Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

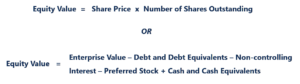

Total value of the company available to equity investors

Equity value, commonly referred to as the market value of equity or market capitalization, can be defined as the total value of the company that is attributable to equity investors. It is calculated by multiplying a company’s share price by its number of shares outstanding.

Alternatively, it can be derived by starting with the company’s Enterprise Value, as shown below.

To calculate equity value from enterprise value, subtract debt and debt equivalents, non-controlling interest, and preferred stock, and add cash and cash equivalents. Equity value is concerned with what is available to equity shareholders.

Debt and debt equivalents, non-controlling interest, and preferred stock are subtracted as these items represent the share of other shareholders. Cash and cash equivalents are added, as any cash left after paying off other shareholders is available to equity shareholders.

The equity value of a company is not the same as its book value. It is calculated by multiplying a company’s share price by its number of shares outstanding, whereas book value or shareholders’ equity is simply the difference between a company’s assets and liabilities.

For healthy companies, equity value far exceeds book value as the market value of the company’s shares appreciates over the years. It is always greater than or equal to zero, as both the share price and the number of shares outstanding can never be negative. Book value can be positive, negative, or zero.

Basic equity value is simply calculated by multiplying a company’s share price by the number of basic shares outstanding. A company’s basic shares outstanding can be found on the first page of its 10K report. The calculation of basic shares outstanding does not include the effect of dilution that may occur due to dilutive securities such as stock options, restricted and performance stock units, preferred stock, warrants, and convertible debt.

A section on these securities can also be found in the 10K report. The dilutive effect of these securities can be calculated using the treasury stock method. To calculate the diluted shares outstanding, add the additional number of shares created due to the dilutive effect of securities on the basic securities outstanding.

Since all in the money securities are paid off by the buyer during an acquisition, from a valuation perspective, diluted shares outstanding should be used when using equity value or calculating enterprise value, as it more accurately determines the cost of acquiring a firm. Furthermore, once the buyer pays off these securities, they convert into additional shares for the buyer, further raising the acquisition cost of the company.

It is very important to understand the difference between equity value and enterprise value, as these are two very important concepts that nearly always come up in finance interviews.

Simply put, enterprise value is the value of a company’s core business operations that is available to all shareholders (debt, equity, preferred, etc.), whereas equity value is the total value of a company that is available to only equity investors.

To calculate enterprise value from equity value, subtract cash and cash equivalents and add debt, preferred stock, and minority interest. Cash and cash equivalents are not invested in the business and do not represent the core assets of a business.

In most cases, both short-term and long-term investments are also subtracted; however, this requires an analyst’s judgment and depends on how liquid the securities are. Debt, preferred stock, and minority interest are added as these items represent the amount due to other investor groups. Since enterprise value is available to all shareholders, these items need to be added back.

Given the enterprise value, one can work backward to calculate equity value.

Enterprise value is more commonly used in valuation techniques as it makes companies more comparable by removing their capital structure from the equation.

In investment banking, for example, it’s much more common to value the entire business (enterprise value) when advising a client on an M&A process.

In equity research, by contrast, it’s more common to focus on the equity value since research analysts are advising investors on buying individual shares, not the entire business.

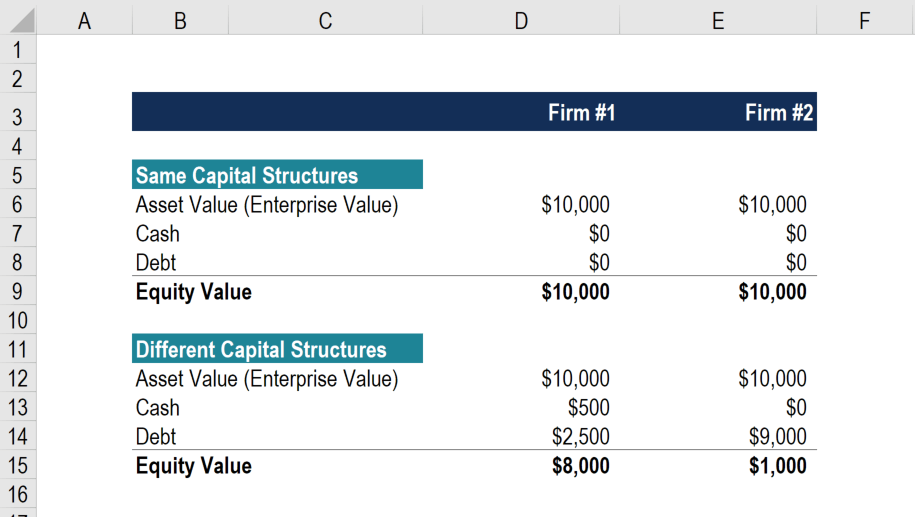

In the illustration below, you will see an example of enterprise value vs equity value. We take two companies that have the same asset value and show what happens to their equity value as we change their capital structures.

As shown above, if two companies have the same enterprise value (asset value, net of cash), they do not necessarily have the same equity value. Firm #2 financed its assets mostly with debt and, therefore, has a much smaller equity value.

Both equity value and enterprise value are used to value companies, with the exception of a few industries, such as banking and insurance, where only equity value is used. An important thing to understand is when to use equity value and when to use enterprise value. It depends on the metric that is being used to value a company.

If the metric includes the net change in debt, interest income, and expense, then equity value is used; if it does not include the net change in debt, interest income, and expense, then enterprise value is used. The reason enterprise value is used before any interest or debt has been deducted is that the cash flow is available to both debt and equity shareholders.

Learn more about Comparable Company Analysis and different types of valuation multiples.

When calculating equity value, levered free cash flows (cash flow available to equity shareholders) are discounted by the cost of equity, the reason being, the calculation is only concerned with what is left for equity investors.

Similarly, when calculating enterprise value, unlevered free cash flows (cash flow available to all shareholders) are discounted by Weighted Average Cost of Capital (WACC), as now the calculation includes what is available to all investors.

Click the button below to download our free Enterprise Value vs Equity Value Calculator template!

The most common use of equity value is to calculate the Price Earnings Ratio. While this multiple is the most well-known to the general public, it is not the favorite of bankers. The reason for this is that the P/E ratio is not capital structure neutral and is affected by non-cash and non-recurring charges, and different tax rates.

However, there are certain industries where the P/E ratio and equity value are more meaningful than enterprise value and its multiples. Such industries include banks, financial institutions, and insurance firms.

The reason the P/E ratio is more meaningful than enterprise value multiples is that banks and financial institutions use debt differently than other companies, and interest is a major component of a bank’s revenue.

Furthermore, it is extremely hard to differentiate between the operating and financing activities of such institutions. These institutions are valued using metrics such as Price/Earnings and Price/Book value.

For intrinsic valuation, dividend discount models are used instead of a traditional DCF model (a form of financial modeling). A dividend discount model is based on projecting a company’s dividends per share using projected EPS. It involves discounting these dividends using the cost of equity to get the NPV of future dividends.

The next step involves calculating the terminal value based on the P/BV multiple in the final year and discounting it back to its NPV. Finally, sum the present values of dividends and the present value of the terminal value to calculate the company’s net present value per share.

Sometimes, a future share price valuation is also used, which is again based on projecting a company’s share price based on P/E multiples of comparable companies and then discounting it back to present value.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading this guide to calculating the market value of equity for a firm. To keep learning and advancing your career, CFI has created a wide range of resources to help you become a world-class financial analyst: