Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

A dividend is a portion of a company’s profits paid to shareholders, offering a steady income stream and signaling financial health to the market.

A dividend is a portion of a company’s profits that is paid out to its shareholders. Dividends are one of the most common ways companies distribute profits to shareholders. When a company earns a profit and accumulates retained earnings, it can either reinvest that money into the business or return it to shareholders in the form of dividends.

Investors often view dividend-paying stocks as a sign of a stable and mature company, particularly in sectors like utilities, consumer goods, and finance. Dividends also play a key role in investment income strategies, especially for those seeking long-term income from the stock market.

There are two primary types of dividends:

Example:

If you own 50 shares of a company and it declares a $1 dividend, you’ll receive $50 in dividend income, usually deposited automatically into your account.

Dividends can take several forms, depending on a company’s structure and financial policy. Below are common examples of dividends and how they work in real-world scenarios:

A company declares a quarterly dividend of $0.50 per share. If you own 200 shares, you receive $100 in dividend income deposited into your brokerage account. This is the most common type of dividend.

Instead of cash, a company issues a 5% stock dividend, meaning you receive 5 additional shares for every 100 you own. This increases your ownership without requiring a new investment.

A company experiences a one-time surge in profits (e.g., asset sale or windfall gain) and issues a special dividend of $1.50 per share to reward shareholders. This is separate from the regular payout schedule.

Although rare, some companies issue non-cash dividends in the form of physical assets or shares in a subsidiary business. These are typically disclosed with more complex tax implications.

Holders of preferred stock receive fixed dividends before any dividends are paid to common shareholders. For example, a preferred stock may pay $2 annually, regardless of the company’s performance.

These examples highlight how companies structure dividend payments to meet different investor preferences and financial goals.

Dividends in finance are an essential part of many investors’ strategies, especially those who are looking for a steady income stream from their investments. Companies, mutual funds, and exchange-traded funds that pay regular dividends are often seen as stable and profitable, making them attractive to investors who prefer lower-risk opportunities.

Understanding how dividend payments work is essential for anyone interested in investing in or analyzing dividend-paying businesses.

The first step in the dividend payment process begins with the company. When a company makes a profit, its board of directors decides whether to pay out a portion of these profits as dividends to shareholders. This decision is based on factors like the company’s financial health, future growth plans, and overall business strategy.

Once the decision is made, the company announces the dividend amount per share and the schedule for payment. This announcement informs shareholders about the expected dividend they will receive.

There are several key dates to keep in mind when it comes to dividend payments:

Once the payment date arrives, the company distributes the dividend to all eligible shareholders:

Dividend income may be taxable depending on your jurisdiction and the classification as qualified dividends or ordinary income.

For example, if you own 100 shares of a company and they pay a $1 dividend per share, you will receive $100 in dividend income. This payment is often deposited directly into your brokerage account, so there’s no need to take any action on your part. However, dividend income can include a tax liability, such as capital gains tax or income tax, so it’s important to speak to a tax professional about any dividend-paying stocks you own and dividend payments received.

Many investors choose to reinvest their dividend income to buy more shares of the same stock. Reinvesting dividends can be a powerful way to grow your investment over time, as it allows you to benefit from compounding returns. Over the long term, this can significantly increase your stock holdings and potential future dividend income. Many companies offer dividend reinvestment plans (DRIP) to help shareholders reinvest dividends.

Companies pay dividends for several strategic and financial reasons that align with shareholder expectations and market positioning:

Mature businesses, especially those in low-growth industries, tend to prioritize dividends as a way to distribute excess cash. Rather than reinvesting all profits into expansion, they return a portion to shareholders, often as part of a larger dividend investing strategy. This approach also reduces idle capital and reflects management’s confidence in long-term profitability.

The amount of a dividend is typically determined by the company’s leadership, usually the board of directors, after reviewing the company’s financial performance. The primary goal is to strike a balance between rewarding shareholders and retaining enough capital to support future growth and operations.

To set a dividend amount, the board assesses the company’s net income, or what’s left after all expenses have been paid. Then, the company decides how much to allocate toward dividends versus how much to reinvest in the business. This allocation reflects the company’s confidence in its financial health and future prospects.

Several key factors influence how much a company’s earnings it decides to pay in dividends, including:

Dividend yield is a key metric that investors use to assess a dividend’s value relative to its stock price. It is calculated by dividing the annual dividend per share by the current stock price and is expressed as a percentage.

For example, if a company pays an annual dividend of $2 per share and its stock is priced at $40, the dividend yield would be 5% ($2 ÷ $40 = 0.05, or 5%). A higher yield can make an investment in a company’s stock more attractive to income-focused investors, as it indicates a higher return on their investment through dividends.

However, while a high dividend yield may seem appealing, it’s important to consider the sustainability of that yield. If the yield is high because the share price has dropped significantly, it could signal underlying issues within the company. Therefore, yield should be evaluated alongside other financial metrics to get a complete picture of the company’s health and prospects.

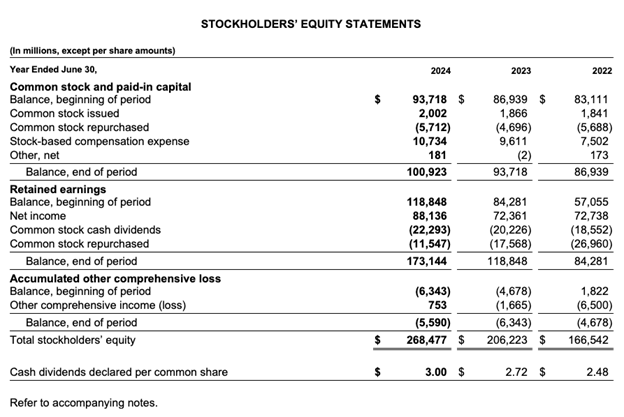

The example below is Microsoft’s 2024 shareholders’ equity statement. The last item in this statement shows that Microsoft declared a dividend per common share of $3.00 in 2024, $2.72 in 2023, and $2.48 in 2022.

This figure can be compared to Earnings per Share (EPS) from continuing operations and Net Earnings for the same time period.

When a company pays a dividend, it is not considered an expense on the income statement since it is a payment made to the company’s shareholders. This differentiates it from a payment for a service to a third-party vendor, which would be considered a company expense.

Dividends:

This is important for anyone building financial models or analyzing investments.

Corporations have several types of distributions they can make to the shareholders. The two most common distribution types are dividends and share buybacks. A share buyback is when a company uses cash on the balance sheet to repurchase shares in the open market.

Both dividends and share buybacks return capital to shareholders, but in different ways:

Buybacks may appeal to companies aiming to increase EPS or boost stock price performance.

Share buybacks are a way to both return cash to shareholders and reduce the number of shares outstanding, which can help boost a company’s earnings per share (EPS). When the number of shares decreases, the denominator in EPS (net earnings/shares outstanding) decreases; thus, EPS increases.

Corporations are frequently evaluated on their ability to move share price and grow EPS, so they may be incentivized to use the buyback strategy.

Paying dividends has no impact on the enterprise value of the business. However, it reduces the equity value of the business by the value of the dividend paid.

In financial modeling, it’s important to have a solid understanding of how a dividend payment impacts a company’s balance sheet, income statement, and cash flow statement. In CFI’s financial modeling courses, you’ll learn how to link the financial statements together so that any dividends paid flow through all the appropriate accounts.

A well-laid-out financial model will typically have an assumptions section where any return of capital decisions are contained. For example, if a company is going to pay a dividend in 2026, then there will be an assumption about what the dollar value will be, which will flow out of retained earnings and through the cash flow statement (financing activities), which will also reduce the company’s cash balance.

Dividend vs Share Buyback/Repurchase

Analysis of Financial Statements

See all Financial Modeling resources

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Yes, in most cases. Qualified dividends are taxed at the capital gains rate, while others are taxed as ordinary income. Tax treatment depends on your location and holding period.

Not exactly. While dividends provide income, they’re paid from the company’s profits, so the share price often adjusts down by the amount of the dividend after the payout.

Most companies pay dividends quarterly, but some pay monthly or annually. The frequency depends on the company’s dividend policy and cash flow.

Dividend yield tells you how much cash return an investor receives from owning a stock relative to the stock’s current price. It’s calculated by taking a company’s annual dividend per share and dividing it by the current share price. For example, a dividend of $2 per share that trades at $40 has a dividend yield of 5%.