Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

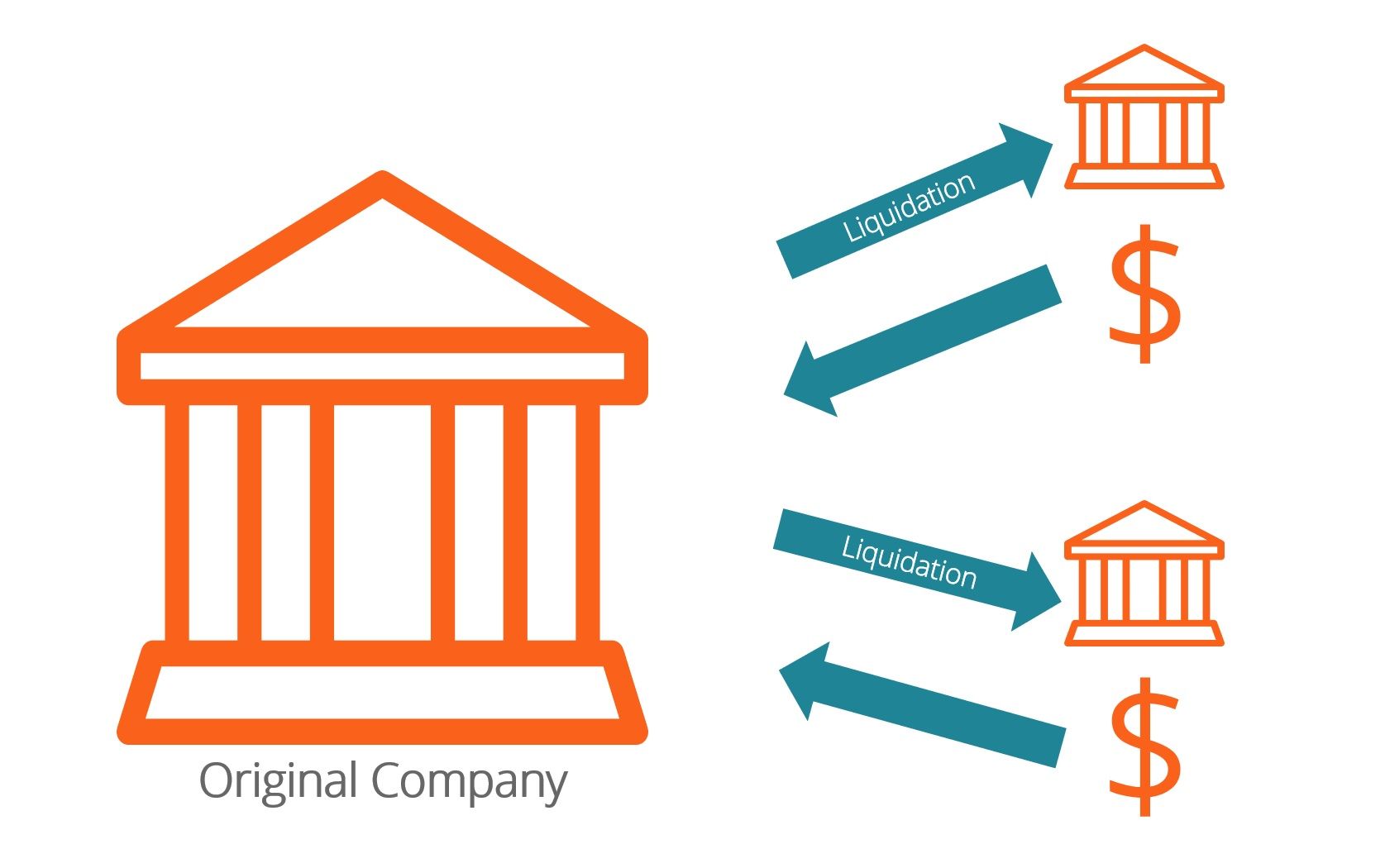

The process by which a business sells off its net assets and ceases operation thereafter

Net asset liquidation or net asset dissolution is the process by which a business sells off its assets and ceases operations thereafter. Net assets are the excess value of a firm’s assets over its liabilities. However, the revenue generated by the sale of the net assets in the market might be different from their recorded book value.

A business usually sells off its assets because it can no longer afford to pay its debts. This is different from a voluntary divestment strategy, which is done to improve operating/financial efficiency.

Here are the different types of liquidating assets:

Complete liquidation is the process by which a business sells off all its net assets and ceases operation. After complete liquidation, the business ceases to exist and is no longer a valid entity. Complete liquidation might be complete voluntary liquidation or complete creditor induced liquidation.

Partial liquidation is the process by which a business sells off part of its assets and reduces the scope of its operation. After partial liquidation, the business continues to exist as a valid entity, albeit with a smaller scale of operation. Partial liquidation might be partial voluntary liquidation or partial creditor induced liquidation.

Voluntary liquidation occurs when a business ceases operation of its own volition. The decision for voluntary liquidation may stem from the realization that the business is no longer capable of profitable operations.

For instance, a firm that manufactures typewriters may have chosen to voluntarily liquidate its assets upon realizing that the advent of personal computers meant that the market for typewriters would soon disappear. Voluntary liquidation may be complete voluntary liquidation or partial voluntary liquidation.

Creditor induced liquidation happens when the creditors of a business force a business to cease operation and sell off its assets. Creditors who have lent money to the business may no longer have confidence in the business’s ability to pay back the loans. As a result, when the business fails to make scheduled loan payments, the creditors may attempt to recover the loans by forcing the business to liquidate its assets.

Creditor induced liquidation may be complete creditor induced liquidation or partial creditor induced liquidation.

Government induced liquidation is distinct from a creditor induced liquidation, as the government need not have any financial interest in the business. Government induced liquidations are often justified through non-market arguments. For instance:

Government induced liquidations may also be complete or partial.

Learn more: Download CFI’s Free Liquidation Value Template.

| Complete Voluntary Liquidation | A typewriter manufacturer sells off all its assets |

| Complete Creditor Induced Liquidation | The creditors of a typewriter manufacturer force it to sell off all its assets |

| Complete Government Induced Liquidation | The government forces a typewriter manufacturer to sell off all its assets as typewriter production pollutes the environment |

| Partial Voluntary Liquidation | A typewriter manufacturer sells off all its assets except its keyboard manufacturing subsidiary |

| Partial Creditor Induced Liquidation | The creditors of a typewriter manufacturer force it to sell off all its assets except its keyboard manufacturing subsidiary |

| Partial Government Induced Liquidation | The government forces a typewriter manufacturer to sell off half its assets and use the revenue generated to install pollution filters |

CFI is the official provider of the Financial Modeling and Valuation Analyst (FMVA)™ certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover:

Learn accounting fundamentals and how to read financial statements with CFI’s online accounting classes.

These courses will give you the confidence to perform world-class financial analyst work. Start now!

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.