Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Used in financial modeling to value a firm

Unlevered Free Cash Flow (also known as Free Cash Flow to the Firm or FCFF for short) is a theoretical cash flow figure for a business. It is the cash flow available to all equity holders and debtholders after all operating expenses, capital expenditures, and investments in working capital have been made.

Unlevered Free Cash Flow is used in financial modeling to determine the enterprise value of a firm. It is technically the cash flow that equity holders and debt holders would have access to from business operations.

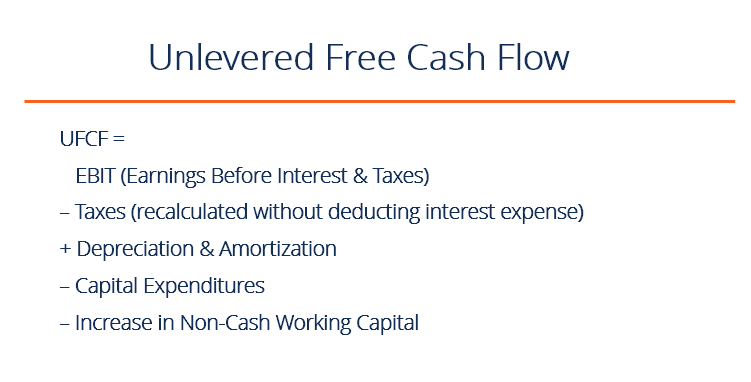

The formula is:

Unlevered free cash flow is used to remove the impact of capital structure on a firm’s value and to make companies more comparable. Its principal application is in valuation, where a discounted cash flow (DCF) model is built to determine the net present value (NPV) of a business. By using unlevered cash flow, the enterprise value is determined, which can easily be compared to the enterprise value of another business.

There are two main reasons capital structure is ignored when performing a valuation:

Let’s explore each of these ideas in more detail below.

Comparability. Since some companies have a high interest expense, while others have little to no interest expense, the levered cash flow of two firms can be skewed by the impact of interest. By removing the interest expense and recalculating taxes, it’s much easier to make an apples to apples comparison.

Discretionary. This point is somewhat theoretical, as firms may be limited in how much flexibility they have, but in theory, the owners or managers of the business can put whatever capital structure they want on the business.

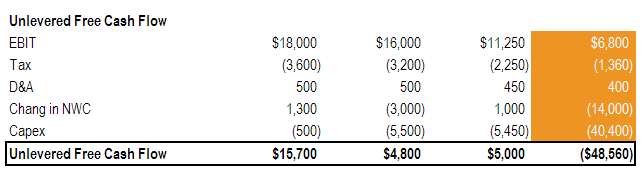

Here is a step-by-step example of how to calculate unlevered free cash flow (free cash flow to the firm):

This is the most common cash flow metric used for any type of financial modeling valuation.

As you can see in the example above and the section highlighted in gold, EBIT of $6,800, less taxes of $1,360 (without deducting interest), plus depreciation and amortization of $400, less an increase in non-cash working capital of $14,000, less capital expenditures of $40,400, results in unlevered free cash flow of -$48,560.

Enter your name and email in the form below and download the free Unlevered Free Cash Flow template now!

When using unlevered free cash flow to determine the Enterprise Value (EV) of the business, a few simple steps can be taken to arrive at the equity value of the firm.

To arrive at equity value, take the following steps:

To learn more, see our guide on equity value vs enterprise value.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to Unlevered Free Cash Flow. To keep learning and advancing your career, the following CFI resources will be helpful: