Get In-Demand Finance Certifications

Models used to value companies by comparing them to other businesses based on certain financial metrics

Relative valuation models are used to value companies by comparing them to other businesses based on certain metrics such as EV/Revenue, EV/EBITDA, and P/E ratios. The logic is that if similar companies are worth 10x earnings, then the company that’s being valued should also be worth 10x its earnings. This guide will provide detailed examples of how to perform relative valuation analysis.

There are two common types of relative valuation models: comparable company analysis and precedent transactions analysis. Below is a detailed explanation of each method:

Comparable company analysis, or “Comps” for short, is commonly used to value firms by comparing them to publicly traded companies with similar business operations. An analyst will compare the current share price a public company relative to some metric such as its earnings to derive a P/E ratio. It will then use that ratio to value the company it is trying to determine the worth of.

The advantages of Comps are that they are always current, and it’s easy to find financial information on public companies.

Precedent transactions, or “Precedents” for short, is a method of valuing companies by looking at historical transactions where entire companies were bought or sold (mergers and acquisitions). These transactions show what an investor was willing to pay for the entire company. Precedents also use ratios, such as EV/EBTIDA.

Precedents are useful for valuing an entire business (including a takeover premium or control premium), but can quickly become out of date, and the information can be difficult to find.

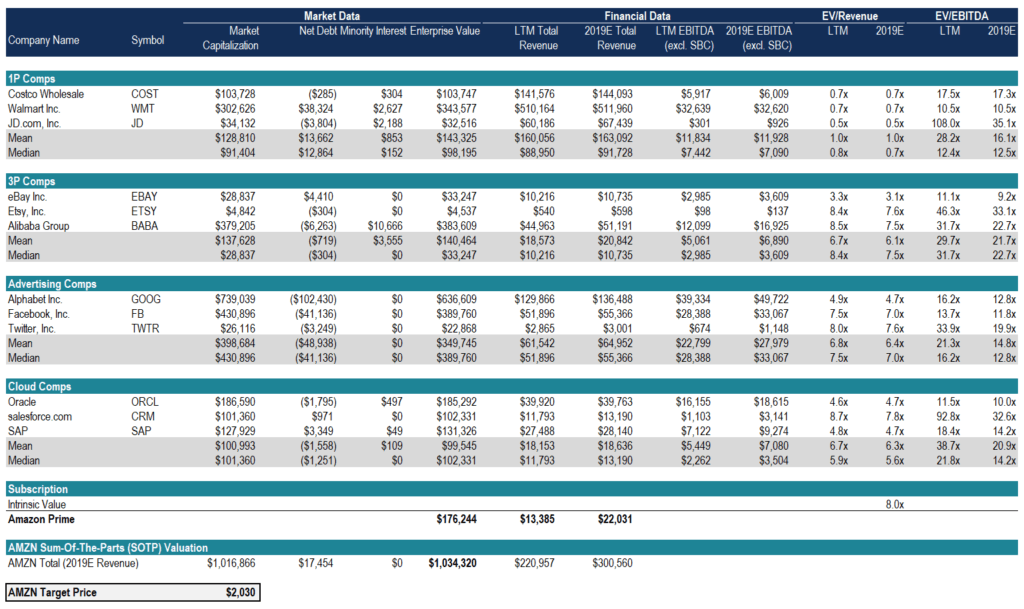

Below is an example of a relative valuation model from CFI’s Advanced Financial Modeling Course on Amazon. In the course, we use Amazon as a case study for performing a Sum Of The Parts (SOTP) analysis to value the online retailer.

As you can see in the screenshot, Amazon’s business is divided into several different segments: first-party sales (1P), third-party sales (3P), advertising, cloud computing, and subscription. For each of these segments, different publicly traded companies are used to gather trading multiples such as EV/Revenue and EV/EBITDA. Those trading multiples are then applied to Amazon’s revenue and EBITDA figures to determine the value of the entire business.

While relative valuation models seek to value a business by companies to other companies, intrinsic valuation models see to value a business by looking only at the company on its own.

The most common intrinsic valuation method is Discounted Cash Flow (DCF) analysis, which calculates the Net Present Value (NPV) of a company’s future cash flow.

The benefits of a DCF model are that it includes lots of detail about the company’s business and isn’t concerned with how other companies are performing. The drawbacks are that many assumptions are required, and the company’s value is very sensitive to changes in some of those key assumptions.

To learn more, check out CFI’s various financial modeling courses.

Thank you for reading CFI’s guide to Relative Valuation Models. To learn more, these additional resources will be helpful:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: