Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

How quickly an investment can be sold without impacting its price

In financial markets, liquidity refers to how quickly an investment can be sold without negatively impacting its price. The more liquid an investment is, the more quickly it can be sold (and vice versa), and the easier it is to sell it for fair value or current market value. All else being equal, more liquid assets trade at a premium and illiquid assets trade at a discount.

In accounting and financial analysis, a company’s liquidity is a measure of how easily it can meet its short-term financial obligations.

Below is an example of how many common investments are typically ranked in terms of how quickly and easily they can be turned into cash (of course, the order may be different depending on the circumstances).

As you can see in the list above, cash is, by default, the most liquid asset since it doesn’t need to be sold or converted (it’s already cash!). Stocks and bonds can typically be converted to cash in about 1-2 days, depending on the size of the investment. Finally, slower-to-sell investments such as real estate, art, and private businesses may take much longer to convert to cash (often months or even years).

Items on a company’s balance sheet are typically listed from the most to the least liquid. Therefore, cash is always listed at the top of the asset section, while other types of assets, such as Property, Plant & Equipment (PP&E), are listed last.

In finance and accounting, the concept of a company’s liquidity is its ability to meet its financial obligations. The most common measures of liquidity are:

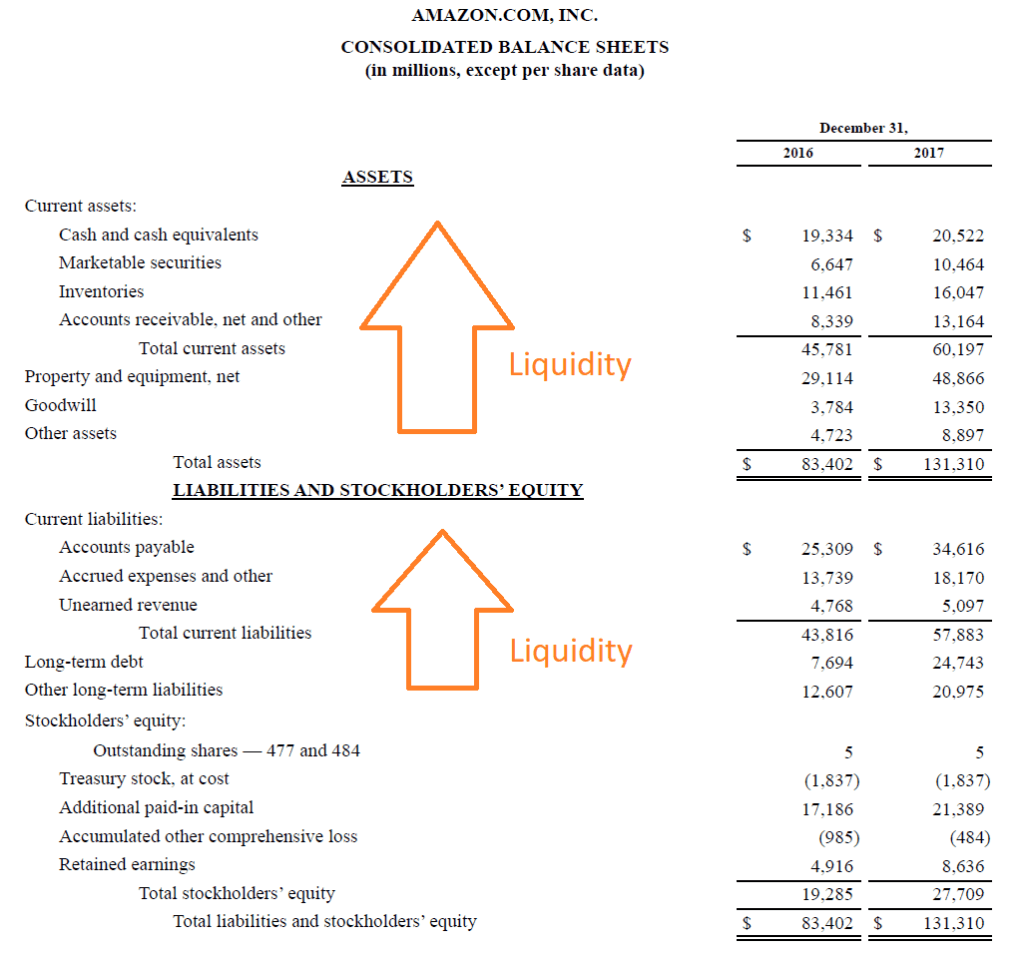

Below is a screenshot of Amazon’s 2017 balance sheet, which displays its assets and liabilities in order of their liquidity, as well as its stockholders’ equity.

As you can see in the image, Amazon’s assets are separated into two categories, current assets and non-current assets (everything else).

Current assets are as follows:

For most companies, these are four of the most common current assets. Their liquidity, however, can vary. For many companies, accounts receivable is more liquid than inventories (meaning the company expects to receive payment from customers faster than it takes to sell products in inventory).

Current liabilities are listed as follows:

To learn more, check out CFI’s Advanced Financial Modeling Course on Amazon.

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful: