Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Assessing how a company accumulates its cash

A quality of earnings report is a routine step in the due diligence process for private acquisitions. The report assesses how a company accumulates its revenues – such as cash or non-cash, recurring or nonrecurring.

Net income is not necessarily a 100% accurate indication of financial performance for a business. If a company reports large net income figures but negative operating cash flow, for example, then it may not be as financially sound as it appears.

There are many key details that are not outlined in a company’s income statements – therefore, a breakdown of cash sources is very important. Quite simply, if a company reports a positive net income but poor quality earnings, then acquiring the company may be a more risky investment than the company’s financial statements indicate. This assessment often affects whether or not an acquirer decides to pursue a private acquisition.

The following is an example of an abridged version of a hypothetical due diligence quality of earnings review conducted when fictional company, XYZ Capital Partners, decides to acquire the privately held ABC Co and partially acquire DEF Co (ABC’s sister company).

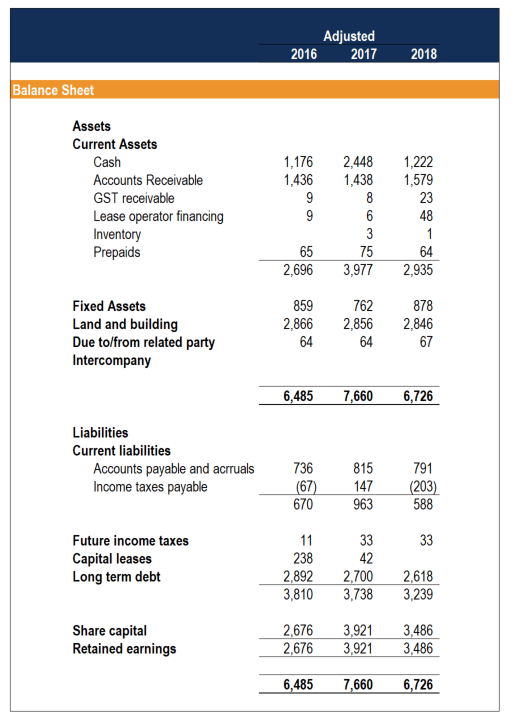

The review is being completed by external auditors QRS LLP. It is separated into three sections: (1) an executive summary, (2) income statement, and (3) the balance sheet.

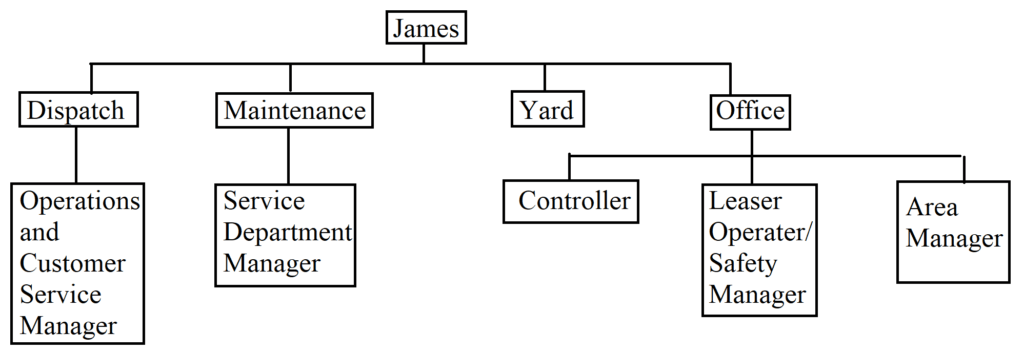

ABC Co. is based in Buffalo, NY and was founded in 2000 by James Smith. ABC provides nationwide moving services that include labor, hauling, and moving. There are five managers who are part of senior management and the company hierarchy is as follows:

In this deal, XYZ will also purchase components of ABC’s sister company, DEF, in order to gain control of certain fixed assets pertinent to the acquisition.

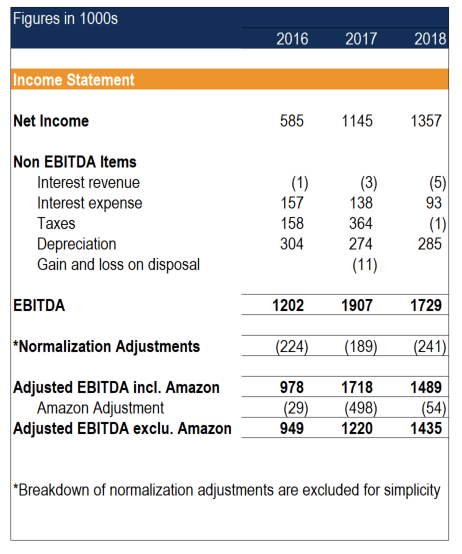

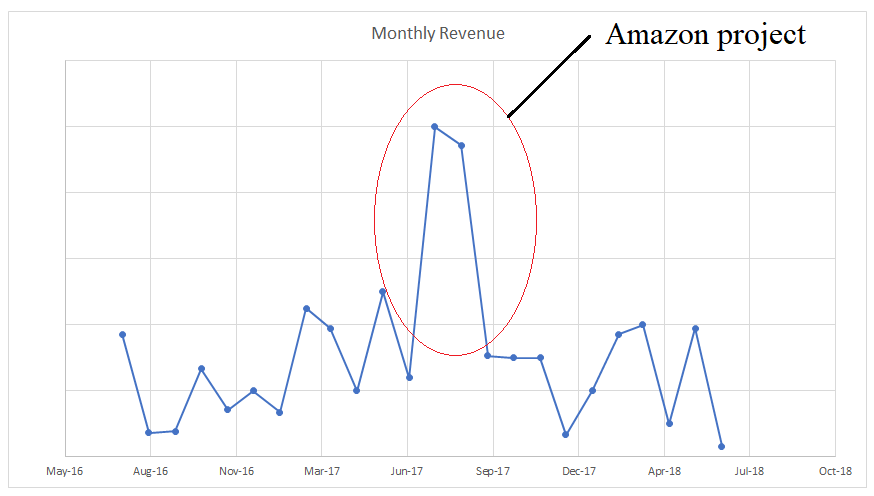

XYZ’s letter of intent includes an acquisition of all the assets of ABC and some other operating assets by DEF for the sum of $6 million. The $6 million represents a 4.23x multiple on EBITDA before adjustments for Amazon-related revenue (a large non-recurring revenue source that appeared when they moved to their Buffalo, NY office over a three-year period), the multiple is 4.39x adjusted EBITDA.

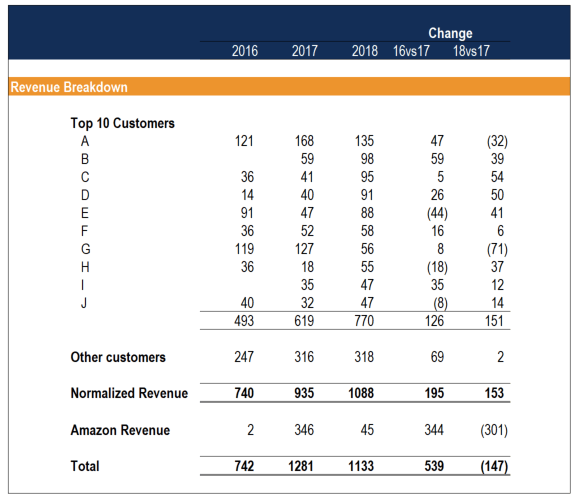

| Revenue and Amazon | ABC normally undertakes a few larger projects that occur each year. However, in in 2017 , ABC was awarded a contract by Amazon that was much larger than normal. | Although the Amazon project was unusual due to its size, ABC may be able to take advantage of future one-time large orders as they are now on the supplier list for Amazon. XYZ Capital Partners should follow Amazon’s Vancouver development closely as it may be able to pick up additional large orders. |

| QRS reviewed revenues for 2017 to determine if any large one-time revenues were incurred similar to Amazon. QRS noted that there were no large revenue increases and all customers in the top 10 reported revenues for at least two 2 consecutive years. |

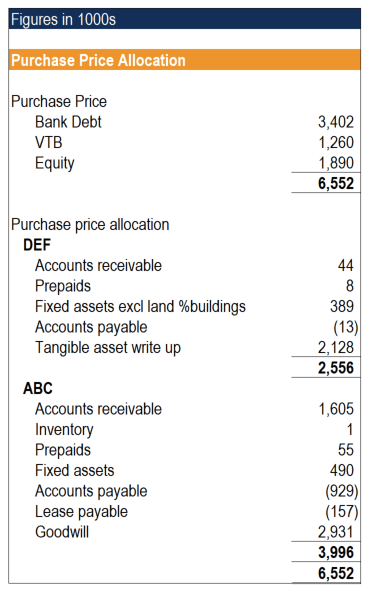

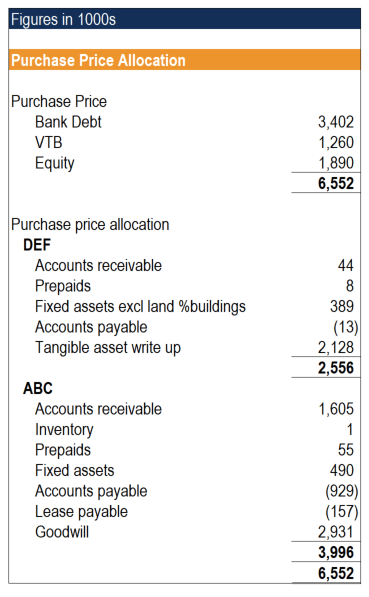

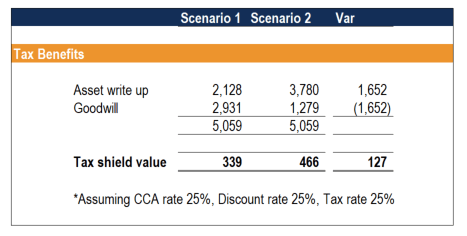

| Purchase Price Allocation | XYZ should allocate as much of the purchase price as possible to tangible assets in order to take advantage of a faster write-off of those assets for tax purposes. QRS estimates that the value of the tax shield to Pender West would increase by $100,800 if an additional $1.26 million of value were allocated to tangible assets. | XYZ should determine the real fair market value for the assets to be purchased and see if it can negotiate any further value to be allocated to the tangible assets in order to increase the tax shield created through this transaction. |

The above example is merely an executive overview of how a quality of earnings review appears and the type of financial statement analysis involved. Other possible issues and recommendations an external auditor may bring up include things such as normalizing earnings, addressing payroll inefficiencies, or implementing a new IT system.

Notice the important issues here. In 2017, a large proportion of ABC’s net income came from a single large order from Amazon. Without a quality of earnings report, ABC’s value could appear greatly inflated.

Many acquisition transactions fail during the due diligence process as the reviews highlight the key failings of a target company that would not have been discovered without an external audit. Consulting services are of critical importance because they also provide recommendations on how to hedge potential business risks and take advantage of potential gains (such as tax benefits).

Note that this assessment is purely recommendation-based. The recommendations in a quality of earnings report constitute professional analysis and advice but are not required to be followed by either the acquirer or the target company.

Thank you for reading CFI’s guide to the quality of earnings report. CFI is the official provider of the Financial Modeling & Valuation Analyst certification. To continue learning and advancing your career, these additional CFI resources will be helpful: