Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

A senior class of equity

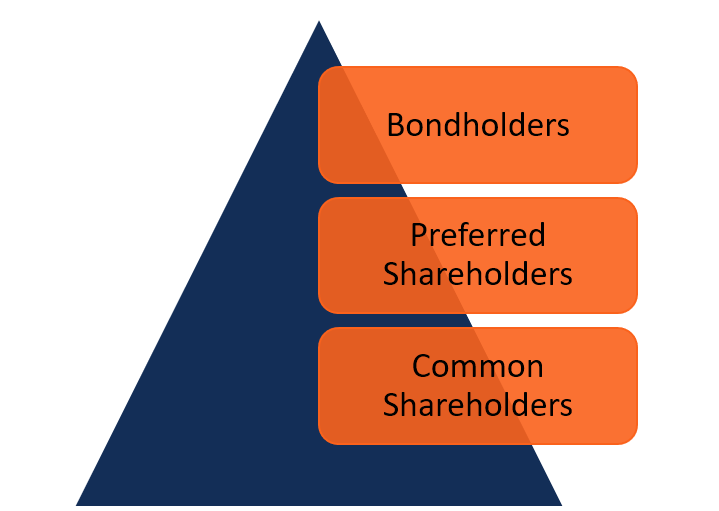

Preferred shares, also called preferred stock, are a unique class of equity ownership in a company, but with bond-like features such as fixed dividends. Investors buy preferred shares for steady dividend income and potentially higher yields. Preferred shareholders are also paid before common shareholders, but after debt holders, in the event of liquidation.

Companies issue preferred shares to raise capital without diluting voting control. This guide covers what preferred shares are, how they work in practice, real-world issuance examples, types, pros and cons, tax treatment, valuation, and how to invest.

Preferred shares have a special combination of features that differentiate them from debt or common equity. Although the terms may vary, the following features are common:

Dividend Payments Usually a fixed rate, but can be a floating rate, stated in terms of par value, based on a benchmark such as SOFR Vary based on company performance

Voting Rights Typically none Yes

Liquidation Priority Higher than common stockholders Lowest priority

Price Volatility Usually less volatile than common stock, but more volatile than bonds High volatility

Preferred shares can be structured in various ways to meet the needs of both the issuer and the investor. Here are the main types, with practical explanations and examples.

Example: Private equity-backed firms sometimes use participating preferreds in deal structures.

Cumulative

Non-Cumulative

Convertible

Callable

Participating

When a company issues preferred shares, it typically sets:

Dividends are paid before any common stock dividends. If dividends are cumulative, unpaid preferred dividends roll forward until paid in full. Non-cumulative preferreds don’t carry over unpaid dividends.

Example:

If ABC Bank issues $100 million in 5% preferred shares, each with a par value of $25, investors receive $1.25 per share annually (5% × $25), typically in quarterly installments of $0.3125.

In March 2023, JPMorgan issued $500 million of non-cumulative preferred shares with a fixed dividend rate of 5.75%. The issuance allowed the bank to strengthen its Tier 1 capital ratio without diluting common shareholders’ voting rights.

RBC issued CAD $350 million in rate-reset preferred shares, offering a 4.90% dividend for the first five years, after which the rate resets based on the Government of Canada five-year bond yield plus a 3.5% spread. This structure offers income stability initially and some protection against interest rate changes.

Understanding both the benefits and drawbacks of preferred stock is crucial for making informed investment or corporate financing decisions.

Investors Stable income, priority claim, moderate volatility, possible tax benefits Limited upside, interest rate risk, call risk, possible dividend suspension

Issuers No voting dilution, flexible financing, appeal to institutions Dividend obligation, higher cost than debt, impact on leverage

Preferred shares are usually valued based on the present value of their expected dividend payments. Because many preferreds have fixed dividends, they can be analyzed similarly to bonds, but with equity-specific adjustments.

Formula:

Where:

Example:

A preferred share pays a $1.50 annual dividend. If investors require a 6% return:

P0 = 1.50 / 0.06 = $25.00

If market yields rise to 7%, the price falls:

P0 = 1.50 / 0.07 = $21.43

For callable preferreds, investors often calculate Yield-to-Call instead of Yield-to-Maturity.

Formula:

Rate-reset preferreds (common in Canada) adjust their dividend every reset period.

Formula:

Example:

New Dividend Rate = 5.70% (applied to par value)

Preferred shares can be accessed through primary offerings, secondary markets, or pooled investment products.

Preferreds are first sold through underwriters when issued. While institutions typically receive the bulk of allocations, some offerings may become available to retail investors through brokerage platforms.

Most investors purchase preferreds on securities exchanges, such as the NYSE, TSX, or LSE, after issuance. Prices trade above or below par depending on interest rates, credit quality, and market demand.

Exchange-traded funds and mutual funds provide diversified exposure to the preferred share market. Examples include the iShares Preferred and Income Securities ETF (PFF) in the U.S. and the BMO Laddered Preferred Share Index ETF (ZPR) in Canada.

Preferred shares are hybrid securities that combine features of stocks and bonds. They pay fixed or floating dividends that take priority over common stock, though after bond interest and other debt obligations. Investors are often drawn to them for their stable income, but they come with trade-offs such as limited capital appreciation and heightened sensitivity to interest rates.

Key variations, such as cumulative, convertible, and callable shares, affect the balance of risk, return, and flexibility for investors. Issuers use preferred shares to raise capital without diluting voting control.

Before investing, it’s important to evaluate factors such as dividend structure, the issuer’s credit rating, call provisions, and jurisdiction-specific tax treatment. Make sure you understand how preferred shares are structured, along with their benefits and risks, to determine if preferred shares align with your or your client’s income goals and portfolio strategy.

Explore CFI’s industry-leading programs and resources to build your skills:

Start building a strong foundation today and set yourself apart in one of the most rewarding sectors in finance.

Thank you for reading CFI’s guide to Preferred Shares. To help you advance your career, check out the additional CFI resources below: