Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The actual value of a product, stock, or security that is agreed upon by both the seller and the buyer

Fair value refers to the actual value of an asset – a product, stock, or security – that is agreed upon by both the seller and the buyer. Fair value is applicable to a product that is sold or traded in the market where it belongs or under normal conditions – and not to one that is being liquidated. It is determined in order to come up with an amount or value that is fair to the buyer without putting the seller on the losing end.

For example, Company A sells its stocks to company B at $30 per share. Company B’s owner thinks he could sell the stock at $50 per share once he acquires it and so decides to buy a million shares at the original price. Despite the large profit potential for Company B, the sale is considered fair value because the price was agreed by both sides and they both benefit from the sale.

Fair value and carrying value are two different things. Consider the following:

To illustrate, let’s say Company A, a construction company, bought a backhoe for its operations at $30,000. Assuming it will last for 10 years, with a depreciation expense of $2,000 for each year, then its carrying value would already be $10,000.

Carrying Value = $30,000 – ($2,000 x 10) = $10,0000

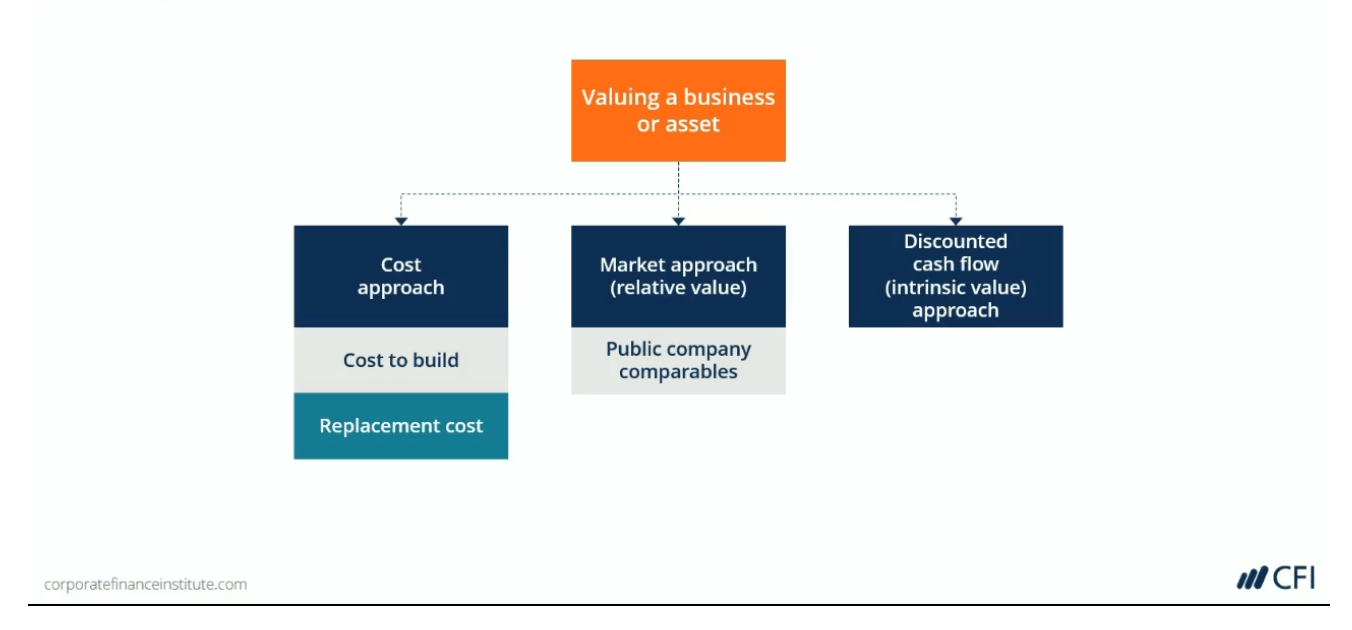

To learn more, check out CFI’s Business Valuation Modeling course.

Market value is also different from fair value in the following points:

If the owner tries to sell a property for $200,000 during a low time in the real estate market, then it might not get sold because the demand is low. But if it is offered for $500,000 during a high time, it may get sold at that price.

Fair value accounting measures the actual or estimated value of an asset. It is one of the most commonly used financial accounting methods because of its advantages, which include:

With fair value accounting, valuations are more accurate, such that the valuations can follow when prices go up or down.

With fair value accounting, it is total asset value that reflects the actual income of a company. It doesn’t rely on a report of profits and losses but instead just looks at actual value.

Such a method is able to make valuations across all types of assets, which is better than using historical cost value, which may change through time.

Fair value accounting helps businesses survive during a financially difficult time because it allows asset reduction (or the act of declaring that the value of an asset that is included in a sale was overestimated).

To learn more, check out CFI’s Business Valuation Modeling course.

Thank you for reading CFI’s guide to Fair Value. To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below:

Learn accounting fundamentals and how to read financial statements with CFI’s online accounting classes.

These courses will give you the confidence to perform world-class financial analyst work. Start now!

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.