Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

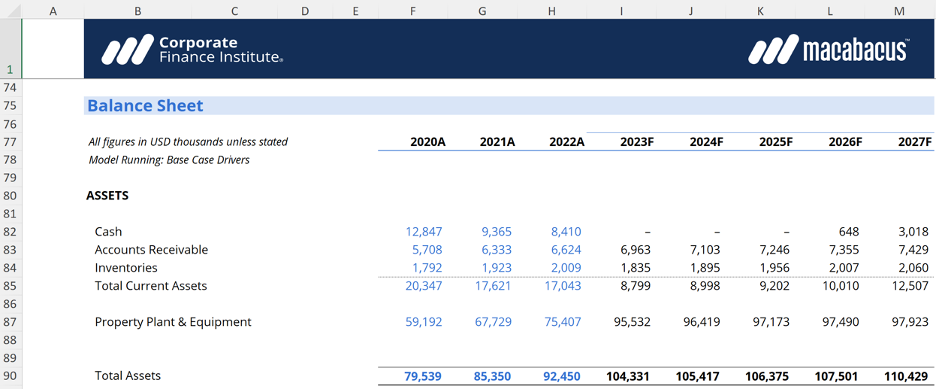

A key current asset account

Inventory is a current asset account found on the balance sheet, consisting of all raw materials, work-in-progress, and finished goods that a company has accumulated. It is often deemed the most illiquid of all current assets and, thus, it is excluded from the numerator in the quick ratio calculation.

There is an interplay between the inventory account and the cost of goods sold in the income statement — this is discussed in more detail below.

The ending balance of inventory for a period depends on the volume of sales a company makes in each period.

The basic formula for ending inventory is:

Ending Inventory = Beginning Balance + Purchases – Cost of Goods Sold

Higher sales (and thus higher cost of goods sold) leads to draining the inventory account. The conceptual explanation for this is that raw materials, work-in-progress, and finished goods (current assets) are turned into revenue. The cost of goods flows to the income statement via the cost of goods sold (COGS) account.

Ending inventory is also determined by the accounting method for cost of goods sold. There are four main methods of inventory calculation: FIFO (“first in, first out”), LIFO (“last in, first out”), weighted average, and specific identification. These all have certain criteria to be applied, and some methods may be prohibited in certain countries under certain accounting standards.

In an inflationary period, LIFO will generate higher cost of goods sold than the FIFO method will. As such, using the LIFO method would generate a lower inventory balance than the FIFO method would. This must be kept in mind when an analyst is analyzing the inventory account.

Finished goods inventory is inventory that has been completely built and is ready for immediate sale. Regardless of the inventory cost method mentioned above, finished goods inventory consists of the raw material cost, direct labor, and an allocation of overhead.

Work-in-progress inventory consists of all partially completed units in production at a given point in time.

Raw materials inventory is any material directly attributable to the production of finished goods, but on which work has not yet begun. An example would be steel for a car manufacturer.

Below is an example from Procter & Gamble’s 2022 annual report (10-K), which shows a breakdown of its inventory by component. In fiscal 2022, P&G had materials and supplies (raw materials) of approximately $2.2 billion, work-in-process of $856 million, and finished goods of $3.9 billion.

The type of accounting system used affects the value of the account on the balance sheet. Periodic inventory systems determine the LIFO, FIFO, or weighted average value at the end of every period, whereas perpetual systems determine the inventory value after every transaction.

Because of the varying time horizons and the possibility of differing costs, using a different system will result in a different value. Analysts must account for this difference when analyzing companies that use different inventory systems.

The average inventory balance between two periods is needed to find the turnover ratio, as well as to determine the average number of days required for inventory turnover. In these calculations, either net sales or cost of goods sold can be used as the numerator, although the latter is generally preferred, as it is a more direct representation of the value of the raw materials, work-in-progress, and finished goods ready for sale.

Accounts payable turnover requires the value for purchases as the numerator. This is indirectly linked to the inventory account, as purchases of raw materials and work-in-progress may be made on credit — thus, the accounts payable account is impacted.

Free Accounting Fundamentals Course