Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

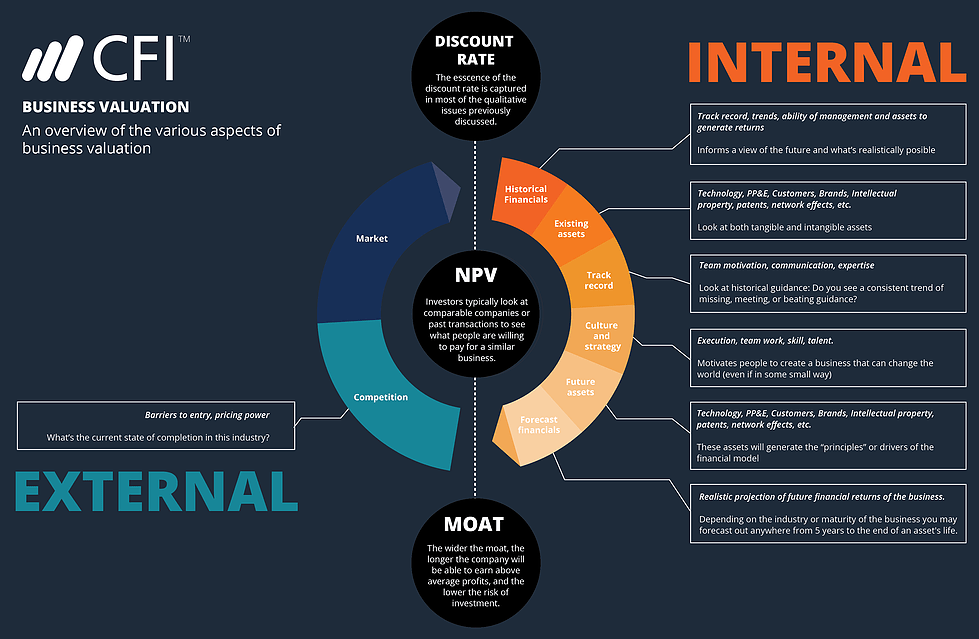

Methods for valuing private companies

Private company valuation is a set of valuation methodologies used to determine the intrinsic value of a private company. For public companies, we can easily observe the stock price and source the number of shares outstanding from filings. The market value of the public company, also called market capitalization, is the product of the stock price and the shares outstanding.

Such an approach, however, will not work with private companies, since information regarding their stock price is not publicly listed. Moreover, as privately held firms often are not required to operate by the stringent accounting and reporting standards that govern public firms, their financial statements may be inconsistent and unstandardized and, as such, are more difficult to interpret.

Here, we will introduce three common methods for valuing private companies, using data available to the public.

Comparable company analysis (also called “trading comps”) is a relative valuation method in which you compare the current value of a business to other similar businesses by looking at trading multiples like P/E, EV/EBITDA, or other multiples.

The “comps” valuation method provides an observable value for the business, based on what other comparable companies are currently worth. Comps is the most widely used approach, as the multiples are easy to calculate and always current. The logic follows that if company X trades at a 10-times P/E ratio, and company Y has earnings of $2.50 per share, company Y’s stock must be worth $25.00 per share (assuming the companies have similar risk and return characteristics).

Enterprise Value of target firm = EV/EBITDA Multiple x EBITDA of the target firm

or

Equity Value of target firm = P/E Multiple x Net Income of the target firm

The EBITDA and/or Net Income used to value the target firm may be based on historicals (LTM or Last Twelve Months) or a projected number.

The image shown above is a Comps Table from CFI’s Comparable Valuation Analysis Course.

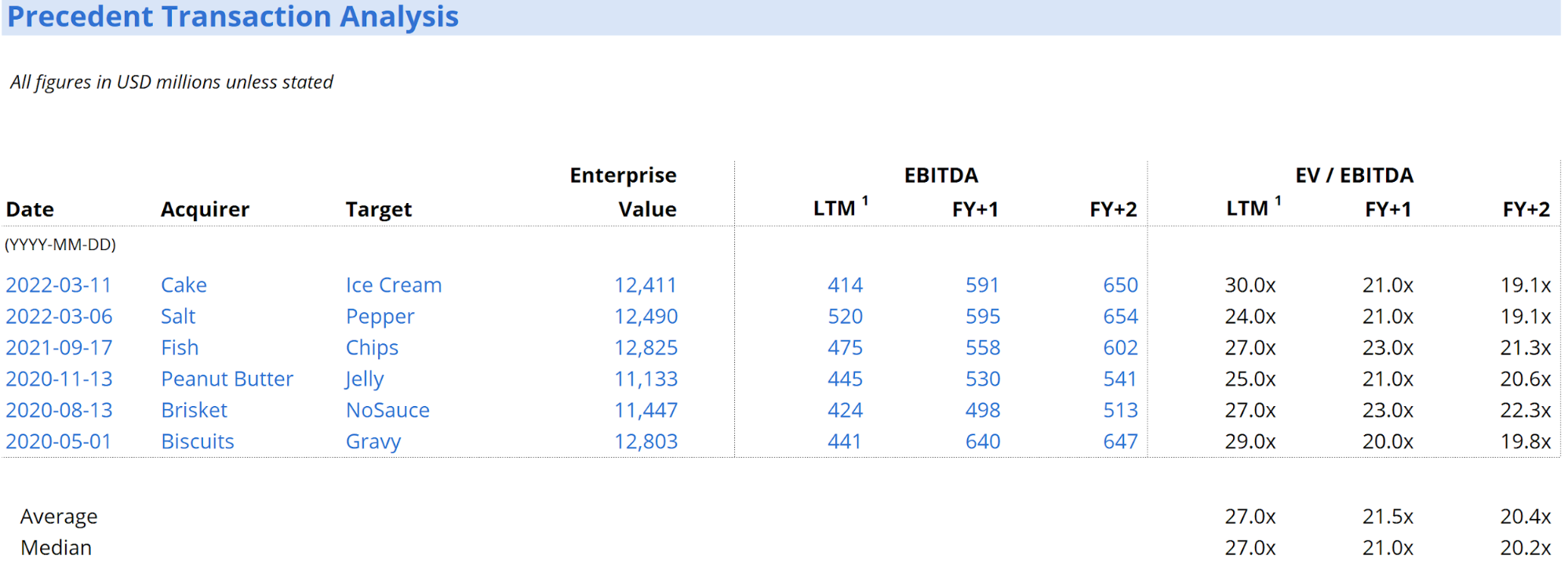

Precedent transactions analysis is another form of relative valuation where you compare the company in question to other businesses that have recently been sold or acquired in the same industry. These transaction values include the take-over premium included in the price for which they were acquired.

The values represent the entire value of a business and not just a small stake. They are useful for M&A transactions but can easily become dated and no longer reflective of current market conditions as time passes.

Discounted Cash Flow (DCF) analysis is an intrinsic value approach where an analyst forecasts a business’s unlevered free cash flow into the future and discounts it back to today at the firm’s Weighted Average Cost of Capital (WACC).

A DCF analysis is performed by building a financial model in Excel and requires an extensive amount of detail and analysis. It is the most detailed of the three approaches and requires the most estimates and assumptions. Therefore, the effort required to preparing a DCF model may also often result in the least accurate valuation due to the sheer number of inputs. However, a DCF model allows the analyst to forecast value based on different scenarios and even perform a sensitivity analysis.

The formula for unlevered free cash flow is:

Free cash flow = EBIT (1-tax rate) + (depreciation) + (amortization) – (change in net working capital) – (capital expenditure)

We usually use the firm’s weighted average cost of capital (WACC) as the appropriate discount rate. To derive a firm’s WACC, we need to know its cost of equity, cost of debt, tax rate, and capital structure. Cost of equity is calculated using the Capital Asset Pricing Model (CAPM). We estimate the firm’s beta by taking the industry average beta. Cost of debt is dependent on the private company’s credit profile, which affects the interest rate at which it incurs debt.

We also refer to the target’s public peers to find the industry norm of tax rate and capital structure. Once we have the weights of debt and equity, cost of debt, and cost of equity, we can derive the WACC.

With all the above steps completed, the valuation of the target firm can be calculated as:

It should be noted that performing a DCF analysis requires significant financial modeling experience. The best way to learn financial modeling is through practice and direct instruction from a professional. CFI’s financial modeling course is one of the easiest ways to learn this skill.

The First Chicago Method is a combination of the multiple-based valuation method and the DCF method. The distinct feature of this method lies in its consideration of various scenarios of the target firm’s payoffs.

Usually, this method involves the construction of three scenarios: a best-case, a base-case (the most likely scenario), and a worst-case scenario. A probability is assigned to each case. The ultimate valuation is the probability-weighted sum of each of the three scenarios.

This private company valuation method can be used by venture capitalists and private equity investors as it provides a valuation that incorporates both the firm’s upside potential and downside risk.

Investors prefer liquid companies. Therefore, a publicly traded company should be worth more than a similar private company. Because of that preference, any private company valuation done using publicly traded data should be further discounted for a lack of liquidity and/or marketability.

For example, if a private company is valued at $100 million using comparable company analysis, but the analyst thinks there is a discount for lack of marketability of 30%, then the private company is really worth $70 million [$100 million x (1 – 30%)]. Read more about the discount for lack of marketability here.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.