Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Do the company’s current assets easily cover its current liabilities?

The Quick Ratio, also known as the Acid-test or Liquidity ratio, measures a business’s ability to pay its short-term liabilities by using assets that are readily convertible into cash. These assets are, namely, cash, marketable securities, and accounts receivable. These assets are known as “quick” assets because they can be converted into cash quickly.

Quick Ratio = [Cash & Equivalents + Marketable Securities + Accounts Receivable] / Current Liabilities

Or, alternatively,

Quick Ratio = [Current Assets – Inventory – Prepaid expenses] / Current Liabilities

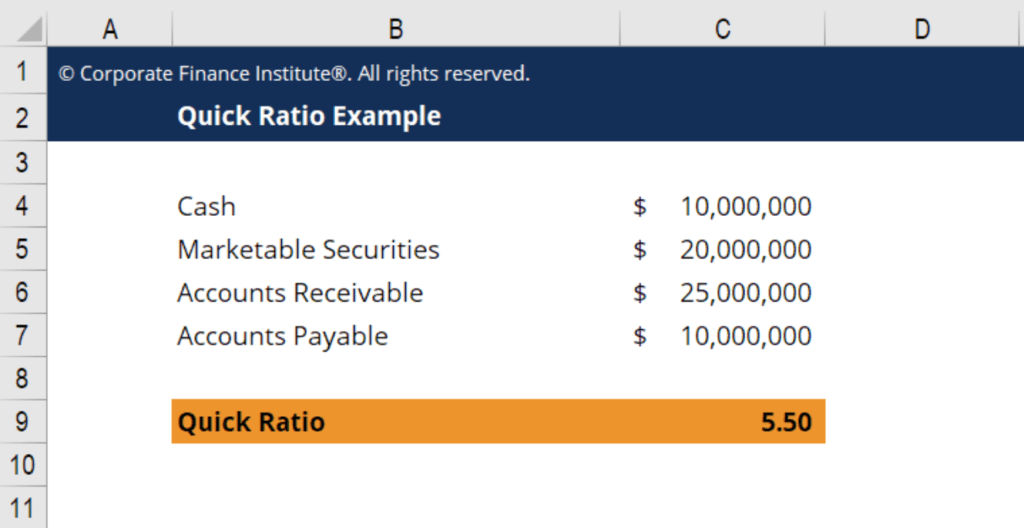

For example, let’s assume a company has:

This company has a liquidity ratio of 5.5, which means that it can pay its current liabilities 5.5 times over using its most liquid assets. A ratio above 1 indicates that a business has enough cash or cash equivalents to cover its short-term financial obligations and sustain its operations.

The formula in cell C9 is as follows = (C4+C5+C6) / C7

This formula takes cash, plus securities, plus AR, and then divides that total by AP (the only liability in this example).

The result is 5.5.

Click the button below to download CFI’s free Quick Ratio template!

Generally speaking, the ratio includes all current assets, except:

As you can see, the ratio is clearly designed to assess companies where short-term liquidity is an important factor. Hence, it is commonly referred to as the Acid Test.

The quick ratio focuses on the most liquid assets, yet it still differs from pure cash availability—illustrating the concept of cash vs liquidity.

The quick ratio is a barometer of a company’s ability to pay its current obligations. Investors, suppliers, and lenders are more interested in knowing if a business has more than enough cash to pay its short-term liabilities rather than when it does not. Having a well-defined liquidity ratio is a signal of competence and sound business performance that can lead to sustainable growth.

To learn more about this ratio and other important metrics, check out CFI’s course on performing financial analysis.

The quick ratio is different from the current ratio, as inventory and prepaid expense accounts are not considered in the quick ratio because, generally speaking, inventories take longer to convert into cash, and prepaid expense funds cannot be used to pay current liabilities.

For some companies, however, inventories are considered quick assets; it depends entirely on the nature of the business, but such cases are extremely rare.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to Quick Ratio. To keep learning and advancing your career as a financial analyst, these additional CFI resources will help you on your way: