Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Each common share’s profit allocation out of the company’s total profit

Earnings per share (EPS) is a key metric used to determine the common shareholder’s portion of the company’s profit. EPS measures each common share’s profit allocation in relation to the company’s total profit. IFRS uses the term “ordinary shares” to refer to common shares.

The EPS figure is important because it is used by investors and analysts to assess company performance, predict future earnings, and estimate the value of the company’s shares. The higher the EPS, the more profitable the company is considered to be and the more profits are available for distribution to its shareholders.

Capital structures that do not include potentially dilutive securities are called simple capital structures. On the other hand, complex capital structures include such securities.

Dilutive securities refer to any financial instrument that can be converted or can increase the number of common shares outstanding for the company. Dilutive securities can be convertible bonds, convertible preferred shares, or stock options or warrants.

There are two different types of earnings per share: basic and diluted. Reporting basic EPS is required because it increases the comparability of earnings between different companies. Diluted EPS is required to reduce moral hazard issues.

Without diluted EPS, it would be easier for the management to mislead shareholders regarding the profitability of the company. It is done by issuing convertible securities such as bonds, preferred shares, and stock options that do not require issuing common shares immediately but can lead to issuance in the future.

Basic EPS Diluted EPS

Shows how much of the company’s earnings are attributable to each common share Amount of the company’s earnings attributable to each common shareholder in a hypothetical scenario in which all dilutive securities are converted to common shares

EPS = (Net income available to shareholders) / (Weighted average number of shares outstanding) Amount of the company’s earnings attributable to each common shareholder in a hypothetical scenario in which all dilutive securities are converted to common shares

Basic EPS is always larger than diluted EPS Diluted EPS is always smaller than basic EPS

Net income available to shareholders for EPS purposes refers to net income less dividends on preferred shares. Dividends payable to preferred shareholders are not available to common shareholders and must be deducted to calculate EPS.

There are two kinds of preferred shares that we need to know about: cumulative and non-cumulative. For cumulative preferred shares, the preferred shareholder’s entitlement must always be deducted regardless of whether they are declared or paid.

Only the current period’s dividends should be considered, not any dividend in arrears. For non-cumulative preferred shares, the dividends should only be deducted if the dividend has been declared.

To determine the total number of common shares, we calculate the weighted average number of ordinary shares outstanding. A weighted average number is used instead of a year-end number because the number of common shares frequently changes throughout the year.

Consider the following example:

Assume that on January 1, 2017, XYZ Company reported the following:

Preferred shares: 1,000,000 authorized, 400,000 issued and outstanding, $4 per share per year dividend, cumulative, convertible at the rate of 1 preferred to 5 common shares.

Common shares: 5,000,000 authorized, 800,000 issued and outstanding, no par value, and no fixed dividend.

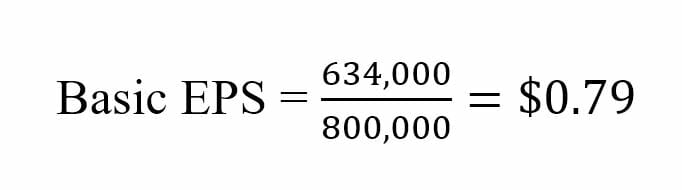

Calculate Basic EPS if net income was $2,234,000.

| Net income | $2,234,000 |

| Less: Cumulative preferred dividends | ($1,600,000) |

| Net income available to common shareholders | $634,000 |

In our example, there are no instances of common share issuance or repurchase. Therefore, the weighted average is equal to the number of shares outstanding: 800,000

Enter your name and email in the form below and download our free Earnings Per Share template now!

When calculating diluted EPS, we must always consider and identify all potential ordinary shares.

A potential ordinary share describes any financial instrument that can lead to one or more common shares in the future. Thus, a potentially dilutive share is one that decreases EPS because the denominator value for the number of shares increases. As mentioned before, potential ordinary shares include:

When calculating diluted EPS, we always use the if-converted method. The if-converted method assumes that the security is converted into common shares at the beginning of the period unless noted otherwise and that the company did not pay interest or preferred share dividends during the year because it is assumed to be converted at the beginning of the year.

Remember that interest on bonds payable is a tax-deductible expense while dividends on preferred shares are not. Finally, for stock options and warrants, we must only consider options that are “in-the-money.” They refer to options in which the exercise price is lower than the average market price of the shares.

Watch the short video below to quickly understand the main concepts covered here, including what earnings per share is, the formula for EPS, and an example of EPS calculation.

Investors purchase the stocks of a company to earn dividends and sell the stocks in the future at higher prices. The earning capability of a company determines the dividend payments and the value of its stocks in the market. Hence, the earnings per share (EPS) figure is very important for existing and prospective common shareholders.

However, a company’s real earning capability cannot be assessed by the EPS figure for one accounting period. Investors should compute the company’s EPS for several years and compare them with the EPS figures of other similar companies to select the most appropriate investment option.

A company with a constant increase in its EPS figure is usually regarded to be a reliable option for investment. Furthermore, investors should use the EPS figure in conjunction with other ratios to estimate the future stock value of a company.

Many companies today issue stock options and warrants to their employees as part of their benefits package. Would such a benefit be appealing to you or are they simply a marketing tactic? Although the benefits can prove to be useful, they also come with limitations. Let us take a look at the advantages and disadvantages of stock option benefits.

| Addresses the issue of moral hazard – Employees are motivated to work harder because the value of their compensation can increase through better performance. | Employees may have low tolerance to risks and therefore, they may not like the risk inherent in stock options. |

| Typically, the options have a vesting period wherein employees can only exercise them at a later date, which helps retain employees. | If employees do not understand the value of the options, they will not consider it a benefit. |

| If the options are exercised, employees become shareholders, which ensures that they will act in the best interests of the company. | Employees have limited abilities to affect the stock price and therefore, stock options might not be motivating enough for them to work hard. |

Thank you for reading CFI’s guide to Earnings Per Share (EPS). To increase your knowledge and advance your career, see the following free CFI resources: