Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Capital used for acquisitions, growth, recaps, or MBOs/LBOs

A mezzanine fund is a pool of capital that invests in mezzanine finance for acquisitions, growth, recapitalization, or management/leveraged buyouts. In the capital structure of a company, mezzanine finance is a hybrid between equity and debt. Mezzanine financing most commonly takes the form of preferred stock or subordinated and unsecured debt. It is treated as equity on the balance sheet.

To learn more about Mezzanine Funds, launch our free corporate finance course!

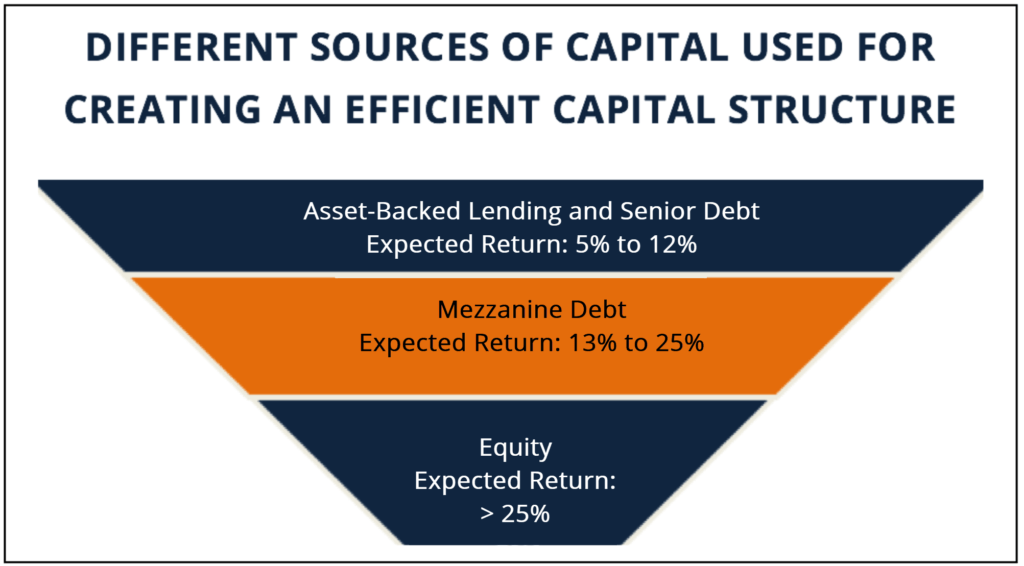

Mezzanine capital fills the gap between equity and senior debt in the capital structure of a company, which may arise due to:

Mezzanine investors receive a rate of return (RoR) of 15% to 20%, which is higher than the RoR offered on traditional forms of debt financing (such as high-yield bonds and bank loans). This is because mezzanine capital is not as liquid as traditional debt finance and is subordinate to all other debt held by the company. The return on mezzanine finance becomes available through five sources:

To learn more about Mezzanine Funds, launch our free corporate finance course!

To raise mezzanine finance, a company must have a credible track record in the industry, consistent profitability, and a feasible plan for expansion through an initial public offering (IPO) or acquisition. Thus, mezzanine finance is used by companies that have a positive cash flow.

Mezzanine debt usually has a maturity period of 5 years or more. However, if the mezzanine debt is issued at the same time as bank debt, the mezzanine debt matures after the bank debt. Furthermore, given the high RoR offered on mezzanine finance vis-à-vis traditional finance, issuers often prefer shorter maturities. Mandatory redemption/prepayment is required in the event of asset sales or a change in control transactions.

Traditionally, mezzanine capital is a buy and hold product. Thus, unlike bonds and stock, mezzanine debt securities are not traded. As a result, they have limited liquidity. Managers of a mezzanine fund need to take the non-transferability of these securities into account when managing their portfolio, it’s liquidity, and the timing of maturities.

To learn more about Mezzanine Funds, launch our free corporate finance course!

Mezzanine debt is cheaper than equity and also does not result in the dilution of existing stakeholders. When used, it reduces the need for equity. Furthermore, interest on mezzanine debt is tax-deductible. Additionally, banks are more likely to lend to a company with mezzanine funding, as the mezzanine lender is usually an institutional investor whose presence reduces the risk of lending to the company.

Thus, by using mezzanine funding, as a borrower, you can create a cost-effective capital structure with maximum funding, maximum return on equity, and minimum cost of capital.

Unlike stock (which does not guarantee the provision of dividend), a mezzanine investor is contractually entitled to interest payments monthly, quarterly, or annually. Thus, returns are more consistent and the downside risk is minimized. Furthermore, the option of converting to equity may increase the investor’s returns if the company starts doing well.

To learn more about Mezzanine Funds, launch our free corporate finance course!

We hope this overview of a Mezzanine Fund has been a helpful starting point for you. In order to keep learning about other investment vehicles and corporate finance in general, we highly recommend these related CFI articles: