Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Usually the most liquid of all assets. The quickest of quick assets, the most current of current assets.

Let’s begin by defining cash itself: cash includes legal tender, bills, coins, checks received but not deposited, and checking and savings accounts. Cash equivalents are low-risk, short-term investment securities with maturity periods of 90 days (three months) or less. These include bank certificates of deposit, banker’s acceptances, Treasury bills, commercial paper, and other money-market instruments.

As an example, here is how Amazon defines cash equivalents:

Cash and cash equivalents differ from other current assets, like marketable securities and accounts receivable, based on their nature. However, certain marketable securities may be classified as cash equivalents, depending on the accounting policy of a company.

The definition of cash by companies is consistent with how most people think of as cash. This includes not only actual cash currency on hand but demand deposits with banks or other financial institutions.

Cash also includes other accounts that are similar in nature to demand deposits, if applicable. These accounts should allow the customer complete flexibility in both depositing and withdrawing funds at any time, without prior notice or penalty.

Basically, to qualify as cash, the funds effectively need to be available for immediate use.

On the other hand, cash equivalents are short-term, highly liquid investments that are not yet immediately available for use.

Cash equivalents usually have both of the following characteristics:

Generally, only investments with original maturities of three months or less qualify as cash equivalents. By original maturity, we mean the original maturity from the point of investment.

For example, investing in a three-month United States Treasury bill or a three-year U.S. Treasury note purchased three months before maturity both qualify as cash equivalents. However, a Treasury note purchased ten years ago does not become a cash equivalent when its remaining maturity is three months (the original maturity was ten years at the time of investment).

The definition of cash equivalents presumes these are highly liquid investments. Highly liquid investments are redeemable upon demand without significant penalties, traded on an established market, and/or have the ability to be converted into cash within normal processing time without significant penalties or disruptions to market prices.

This is important because even if an investment matures in three months or less, if it cannot be readily converted into cash, then it would not be considered a cash equivalent. Similarly, an investment that is readily convertible into cash, but has a maturity greater than three months, is also not considered a cash equivalent, barring unique features like a put option that will be redeemed within three months.

A detailed list of cash equivalents includes the following items:

A banker’s acceptance is a financial instrument that represents a promised future payment from a bank. These are traded in a liquid secondary market and are very similar to other short-term debt instruments. Banker’s acceptances generally mature within 30 to 180 days.

Commercial paper is a short-term, unsecured debt obligation primarily issued by financial institutions and large corporations. It is a money market instrument that generally comes with a maturity of up to 270 days.

The difference between commercial paper and a banker’s acceptance is that a bank issues commercial paper as a source of financing itself. A banker’s acceptance is just the promise of a bank to pay one party on behalf of another party.

Treasury bills (or T-Bills for short) are short-term financial instruments issued by the United States Government. T-bills have maturity periods ranging from a few days up to 52 weeks (one year). These instruments are considered among the safest investments since they are backed by the full faith and credit of the US Government.

Money market funds are fixed income mutual funds that invest in short-term debt securities, such as Treasury bills, municipal bills, and short-term corporate and bank debt instruments that come with low credit risk and high liquidity.

A certificate of deposit (CD) is a product offered by a financial institution like a bank or credit union. CDs allow customers to earn interest income on their deposits. In return, the deposits remain untouched for a certain period of time and are subject to a penalty if funds are withdrawn early.

Companies may elect to classify some types of their marketable securities as cash equivalents. This depends on the liquidity of the investment and what the company intends to do with such products. Typically, this will be disclosed in the footnotes of a company’s financial statements.

Investments in longer-term liquid securities, such as stocks, bonds, and derivatives, are not normally included in cash and cash equivalents. Even though such assets may be easily turned into cash, they are still not usually considered cash equivalents. Instead, most marketable securities are listed as investments (assets) on a balance sheet.

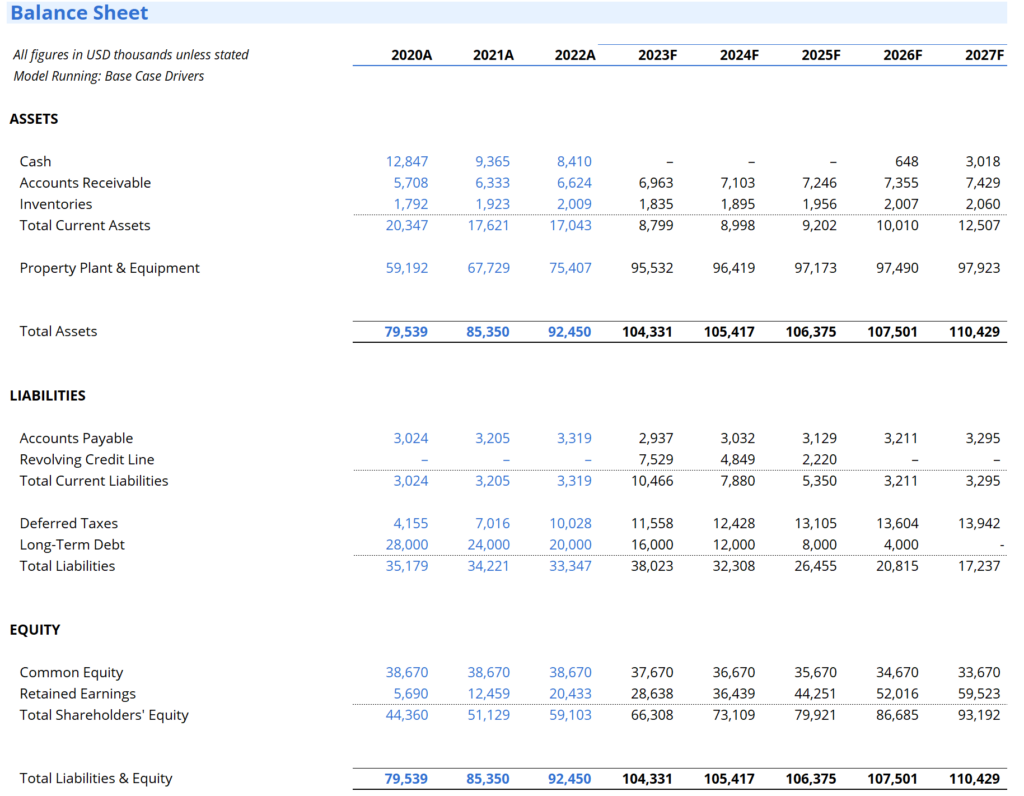

Cash and cash equivalents are part of the current assets section of the balance sheet and contribute to a company’s net working capital (NWC). Net working capital is equal to current assets less current liabilities.

Working capital is important for funding a business in the short term (12 months or less) and can be used to help finance inventory, operating expenses, and capital purchases.

In financial modeling and valuation, cash is king. Financial analysts spend a lot of their time “undoing” the work of accountants (accruals, matching, etc.) to arrive at the cash flow of a business.

When building a financial model, cash is typically the last item to be completed and will reveal whether or not the balance sheet balances and if the model is working properly.

When building a financial model, cash is typically the last item to be completed and will reveal whether or not the balance sheet balances and if the model is working properly.

When a company has excess cash, it will usually invest the excess amounts. One of the most common investments is in cash equivalents. These are short-term, low-risk instruments that are easily convertible into cash. Since these investments are low risk and so close to maturity, they are practically as good as cash in the bank, which is why they are called “cash equivalents.”

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide on Cash Equivalents. To keep advancing your career and skills, the following CFI resources will be useful: