Get Certified for

Financial Planning & Wealth Management Professional (FPWMP®)

Learn financial analysis & planning, portfolio management, and risk assessment.

The ratio of losses paid out and premiums earned, expressed as a percentage

The loss ratio, used primarily in the insurance industry, is a ratio of losses paid out to premiums earned, expressed as a percentage.

The formula for the loss ratio is provided below:

Where:

A simpler but less commonly used variation to the formula above is to divide insurance claims paid by total premiums earned, ignoring the loss adjustment expense. The variation is generally used when a quick calculation is required or the loss adjustment expense figure is not readily available.

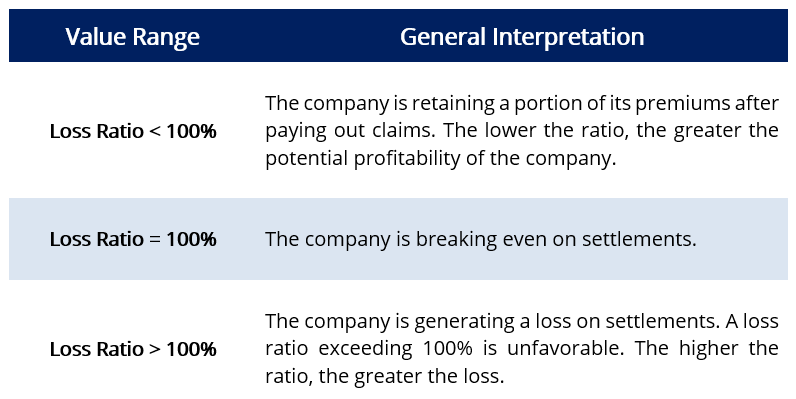

The purpose behind the loss ratio is to provide insurance companies with a high-level overview of their financial performance by comparing the costs paid for claims versus the premiums received. The following shows the value range of the loss ratio and its general interpretation:

Readers should note that the loss ratio is commonly combined with the expense ratio (calculated by dividing underwriting expenses by total premiums earned) to provide a greater sense of profitability. The combination of the two ratios is called the combined ratio.

As such, a loss ratio below 100% does not necessarily indicate a profitable company – other expenses, such as agent’s sales commissions, salaries, overhead expenses, marketing expenses, and other general expenses, which are not reflected in the loss ratio but in the expense ratio, should be considered to assess profitability.

Question 1: An insurance company earned $100 million in premiums from clients in 2020. In the same year, claims paid out totaled $60 million, and an additional $5 million was spent adjusting claims. What is the loss ratio?

Answer: The loss ratio is calculated as ($60,000,000 + $5,000,000) / ($100,000,000) x 100 = 65%. The insurance company used 65% of its premiums to pay for claims.

Question 2: Based on the loss ratio in the previous example, is the insurance company profitable?

Answer: Although the insurance company is retaining a portion of its premiums after paying out claims, it is unclear whether the company is profitable. Additional expenses, such as overhead expenses, salaries, marketing, etc., are not incorporated in the ratio. The loss ratio should be used in conjunction with the expense ratio to determine the company’s profitability.

Each insurance company formulates its own target loss ratio, which depends on the expense ratio. For example, a company with a very low expense ratio can afford a higher target loss ratio. In general, an acceptable loss ratio would be in the range of 40%-60%.

Below are several reasons why a company may incur a high loss ratio:

When the insurance company underestimates its clients’ risk profile, the loss ratio is expected to be higher. For example, in auto insurance, insurance companies commonly look at (1) the driving record of the client, (2) the type of car to be insured, (3) limits and deductibles chosen, (4) age and gender, and (5) purpose of the use of the car to determine an individual’s risk profile and resulting premium.

Underestimation of the above factors would lead to the company offering that individual a lower premium when, in fact, the individual demonstrates a riskier profile.

In the event of a natural disaster, the number of claims tends to increase. For example, natural disasters such as wildfires and hurricanes caused $76 billion in insured losses for Swiss Reinsurance Company Ltd. in 2020 – a 40% increase year-over-year.

The company may employ insurance adjusters who are inefficient in their role, causing unnecessary additional expenses.

Thank you for reading CFI’s guide to Loss Ratio. To keep advancing your career, the additional resources below will be useful: