Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

A division within financial services firms that is a hybrid between Commercial and Investment Banking

Corporate banking is a very important division within many large commercial and bulge bracket banks; this team serves as a critical link between the commercial banking group and the capital markets/investment banking teams.

Corporate banking teams provide financial services like cash management, payment processing, credit products, and hedging strategies to large corporations. Most of these corporations are publicly traded.

The term “corporate banking” is often used erroneously by non-finance people when talking about the provisioning of banking services to corporations (broadly); however, there is much more nuance when it comes to banking for businesses.

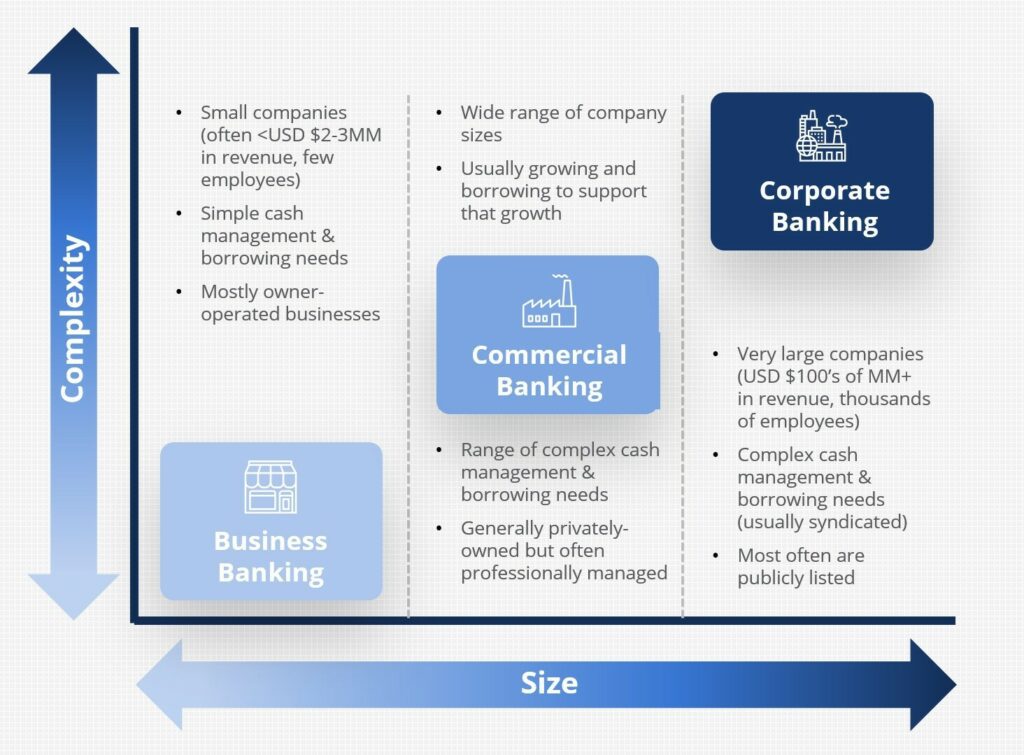

As illustrated in the graphic above, there are generally three groups at a bank that provide financial services to business clients (as opposed to individual, “retail” clients). These are the business banking team (often called small business), commercial banking, and the corporate banking team.

The easiest way to plot a prospective client on this chart is by its size and its level of complexity. “Small businesses” are typically characterized by much lower revenues and very simple operations, whereas corporate banking prospects are generally extremely large and very complex businesses (which require complex banking and credit solutions).

In order to deliver complex banking products and credit solutions, a corporate banker must have extensive industry knowledge as well as experience with their firm’s systems and processes.

One of the most common complex credit solutions provided for corporate banking clients is syndicated lending.

Corporate bankers from different financial institutions join together to offer credit and share in the risk of financing a corporate borrower using a multilateral credit arrangement called a syndicated loan.

Corporate banking clients often borrow dollar amounts that are extraordinarily high, given that these are typically large, publicly traded companies. Some of this credit is issued through the corporate bond market, but some is debt (like revolvers, CAPEX loans, and commercial real estate lending) extended directly by financial institutions or other private lenders (e.g. private equity, pension plans, etc).

For example, an institution’s business or commercial banking division may limit credit to a single name or group of a specific risk to $10MM via a bilateral lending agreement. Beyond that, the same bank’s corporate banking division may get involved in structuring multilateral lending via a syndicate once its corporate hold limit is exceeded.

Concentration risk from any single name or group on the balance sheet of the lending institution guides the hold limit amount and influences a firm’s participation in a syndicate.

As noted earlier, the principal difference between business/commercial banking and corporate banking is the size and complexity of the borrowing client’s operations, as well as the nature of the financial services and products it requires. Other key differences include:

External recourse (guarantees) for public companies that are widely held or for large private companies tend to be from other related corporations rather than individuals. The construct of this collateral is part of “ring-fencing” that determines the overall value of the borrowing entity.

CFI offers the CBCA™ certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following resources will be helpful: