Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

What you need to know about transaction multiples

Transaction Multiples are a type of financial metrics used to value a company. In an M&A deal, the valuation of a particular company is done by various methods, including discounted cash flow and multiples. Among the different methods, Transaction Multiples play a very different role, as they make the buyer aware of the value of a particular kind of company for investors based on recent trends. It assists in the understanding of multiples and premiums paid in a specific industry.

Calculating transaction multiples takes into consideration several factors, such as the type of premium a company needs to pay to get a controlling stake. This is also one of the reasons why transaction multiples are higher than trading multiples.

Transaction multiples are also known as “Precedent Transaction Analysis.”

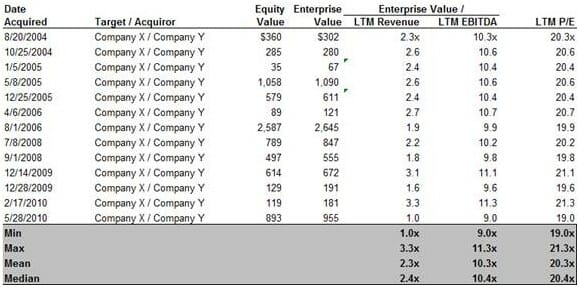

The table below shows a snapshot of transaction multiples for different transactions:

Thank you for reading CFI’s guide to Transaction Multiples. To keep learning and advancing your career, the following resources will be helpful: