Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

A type of loan where the lender can demand repayment from the borrower at any time

A call loan is a type of loan where the lender can demand repayment from the borrower at any time. It is different from other loans because it is repayable on demand instead of being repaid based on a fixed schedule.

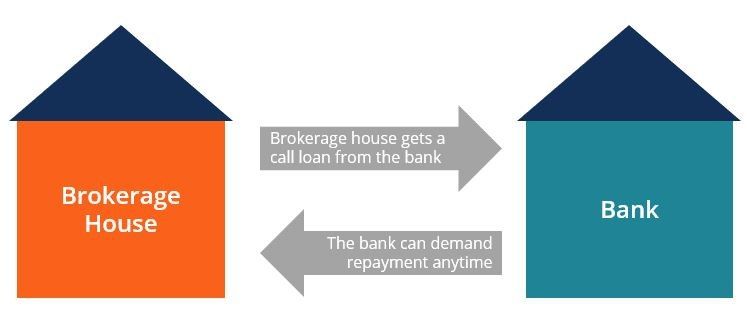

Call loans are usually offered by banks to brokerage houses, which use the loans as short-term financing for their clients’ margin accounts. The bank that provides the loan are able to demand repayment from the brokerage houses at any time. Therefore, call loans are also known as broker loans or broker overnight loans.

The interest rate on a call loan is referred to as the call loan rate or the broker’s call. It is what the bank would charge the brokerage house for the loan. It is accrued and calculated on a daily basis.

Besides offering loans to brokerage houses, another example is used in margin trading. Individuals who are involved with margin trading would open a margin account with a stockbroker. Using the margin account, individuals are able to borrow money from the broker in order to purchase stocks.

The money is lent to the borrowers as a call loan, so the broker will be able to demand repayment of the loan anytime, specifically when the stock price declines substantially in order to ensure that the broker can be able to acquire all its money back.

The risk in margin trading is that the broker is allowed to sell some of the borrowers’ stocks to repay the loan if the borrower is unable to repay on demand. As a result, the borrower faces risks when the stock price drops significantly because the losses are magnified. Not only does the borrower lose from the decline in value of the stock, but the borrower also must sell it to create funds that are needed to repay the loan to the broker.

Besides issuing loans to other brokerage houses, banks also issue call loans to other banks as well. A bank may want to borrow a sum of money from another bank in order to cover short-term financial obligations and temporarily increase its liquidity.

Using call loans is a risky method of financing for brokerage houses and investors who are involved with margin trading. Interest can be accrued quickly every day and loans can be demanded by the lender at any time.

Sometimes, brokerage houses that get call loans from banks may use the proceeds to purchase securities. The securities are used as collateral for the loan if the brokerage house becomes insolvent or cannot repay back the loan upon the banks’ request.

When a lender wants to demand repayment from the borrower, such as a bank demanding payment from a brokerage house, the borrower will be given a certain period of time to repay it back to the lender. During this timeframe, the brokerage house will need to collect and organize the money for repayment.

Although the lender can request repayment at any time, the loan can also be canceled at any time as well. This is because the loan can be repaid by the borrower with no penalty for prepayment.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI offers the Certified Banking & Credit Analyst (CBCA)® certification program for those looking to take their careers to the next level. To keep learning and advance your career, the following resources will be helpful: