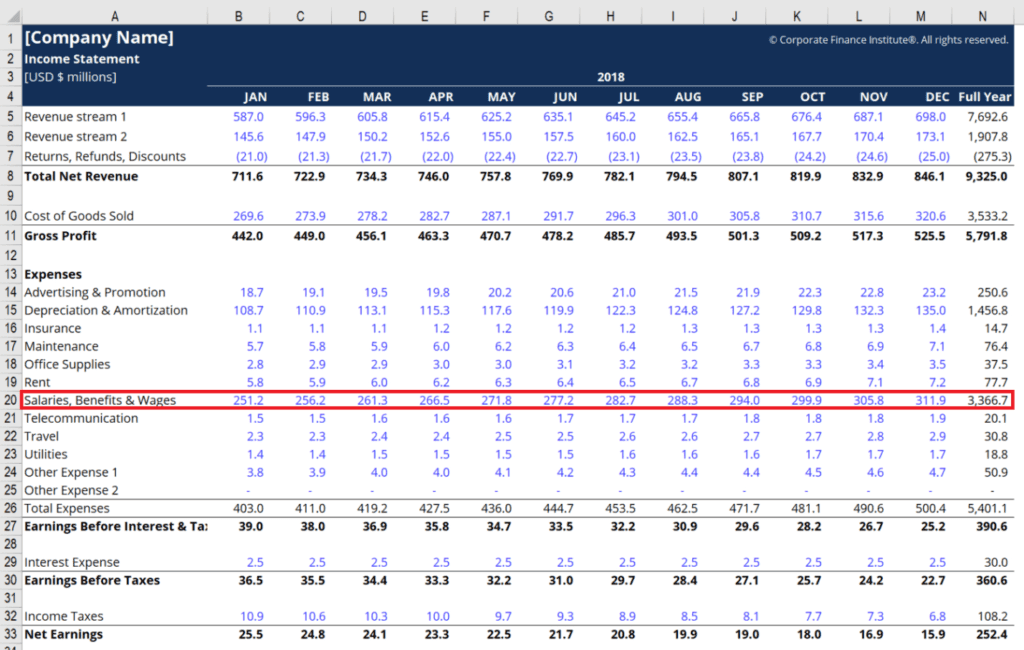

Wage expense on the income statement is typically combined with similar expenses, as shown below.

For companies that produce goods (i.e., manufacturing companies), a portion of their wage expense may be aggregated into costs of goods sold (COGS) on the income statement. As you may recall, COGS refers to direct costs related to the production of goods, which include the cost of materials, labor, and manufacturing overhead.

As an example, assume that a manufacturing company incurred a wage expense of $200,000 for the fiscal year 2020. Of the $200,000, 25% relate to wages for factory workers while the remaining relate to wages for workers at the head office.

In such a scenario, only $150,000 would be classified as wage expense on the company’s income statement. The remaining $50,000 would be aggregated into COGS (assuming the products produced by the factory workers are sold in the same year).

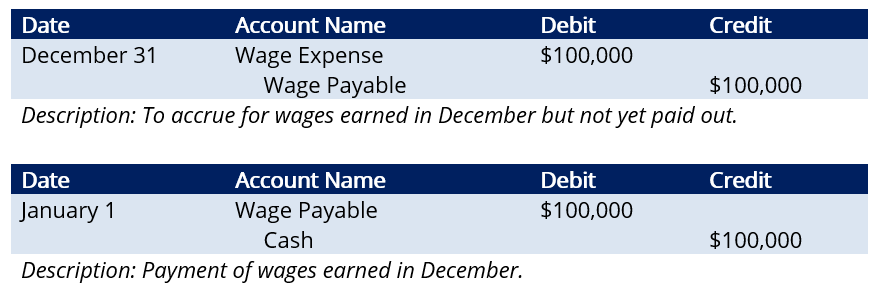

Companies commonly prepare financial statements on an accrual basis. Below, we illustrate the journal entries for wage expense.

Background Information: Company A pays its employees on the first day of the next month. For example, wages for work done in the month of December are paid on the first day of January.

Question: Wages for employees in the month of December totaled $100,000. What would be the relevant journal entries?

Answer:

CFI offers the Financial Modeling & Valuation Analyst (FMVA®) certification program for those looking to take their careers to the next level. To keep learning and developing your knowledge base, please explore the additional relevant resources below: