Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Profit after deducting direct costs from sales revenue

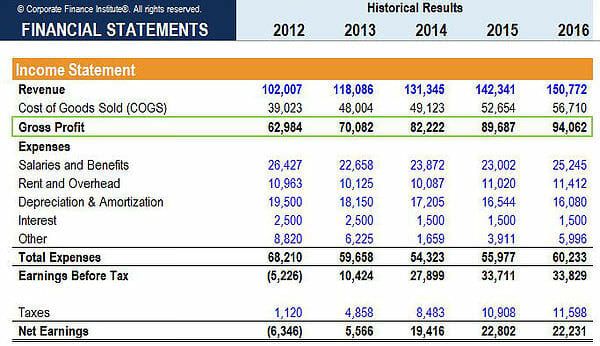

The Gross Profit (GP) of a business is the accounting result obtained after deducting the cost of goods sold and sales returns/allowances from total sales revenue. GP is located on the income statement (sometimes referred to as the statement of profit and loss) produced by a company and used to determine a company’s gross margin. Below is an example:

The gross profit formula is:

Gross Profit = Sales Revenue – Cost of Goods Sold

To illustrate:

As of the first quarter of business operation for the current year, a bicycle manufacturing company has sold 200 units, for a total of $60,000 in sales revenue. However, it has incurred $25,000 in expenses, for spare parts and materials, along with direct labor costs. There were also returns and allowances for a total of $1,000. As a result, the gross profit declared in the financial statement for Q1 is $34,000 ($60,000 – $1,000 – $25,000).

Sales revenue or net sales is the monetary amount obtained from selling goods and services to customers – excluding merchandise returned and any allowances/discounts offered to customers. This can be realized either as cash sales or credit sales.

Cost of goods sold, or “cost of sales,” is an expense incurred directly by creating a product. It includes any raw materials and labor costs incurred. However, in a merchandising business, cost incurred is usually the actual amount of the finished product (plus shipping cost, if any) purchased by a merchandiser from a manufacturer or supplier. In any event, cost of sales is properly determined through an inventory account or a list of raw materials or goods purchased.

Gross profit serves as the financial metric used in determining the gross profitability of a business operation. It shows how well sales cover the direct costs related to the production of goods.

The formula for calculating gross margin is:

Gross Margin = Gross Profit / Total Revenue x 100

Gross margin is expressed as a percentage. For example, a company has revenue of $500 million and cost of goods sold of $400 million; therefore, their gross profit is $100 million. To get the gross margin, divide $100 million by $500 million, which results in 20%.

Thank you for reading CFI’s guide to Gross Profit. With that in mind, these additional CFI resources will help you advance your career:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: