Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

When one party receives resources from another party without immediate payment

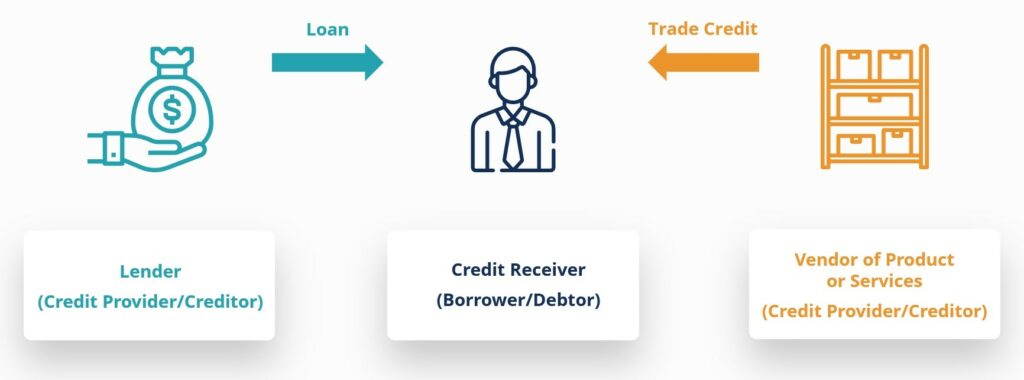

Credit is created when one party (a creditor) provides resources to another party (a debtor) where no immediate payment is made; rather, the resources are provided with a promise of future payment.

The resources provided by the creditor may be financial resources, like actual cash, a credit card limit, or a mortgage for a property purchase. This is typically called a loan and is often extended by a bank or another financial institution.

Alternatively, the resources may be services rendered or physical products. This is what’s known as trade credit, because it facilitates trade between two parties. Consider a plumber who completes work at a job site and then issues an invoice to the general contractor; or a manufacturing business that sells widgets to a wholesaler on open credit with 30-day terms.

Credit is extended based on a promise of future payment (or repayment); this promise is best documented using a legal contract.

In the event of a loan or other type of financial resource, a formal agreement is typically drafted between the counterparties. This agreement may be called a variety of things, including a loan contract, a promissory note, or a credit agreement.

It should outline the terms of the credit, including the interest rate, repayment schedule, covenants, what constitutes an event of default, if collateral is being pledged, and any other characteristics that are relevant to the two counterparties. In all instances, the agreement is legally binding.

When it comes to trade credit, the transaction is typically consummated with a Purchase Order (PO), where the buyer legally agrees to purchase the good(s) or service(s) from the seller. Once the product is delivered or the service is rendered, the purchase order is considered fulfilled and the seller then issues a payment invoice to the buyer. Like a loan agreement, the invoice includes payment terms (like due date, payment instructions, late payment penalties, etc.)

Credit risk is the risk that a creditor will advance resources to a debtor (either financial resources, physical goods, etc.), but that payment will not be received in return.

Before a creditor offers their borrower a loan (or credit terms on a transaction), they must get comfortable with the borrower and the level of credit risk they present.

The two main categories of effective credit risk management are:

Credit professionals use a variety of risk rating and loan pricing models to understand a prospective borrower’s likelihood of triggering an event of default (and to price the risk accordingly).

For personal borrowings like car loans and home mortgages, it’s a fairly formulaic process; a lender may use a few financial ratios, but their models are heavily reliant on the borrower’s credit history (like their FICO score).

For corporate borrowers, risk models tend to be much more advanced since there is a lot more information to unpack in order to understand the financial health of a business and its operations.

A common framework used to assess the creditworthiness of a borrower (and to understand the strength of a borrowing request more broadly) is the 5 Cs of Credit. These are:

An event of default is triggered when one of the terms in a credit agreement is violated by a borrower. Examples include late reporting, breaches of one of the many representations and warranties outlined in the credit agreement, the borrower being offside with a covenant, or a missed payment.

A missed payment is what’s called a delinquent payment. Many people outside of the finance, accounting, and legal community use the term default in reference to a missed or late payment of interest or principal.

A delinquent payment is one example of an event of financial default, but the term “default” does not itself mean “missed payment.” The other category of default is technical defaults; these are non-financial in nature.

When an event of default occurs, a creditor may accelerate repayment of the principal outstanding (sometimes referred to as “calling the loan”). If the principal cannot be refinanced or repaid, the lender may take what’s called enforcement action against any collateral security in order to recover some of the outstanding principal.

Many public companies want to borrow money, too. These large firms may not be able to borrow directly from a financial institution as it might not make sense for the lender to take on the balance sheet risk associated with such a large borrowing amount.

These public companies may instead issue bonds, which are fixed income securities. Individual investors and asset managers can then purchase these bonds in the credit market, in turn becoming creditors to the public issuer.

The creditworthiness of these public issuers must also be monitored and updated based on improvement (or deterioration) in their credit quality. Credit analysts at the various third-party credit rating agencies (Standard & Poor’s, Fitch, Moody’s, etc.) are responsible for objectively assessing the issuers and assigning a credit rating to their fixed income securities accordingly.

Financial institutions may also “package” and sell individual loans that were previously held on their balance sheets (student loans, mortgages, credit card debt, etc.) – a process known as securitization. These securitized products also trade in the credit market and are also rated by credit analysts at various rating agencies.

CFI offers the CBCA™ certification program for those looking to take their careers in commercial lending to the next level. To keep learning and advancing your career, the following resources will be helpful: