Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Costs that vary depending on the volume of activity

Variable costs are expenses that vary in proportion to the volume of goods or services that a business produces. In other words, they are costs that vary depending on the volume of activity. The costs increase as the volume of activities increases and decrease as the volume of activities decreases.

Essentially, if a cost varies depending on the volume of activity, it is a variable cost.

The formula for calculating the total variable cost is:

Costs incurred by businesses consist of fixed and variable costs. As mentioned above, variable expenses do not remain constant when production levels change. On the other hand, fixed costs are costs that remain constant regardless of production levels (such as office rent). Understanding which costs are variable and which are fixed is important to business decision-making.

For example, Amy is quite concerned about her bakery as the revenue generated from sales is below the total costs of running the bakery. Amy asks for your opinion on whether she should close down the business or not. Additionally, she’s already committed to paying for one year of rent, electricity, and employee salaries.

Therefore, even if the business were to shut down, Amy would still incur these costs until the year-end. In January, the business reported revenues of $3,000 but incurred total costs of $4,000, for a net loss of $1,000. Amy estimates that February should experience revenues similar to those of January. Amy’s list of costs for the bakery is as follows:

A. January Fixed Costs:

Total January Fixed Costs: $1,700

B. January Variable Costs:

Total January Variable Costs: $2,300

If Amy did not know which costs were variable or fixed, it would be harder to make an appropriate decision. In this case, we can see that total fixed costs are $1,700 and total variable expenses are $2,300.

If Amy were to shut down the business, Amy must still pay the monthly fixed costs of $1,700. If Amy were to continue operating despite losing money, she would only lose $1,000 per month ($3,000 in revenue – $4,000 in total costs). Therefore, Amy would actually lose more money ($1,700 per month) if she were to discontinue the business altogether.

This example illustrates the role that costs play in decision-making. In this case, the optimal decision would be for Amy to continue in business while looking for ways to reduce the variable expenses incurred from production (e.g., see if she can secure raw materials at a lower price).

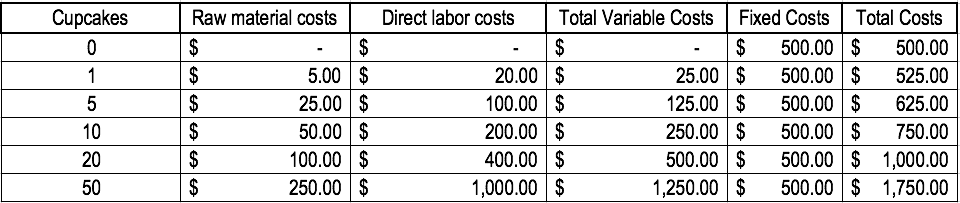

Let us consider a bakery that produces cakes. It costs $5 in raw materials and $20 in direct labor to bake one cake. In addition, there are fixed costs of $500 (the equipment used). To illustrate the concept, see the table below:

Note how the costs change as more cakes are produced.

Variable costs play an integral role in break-even analysis. Break-even analysis is used to determine the amount of revenue or the required units to sell to cover total costs. The break-even formula is given as follows:

Consider the following example:

Amy wants you to determine the minimum units of goods that she needs to sell in order to break even each month. The bakery only sells one item: cakes. The fixed costs of running the bakery are $1,700 a month, and the variable costs of producing a cake are $5 in raw materials and $20 in direct labor. Additionally, Amy sells the cakes at a sales price of $30.

To determine the break-even point in units:

Break-Even Point in Units = $1,700 / ($30 – $25) = 340 units

Therefore, for Amy to break even, she would need to sell at least 340 cakes a month.

The variable cost ratio is a cost accounting tool used to express a company’s variable production costs as a percentage of its net sales. The ratio is calculated by dividing the variable costs by the net revenues of the company. The company’s net revenue includes the sum of its returns, allowances, and discounts subtracted from the total sales.

The primary motive for calculating the variable cost ratio is to consider costs that may be subject to variations with changes in levels of production and compare them to the amount of revenues generated by the sales of that particular cycle of production.

In calculating the ratio, fixed costs, which are the expenses that remain constant regardless of variations in production levels, are excluded. Examples of fixed costs include building lease, employee salaries, etc.

The formula for the calculation of the variable cost ratio is as follows:

An alternate formula is given below:

The contribution margin is a quantitative expression of the difference between the company’s total sales revenue and the total variable costs of production of goods that were sold. The contribution margin is expressed in percentage points.

There are several ways in which the variable cost ratio can be calculated. Under the first method, the mathematical calculation is performed on a per-unit basis. In such a situation, consider a product with a per-unit variable cost of $10 and a per-unit sales price of $100. It gives a variable cost ratio of 0.1 or 10%.

The calculation can also be done by utilizing totals over a given period of time. Consider a situation wherein the total variable costs of production are $1,000 per month, and the total revenues generated per month are $10,000. The variable cost ratio, in this situation, is 0.1 or 10%.

The variable cost ratio is a key factor in assessing a company’s overall profitability. It is important for the following reasons:

When a company sees high variable costs relative to its net sales:

Variable costs are expenses directly tied to production volume, such as raw materials, direct labor, and variable overhead, which rise or fall as output changes. Such costs are essential in cost behavior analysis, which helps businesses understand financial dynamics across different activity levels.

A common application is break-even analysis, where the break-even point in units is calculated by dividing fixed costs by the contribution margin per unit (sales price minus variable cost). Understanding variable costs enables better pricing, budgeting, and decision-making, especially when optimizing operations or improving profitability.

A key aspect is the variable cost ratio (VCR) or the portion of net sales consumed by variable costs. VCR is a crucial profitability tool: a high ratio signals lower margins and higher volatility, while a low ratio suggests stronger margins and fixed-cost leverage.

Thank you for reading CFI’s guide to Variable Costs. To keep advancing your career, the additional resources below will be useful: