Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

A coverage ratio that measures the number of times a company can pay dividends to its shareholders

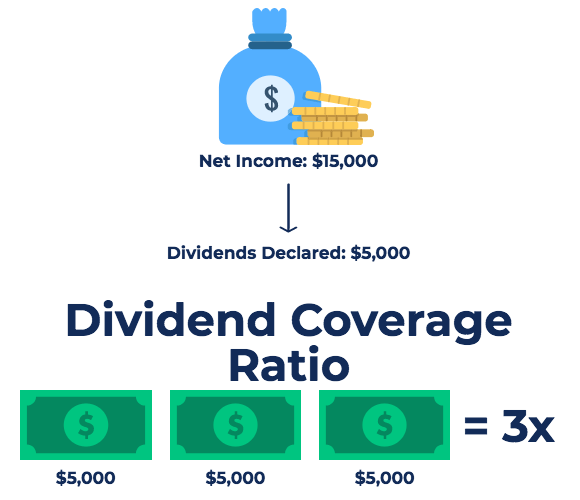

The Dividend Coverage Ratio, also known as dividend cover, is a financial metric that measures the number of times that a company can pay dividends to its shareholders. The dividend coverage ratio is the ratio of the company’s net income divided by the dividend paid to shareholders.

The general formula for calculating DCR is as follows:

Where:

There are also some modified versions of the dividend coverage ratio, which will be discussed below.

The first variation is used to determine the number of times a company can pay dividends to common shareholders when the company also has preferred shares to take into consideration.

The formula is:

The above variation can also be used to determine the number of times a company can pay dividends to preferred shareholders:

The formula is:

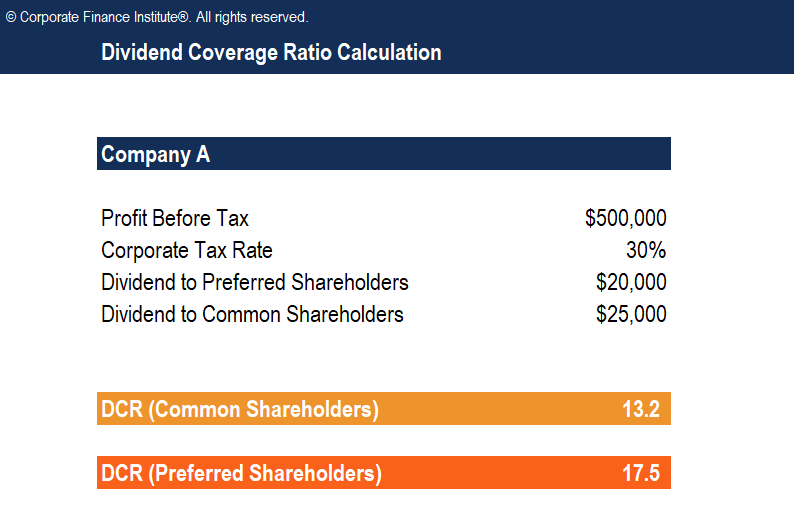

Let’s consider the following example. Company A reported the following figures:

Determine the dividend coverage ratio for preferred and common shareholders:

DCR (Common Shareholders) = ($500,000 x 70% – $20,000) / $25,000 = 13.2

DCR (Preferred Shareholders) = ($500,000 x 70%) / $20,000 = 17.5

If the dividend coverage ratio is greater than 1, it indicates that the earnings generated by the company are enough to serve shareholders with their dividends. As a rule of thumb, a DCR above 2 is considered good.

A deteriorating DCR or a dividend cover that is consistently below 1.5 may be a cause for concern for shareholders. A consistently low or deteriorating dividend cover may signal poor company profitability in the future, which may mean the company will be unable to sustain its current level of dividend payouts.

Although DCR is a useful indicator of dividend payment risk to shareholders, there are a couple of key issues with the ratio for investors to consider:

In calculating a company’s DCR, we use net income in the numerator. Net income does not necessarily equal cash flow. Therefore, a company may report a fairly high net income but still not actually have the cash available to make dividend payments.

Net income can change dramatically from one year to the next. Therefore, calculating a high DCR based on past historical performance may not be a reliable predictor of dividend risk in future years.

Nonetheless, the dividend cover is still commonly used by investors and market analysts to estimate the level of risk associated with receiving dividends from an investment.

In summary, the key points to know about the DCR are:

Thank you for reading CFI’s guide to Dividend Coverage Ratio. To help you advance your career in the financial services industry, check out the following additional CFI resources: