Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Earnings Before Interest and Taxes

EBIT stands for Earnings Before Interest and Taxes and is one of the last subtotals in the income statement before net income. EBIT is also sometimes referred to as operating income and is called this because it’s found by deducting all operating expenses (production and non-production costs) from sales revenue.

Dividing EBIT by sales revenue shows you the operating margin, expressed as a percentage (e.g., 15% operating margin). The margin can be compared to the firm’s past operating margins, the firm’s current net profit margin and gross margin, or to the margins of other, similar firms operating in the same industry.

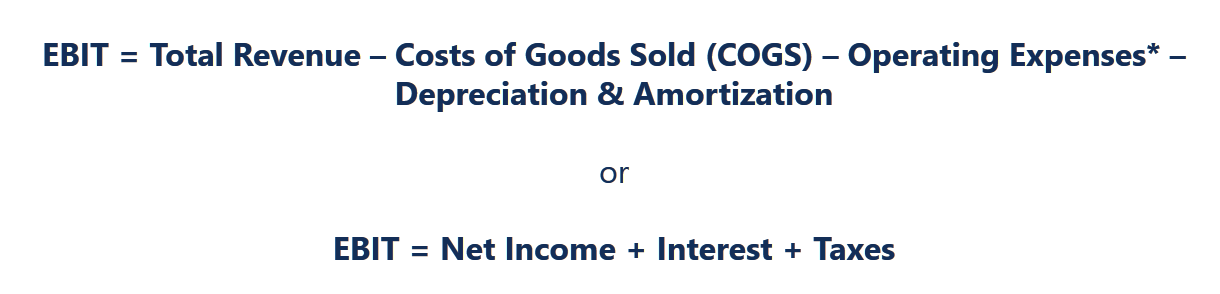

Earnings Before Interest and Taxes can be calculated in two ways. The first is by starting with EBITDA and then deducting depreciation and amortization. Alternatively, if a company does not use the EBITDA metric, operating income can be found by subtracting SG&A (excluding interest but including depreciation) from gross profit.

Here are the two EBIT formulas:

EBIT = Net Income + Interest + Taxes

EBIT = EBITDA – Depreciation and Amortization Expense

Starting with net income and adding back interest and taxes is the most straightforward, as these items will always be displayed on the income statement. Depreciation and amortization may only be shown on the cash flow statement for some businesses.

Earnings Before Interest and Taxes can be used as a proxy for free cash flow in some industries – it works well as long as it’s applied to stable, mature companies with relatively consistent capital expenditures. The EBIT metric is closely tied to free cash flow (FCF).

FCF can be found through the following formula:

FCF = EBIT (1 – T) + D&A + Δ NWC – CapEx

Where:

FCF = Free Cash Flow

T = Average Tax Rate

Δ NWC = Change in Non-Cash Working Capital

CapEx = Capital Expenditures

To learn more, see our guides to Cash Flow and Free Cash Flow.

The EV/EBITDA multiple is often used in comparable company analysis to value a business. By taking the company’s Enterprise Value (EV) and dividing it by the company’s annual operating income, we can determine how much investors are willing to pay for each unit of EBIT.

Example:

A company reported a market capitalization of $50M, a debt of $20M, and cash of $10M. The company also posted a 2017 net income of $4M, taxes of $1M, and interest expense of $1M. What is its 2017 EV/EBIT multiple?

Solution:

EV = $50M + $20M – $10M = $60M

EBIT = $4M + $1M + $1M = $6M

2017 EV/EBIT = 10.0x

Investors use Earnings Before Interest and Taxes for two reasons: (1) it’s easy to calculate, and (2) it makes companies easily comparable.

#1 – It’s very easy to calculate using the income statement, as net income, interest, and taxes are always broken out.

#2 – It normalizes earnings for the company’s capital structure (by adding back interest expense) and the tax regime that it falls under. The logic here is that an owner of the business could change its capital structure (hence normalizing for that) and move its head office to a location under a different tax regime. Whether or not these are realistic assumptions is a separate issue, but, in theory, they are both possible.

We hope this has been a helpful guide to Earnings Before Interest and Taxes, including how to calculate it, what it’s used for, and why it matters to investors. To continue building your corporate finance knowledge base, we highly recommend these related CFI articles and guides: