Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

How loans are customized based on the risk of the borrower and the nature of the credit request

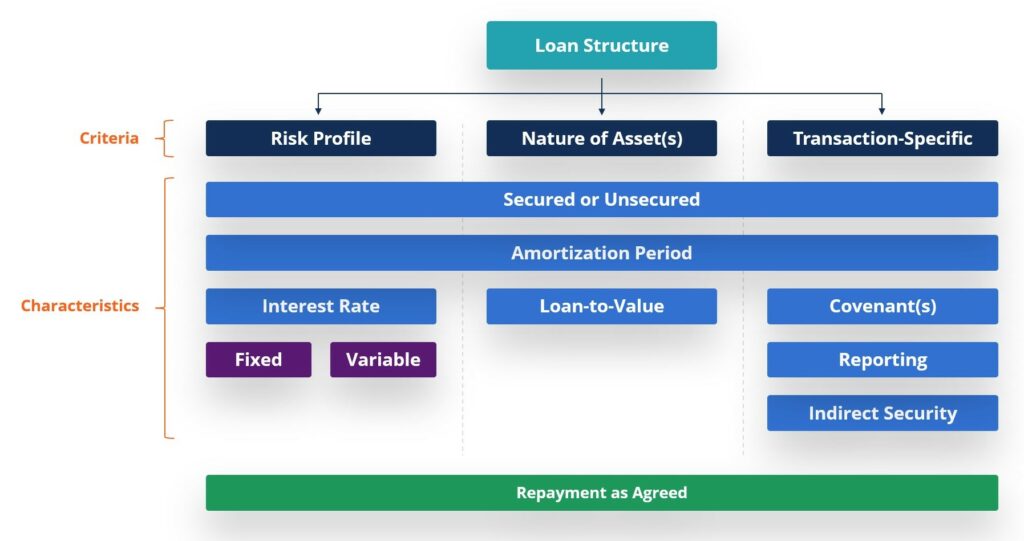

Loan structure refers to the different characteristics that a lender can choose from when extending credit to a borrower. Loan structure is also often referred to as credit structure.

Lenders always want to offer their borrowers credit that is appropriate based upon the nature of the credit request, as well as the perceived risk of the borrower.

As a result, every loan has a variety of characteristics that make it unique from other loans. Examples include, but are not limited to:

Anyone who’s ever borrowed from a bank knows that credit always comes with some guidelines and parameters.

For example, if a borrower wanted to purchase a home, it would be strange for the lender to offer a 5-year amortization. It would also be strange if they offered a 50-year amortization.

A loan to purchase a home is what’s called a mortgage loan; market terms on a mortgage loan are much more like 25 or 30 years (not 5 or 50). Conversely, car loans are generally not 25 or 30 years, they’re much more like 5 or 8 years.

Why is this? Because of loan structure!

Loan structure is informed, at least in part, by any underlying assets that are being financed – as in our mortgage loan example above. But there are other factors and criteria, too. These include:

Lenders have complex risk rating models that help them understand the borrower’s likelihood of triggering an event of default. The higher the likelihood of default, the greater the credit risk.

Higher risk scores generally translate to higher interest rates and loan pricing, which compensate the lender for taking on this greater level of risk. Higher risk scores also tend to translate to more restrictive loan structures (such as shorter amortization periods, higher levels of collateral security, or more frequent and more robust financial reporting).

Credit is generally extended to support the financing (or the refinancing) of an asset. The quality of that asset as collateral will also help to inform loan structure, including loan-to-value (LTV).

As a general rule, the more “desirable” an asset, the more flexible the loan structure is likely to be. Higher quality collateral is generally characterized by how active the secondary market is, how ascertainable its price is, and how stable the asset’s value is likely to remain.

For example, real estate is generally considered more desirable as collateral than intellectual property. As a result, it will tend to have higher LTVs, lower interest rates, and longer amortizations.

This is particularly true of corporate borrowers – think about a piece of manufacturing equipment. If equipment is being purchased and it’s intended to produce cash flow for 10 years, it’s not unreasonable to consider a 10-year repayment period.

The upper limit on amortization may be governed by the condition of the asset, but, intuitively, it would be odd to force a company to pay in full upfront for an asset that will generate cash flow for many years into the future.

This, too, is mostly true of corporate borrowers. Consider a management team that strips a lot of cash out of the company by way of dividends. A lender may wish to put a covenant in place that would restrict dividends to ensure that a sufficient cash buffer is retained in the corporation to support liquidity (and timely loan payments).

Another example is if a borrower was taking on operating credit to finance inventory. A prudent lender may structure the credit such that the borrower must provide periodic inventory listings so that the lender can keep a pulse on the quality and the quantity of inventory on the company’s balance sheet.

While this is not an exhaustive list, important considerations around loan structure include the following:

World-class credit professionals understand how important it is to structure credit effectively, within the context of both managing risk and the competitive landscape in which they operate.

Many financial institutions and non-bank, private lenders have credit policies in place to help provide guardrails for their relationship management teams to work within when negotiating loan terms with prospective borrowers.

Loan structure is a way to both mitigate risk and also to differentiate oneself in the market – assuming that a lender is willing to be creative in how they structure credit for their borrowers.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to Loan Structure. To keep learning and developing your knowledge base, please explore the additional relevant resources below: