Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

An estimate of an asset's price if sold during an unforeseen or uncontrollable event

A forced sale value is the estimate of the amount that a business would receive if it sold off its assets one piece at a time during an unforeseen or uncontrollable event. The appraiser assumes that the business needs to sell its assets within a short duration at an immediate auction.

The rush factor means that the business will end up accepting less compensation for the item on sale than it would under normal business conditions. A forced sale is carried out in response to an economic event, legal order, or changes in regulations.

When trading securities on margin, brokerage firms require their customers to observe margin requirements. This means that the clients must maintain their margins above the company’s requirements. In the event the account drops in value below the minimum margin requirement, the broker will issue a margin call to the client. The margin call informs them that the account is under-margined and they should deposit more funds into the account or sell some of their securities to raise the margin.

If the client fails to meet the margin requirement after receiving the warning, the broker has the right to force-liquidate the securities. They may achieve the liquidation by closing and selling off all open positions. Brokers resort to forced liquidation to protect themselves from possible losses resulting from the margined accounts. If they don’t sell off the current positions, they will be exposed to declining value investments and, hence, may incur losses on those accounts.

When determining the amount that a business would fetch in a forced sale, an appraiser estimates the amount that each asset owned by the business would cost if they were to be sold at an auction. The auction is based on a short timeframe of about 60-90 days, which only attracts a small pool of buyers. The appraiser then sums up the estimated value of all assets to arrive at the total forced sale value. The value represents the minimum value that the business would get if it were to sell all its assets at an auction.

There are certain instances when using forced sale value is a good idea for a business. One of these instances is when the business is troubled and needs to obtain capital within a short time. The business will sell its machinery and equipment as-is, without having to repair or service them for resale. The buyers will purchase the assets at a price that is below the fair market value, with the plan of using them in their own businesses or servicing them and re-selling them at a higher price.

The forced sale valuation method would, however, not be ideal for a healthy business that is disposing of its assets. The business can prolong the auction period to attract a larger pool of buyers who would be willing to pay more for an asset that’s been serviced and is in mint condition. Also, prolonging the auction period gives the business more time to repair and service the assets to increase their valuation.

Apart from using the forced sale valuation, appraisers may also use alternative methods of valuation such as fair market value and orderly liquidation value.

The orderly liquidation value is based on the assumption that the seller has a reasonable amount of time to sell an asset to the highest bidder. The seller uses a channel of sale with the largest pool of buyers with the ability to buy the asset at a relatively higher rate.

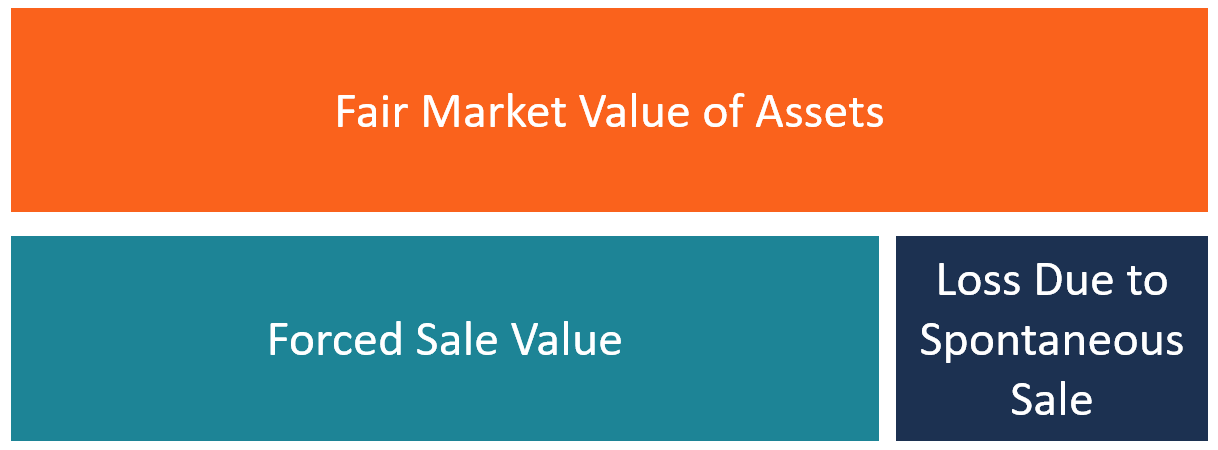

With the forced sale value, the seller is under coercion to sell off the equipment, buildings, and other assets. The buyer takes advantage of the seller’s economic event to force the sale of the assets within a short duration, and the practice attracts reduced sales value compared to the other methods. Due to the urgency associated with the forced sale method, the value of the assets is usually lower than the fair market value and the orderly liquidation value.

On the other hand, fair market value refers to the value that the business would get if it sold its assets at a fair market price. It based on the assumption that the asset is being sold in the open market, and that neither the seller or the buyer is being forced into the transaction.

Comparing the three valuation methods, the forced sale method fetches the lowest value, followed by the orderly liquidation method, whereas the fair market value method offers the highest value, since the assets are sold in the open market and are accessible by a large number of buyers.

Thank you for reading CFI’s explanation of forced sale value. CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful: