Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

This article outlines an example of a Letter of Intent (LOI)

A Letter of Intent (LOI) is a short non-binding contract that precedes a binding agreement, such as a share purchase agreement or asset purchase agreement (definitive agreements). There are some provisions, however, that are binding such as non-disclosure, exclusivity, and governing law.

The main points that are typically included in a letter of intent include:

Letters of intent are often produced by investment bankers on behalf of corporate issuers. Below is an example of an LOI template. We discuss the sections of an LOI in italics below.

The introduction always references the relevant parties, as well as a discussion of why the potential buyer wants to do a transaction. The buyer may also discuss what it does in more detail and how it believes the proposed transaction is valuable. Below is an example of the introductory remarks in a letter of intent.

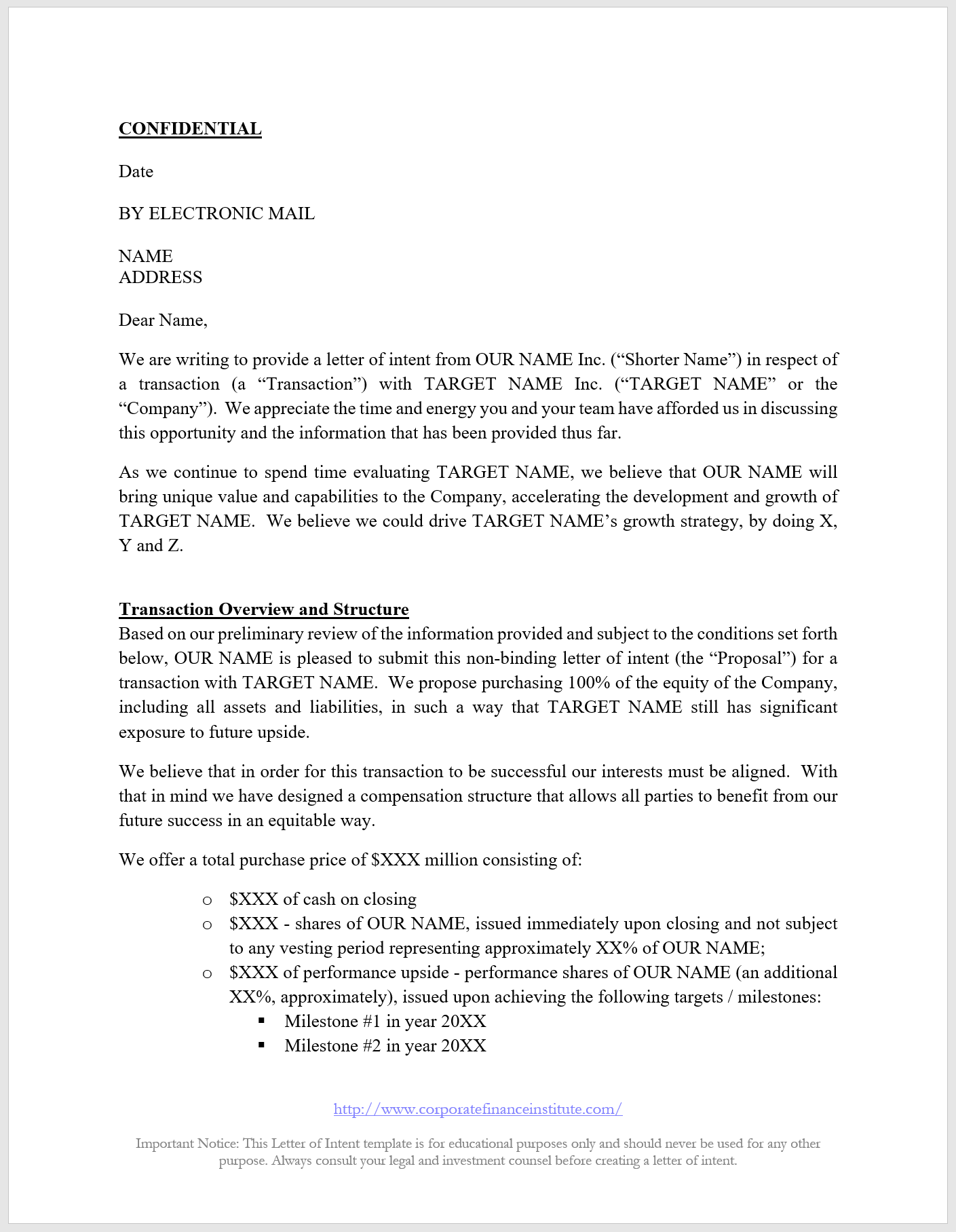

Date

BY ELECTRONIC MAIL

NAME

ADDRESS

Dear Name,

We are writing to provide a letter of intent from OUR NAME Inc. (“Shorter Name”) in respect of a transaction (a “Transaction”) with TARGET NAME Inc. (“TARGET NAME” or the “Company”). We appreciate the time and energy you and your team have afforded us in discussing this opportunity and the information that has been provided thus far.

As we continue to spend time evaluating TARGET NAME, we believe that OUR NAME will bring unique value and capabilities to the Company, accelerating the development and growth of TARGET NAME. We believe we could drive TARGET NAME’s growth strategy, by doing X, Y, and Z.

Here the potential buyer outlines, at a high level, how it envisions to structure and pay for the deal. The buyer may communicate whether it would like to structure a deal as an asset deal or a stock deal. The buyer will also give an indicative offer value. This may be communicated in terms of absolute numbers (as shown below), or by reference to a valuation multiple. There is also usually a discussion on how the transaction would be financed. Below is an example of this section.

Based on our preliminary review of the information provided and subject to the conditions set forth below, OUR NAME is pleased to submit this non-binding letter of intent (the “Proposal”) for a transaction with TARGET NAME. We propose purchasing 100% of the equity of the Company, including all assets and liabilities, in such a way that TARGET NAME still has significant exposure to future upside.

We believe that in order for this transaction to be successful our interests must be aligned. With that in mind, we have designed a compensation structure that allows all parties to benefit from our future success in an equitable way.

We offer a total purchase price of $XXX million consisting of:

It can take several months from the LOI before the buyer can close the transaction. This section discusses the illustrative timeline as well as some further steps the acquirer needs before it can submit a final offer (due diligence and the preparation of legal documents).

Given the importance of timing for TARGET NAME in respect to this transaction we have proposed a high-level timeline as follows:

Since this LOI is not a final binding offer, the buyer will need to spend time and resources more thoroughly reviewing the target company. While some due diligence has been performed before the LOI is sent, further diligence is required so the buyer can become comfortable with the transaction, as well as narrowing down a purchase price.

This Transaction is of the highest priority for us, and we are prepared to proceed as quickly as possible; it is important that you make that same commitment to us before we expend additional time and resources pursuing this opportunity. OUR NAME has developed an investment thesis and an understanding of the business through our initial due diligence, including several conversations with management, as well as a preliminary data review. We envision our remaining due diligence would include, but would not be limited to, commercial, accounting, and financial due diligence, as well as customary legal, tax, and regulatory work. With the Company’s full cooperation, we believe we can expeditiously complete our due diligence and present TARGET NAME with a definitive agreement within eight weeks from the date our Proposal is accepted.

As mentioned above, the buyer will spend a lot of time and resources during the due diligence phase. Because of this, it is common to ask the target for exclusivity. This prevents the target from seriously engaging with another party, thereby potentially wasting the buyer’s efforts on this transaction.

However, if the target receives an unsolicited offer, there may be language in the LOI discussing when the target would communicate that offer to the potential buyer as well as a further discussion on whether the buyer will match the unsolicited offer or if the target will accept the unsolicited offer. If the target accepts the unsolicited offer, then the LOI would be terminated. The example below does not contain these provisions.

Both the buyer (and target) will also ask for confidentiality with regards to the transaction, as well as the due diligence.

If the Company is interested in pursuing the proposed Transaction, we would require sixty days of exclusivity (the “Exclusivity Period”) to finalize our due diligence and negotiate definitive documentation, subject to a 60-day extension if OUR NAME is working in good faith to consummate the transaction at the initial expiration date. In light of our Proposal’s premium valuation, we believe that granting exclusivity at this stage will benefit the Project and its Shareholders. In order to complete our due diligence and to secure the additional requisite capital, we will need reasonable access to Company information and the ability to share that information with our prospective equity partners and debt financing sources in a manner that protects the confidentiality of your information and our discussions. A draft form of the exclusivity and confidentiality agreement is enclosed as Exhibit A for your consideration (the “Exclusivity and Confidentiality Agreement”). We emphasize our desire to complete the proposed Transaction in an expeditious and efficient manner and our readiness to mobilize resources to move ahead quickly. To that end, and assuming we sign this letter in advance, we would suggest an organizational meeting as soon as possible to agree on the work plan during the Exclusivity Period.

This part of the LOI merely indicates the LOI is non-binding with regards to completing the transaction. In other words, the LOI does not create a legal obligation to purchase the target. However, the Exclusivity and Confidentiality provisions will be legally binding.

This non-binding indication of interest is confidential and may not be disclosed other than to you, the Company, and its advisors on a strictly need-to-know basis. It is not intended, and shall not be deemed, to create any binding obligation on the part of OUR NAME, or any of its affiliates, to engage in any transaction with the Company or to continue its consideration of any such transaction. Subject to the immediately following sentence, none of the parties shall be bound in any way in connection with this letter unless and until the parties execute a definitive agreement, and then shall be bound only in accordance with the terms of such agreement. Notwithstanding anything to the contrary in this letter, the Exclusivity and Confidentiality Agreement, once executed by the parties thereto, shall constitute binding obligations of the parties thereto.

We are very excited about the potential opportunity and hope that you are equally interested in proceeding in a constructive and expeditious dialogue. We look forward to working with you to complete this transaction.

Very truly yours,

[Signature]

Name

Company Name

There may be further sections in the LOI regarding how the target company runs its business during this evaluation period. A buyer will want to make sure that the company operates in an ordinary course and doesn’t, as an example, pay shareholders an extra large dividend, depriving the target company of cash and potentially changing the deal terms.

Note: This letter of intent (LOI) template is only for educational purposes and should not be used for any other purpose.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Drafting a letter of intent (LOI) is an important skill for professionals in investment banking, private equity, and corporate development.

To take your corporate finance career to the next level, you may find these resources helpful: