Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

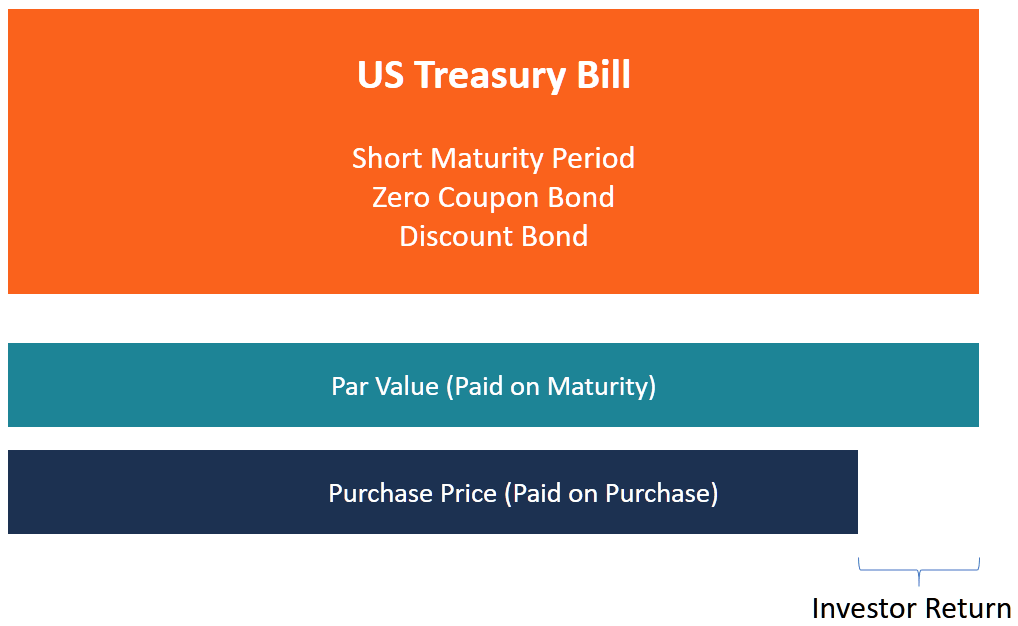

Financial instruments issued by the U.S. Treasury with maturity periods less than 1 year

Treasury Bills (or T-Bills for short) are a short-term financial instrument that is issued by the US Government’s Department of the Treasury. T-Bills have maturity periods ranging from a few days up to 52 weeks (one year) and are issued regularly by the US Treasury. They make up a large proportion of the entire universe of Money Market securities.

They are considered among the safest investments since they are backed by the full faith and credit of the United States Government. As such, Treasury Bills are not only an important vehicle for traders and investors to invest for short amounts of time, they are also used as a baseline for other investment returns.

When an investor buys a Treasury Bill, they are lending money to the government. The US Government uses the money to fund its debt and pay ongoing expenses such as salaries and military equipment. The regular auctions of new T-Bills helps to refinance the maturing T-Bills and for any extra borrowing the Government needs.

T-Bills are sold in denominations ranging from $1,000 for retail investors up to billions of dollars for the largest institutional investors and can be purchased in the primary and secondary markets.

Treasury bills are sold at a discount to the par value, which can be thought of as the maturity amount. For example, a one year Treasury bill with a par value of $1,000,000 may be sold for $950,000. The US Government, through the Department of Treasury, promises to pay the investor the full par value of $1,000,000 of the T-bill at its specified maturity date.

In this example, the investor earns $50,000 for investing $950,000 for a year, pocketing a total of $1,000,000 upon maturity of the T-Bill in one year’s time.

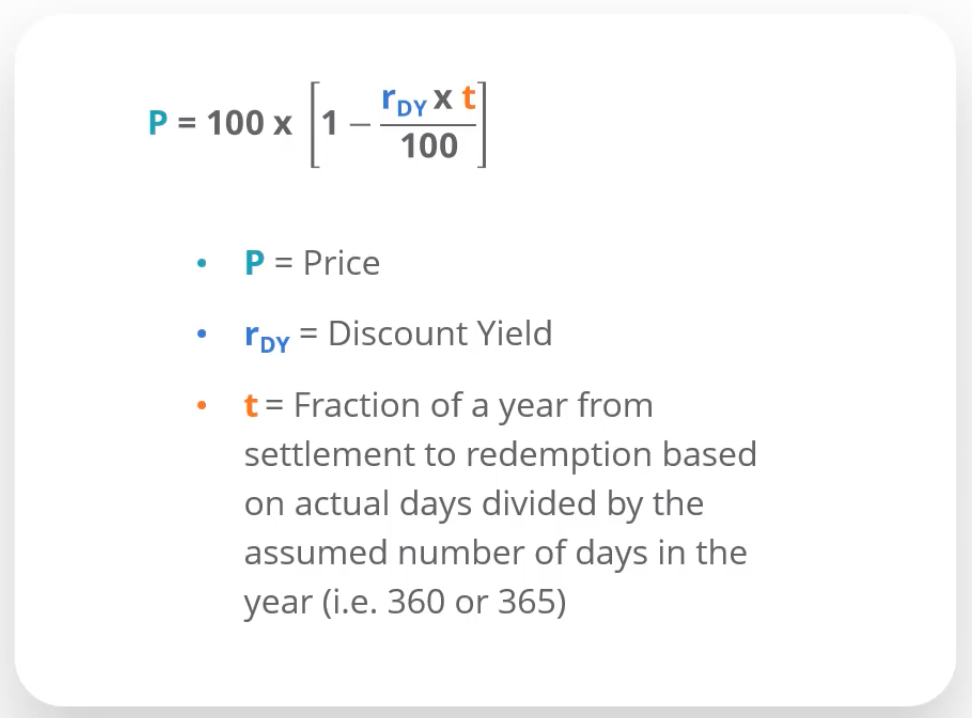

The difference between the face value of the T-bill and the amount that an investor pays is called the discount rate or discount yield, which is calculated as a percentage. In this case, the discount yield is 5% for this one year T-Bill. The formula for calculating discount yield is as follows:

T-Bill reference rates can be obtained directly from the US Treasury website.

Treasury bills can be purchased in the following three ways:

In a non-competitive bid, the investor agrees to accept the discount rate determined at auction. The yield that an investor receives is equal to the average auction price for T-Bills sold at auction. Individual investors prefer this method since they are guaranteed to receive the full amount of the bill at the expiry of the maturity period. Payment is made through TreasuryDirect or the investor’s bank or broker.

In a competitive bidding auction, investors buy T-Bills at a specific discount rate that they are willing to accept. Every submitted bid states the lowest rate or discount margin that the bidder/investor is willing to accept. Bids accepting the lowest discount rate are accepted first.

If there are not enough bids at that level to make the issue fully subscribed, then bids at the next lowest rate are accepted. The process continues until the entire issue has been sold. Purchase payments must be made either through a bank or a broker.

Investors can buy or sell Treasury Bills on the secondary market from market makers, such as Retail and Investment Banks. These institutions would charge a bid/offer margin in order to make the trade profitable for them. Mutual funds (called Money Market Funds) and Exchange-Traded Funds (ETFs) actively invest in T-Bills as well as investors who are looking for a safe place to park their cash.

Like other types of debt securities, the price of T-Bills and the return for investors may be affected by various factors such as macroeconomic conditions, investor risk tolerance, inflation, monetary policy, and specific supply and demand conditions for T-Bills.

The Federal Reserve’s monetary policy is likely to affect the T-Bill price. T-Bill interest rates tend to move closer to the interest rate set by the Fed, known as the Fed(eral) Funds Target Rate (“Fed Funds Rate”). However, a rise in the Fed Funds Rate means that existing T-Bill prices must fall in order to make these securities attractive to investors, who can choose to buy newly issued T-Bill at higher rates instead.

The maturity period of a T-Bill affects its price. For example, a one-year T-Bill typically comes with a higher rate of return than a three-month T-Bill. The explanation for this is that longer maturities mean additional risk for investors in a normal rate environment.

For example, a $1,000 T-Bill may be sold for $970 for a three-month T-Bill, $950 for a six-month T-Bill, and $900 for a twelve-month T-Bill. Investors demand a higher rate of return to compensate them for tying up their money for a longer period of time.

An investor’s risk tolerance levels also affect the price of a T-Bill. When the U.S. economy is going through an expansion and other debt securities are offering a higher return, T-Bills are less attractive and will, therefore, be priced lower. However, when the markets and the economy are volatile and other debt securities are considered riskier, T-Bills command a higher price for their “safe haven” quality.

The price of T-Bills can also be affected by the prevailing rate of inflation as inflation eats away at the real purchasing power of the T-Bill. For example, if the inflation rate stands at 5% and the T-Bill discount rate is 3%, it becomes uneconomical to invest in T-Bills since the real rate of return will be a loss. The effect of this is that there is less demand for T-Bills, and their prices will drop.

T-Bills, T-Notes, and T-Bonds are fixed-income investments issued by the US Department of the Treasury when the government needs to borrow money. They are all commonly referred to as “Treasuries.” The Treasury Department spreads out their borrowing over various maturities to ensure prudent debt management.

Treasury Bills have a maturity of one year or less, and they do not pay interest before the expiry of the maturity period. They are sold in auctions at a discount from the par value of the Bill and are most commonly offered with maturities of 28 days (one month), 91 days (3 months), 182 days (6 months), and 364 days (one year).

Treasury Notes have a maturity period of two to ten years. They come in denominations of $1,000 and offer coupon payments every six months. The 10-year T-Note is the most frequently quoted Treasury when assessing the performance of the bond market. It is also used to show the market’s take on macroeconomic expectations.

Treasury Bonds have the longest maturity among the three Treasuries. They have a maturity period of between 20 years and 30 years, with coupon payments every six months. T-bond offerings were suspended for four years between February 2002 and February 2006 but were resumed due to demand from pension funds and other long-term institutional investors.

Thank you for reading CFI’s guide on Treasury Bills (T-Bills). To continue learning and advancing your career, these additional resources will be helpful: