Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The use of significant leverage for acquisitions

In corporate finance, a leveraged buyout (LBO) is a transaction in which a company is acquired using debt as the primary source of consideration. These transactions typically occur when a private equity (PE) firm borrows as much as it can from a variety of lenders (up to 70 or 80 percent of the purchase price) and funds the balance with its own equity.

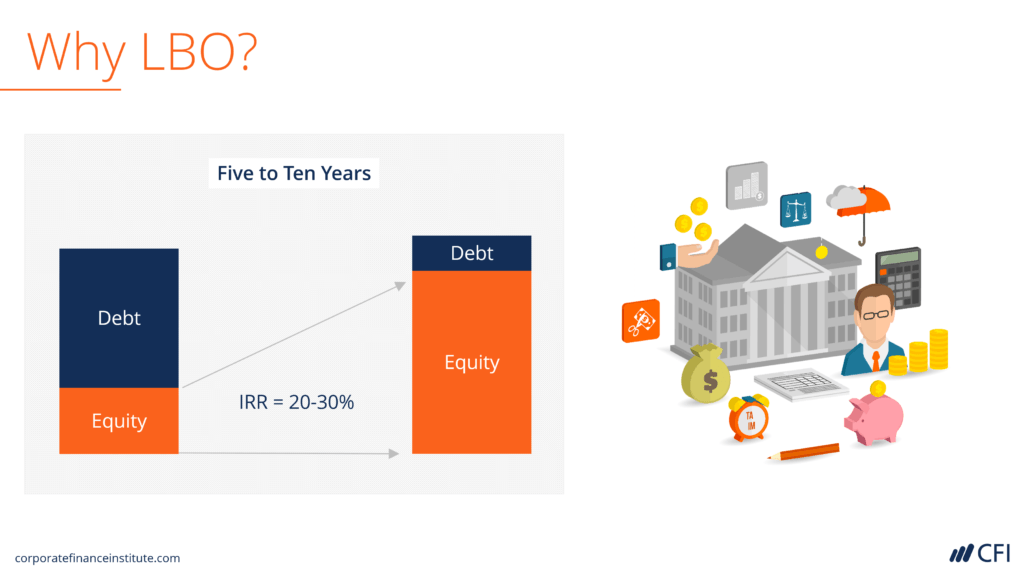

Simply put, the use of leverage (debt) enhances expected returns to the private equity firm. By putting in as little of their own money as possible, PE firms can achieve a large return on equity (ROE) and internal rate of return (IRR), assuming all goes according to plan. Since PE firms are compensated based on their financial returns, the use of leverage in an LBO is critical in achieving their targeted IRRs (typically 20-30% or higher).

While leverage increases equity returns, the drawback is that it also increases risk. By strapping multiple tranches of debt onto an operating company, the PE firm is significantly increasing the risk of the transaction (which is why LBOs typically pick stable companies). If cash flow is tight and the economy of the company experiences a downtur,n they may not be able to service the debt and will have to restructure, most likely wiping out all returns to the equity sponsor.

Generally speaking, companies that are mature, stable, non-cyclical, predictable, etc. are good candidates for a leveraged buyout.

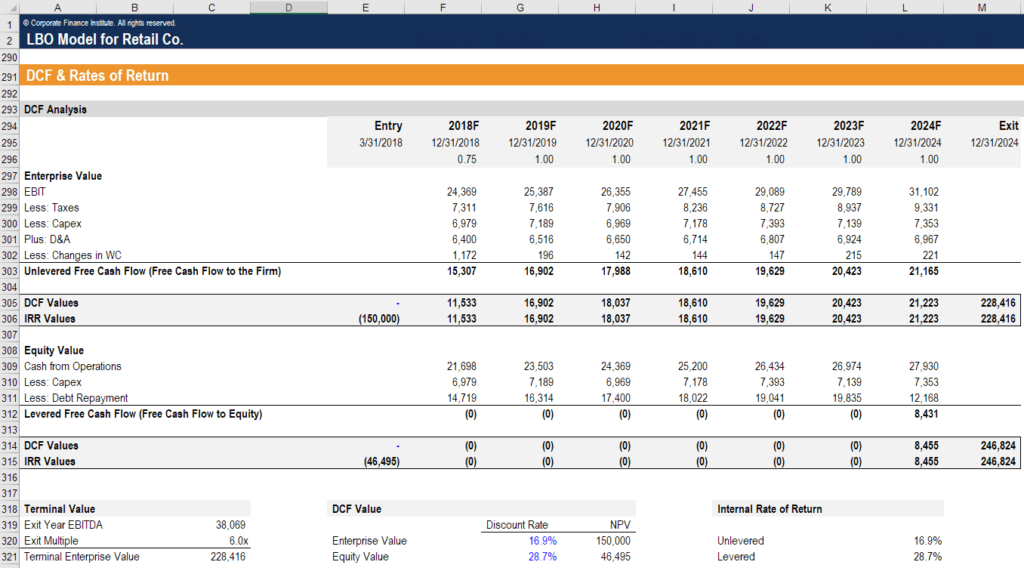

Given the amount of debt that will be strapped onto the business, it’s important that cash flows are predictable, with high margins and relatively low capital expenditures required. This steady cash flow is what enables the company to easily service its debt. In the example below, you can see from the charts how all available cash flow is allocated towards repaying debt, and the total debt balance (far right chart) steadily decreases over time.

The above screenshot is from CFI’s LBO Model Modeling Course.

The LBO analysis starts with building a financial model for the operating company on a standalone basis. It involves building a forecast that extends five years into the future (on average) and calculating a terminal value for the final period.

The analysis will be presented to banks and other lenders in an effort to secure as much debt as possible, thereby maximizing returns on equity. Once the amount and rate of debt financing are determined, the model is updated, and the final terms of the deal are finalized.

After the transaction closes, the work has just begun, as the PE firm and management must add value to the business by growing the top line, reducing costs, paying down debt, and ultimately realizing their return.

Image Source: CFI’s Leveraged Buyout Modeling Course.

When it comes to a leveraged buyout transaction, the financial modeling that’s required can get quite complicated. The added complexity arises from the following unique elements of a leveraged buyout:

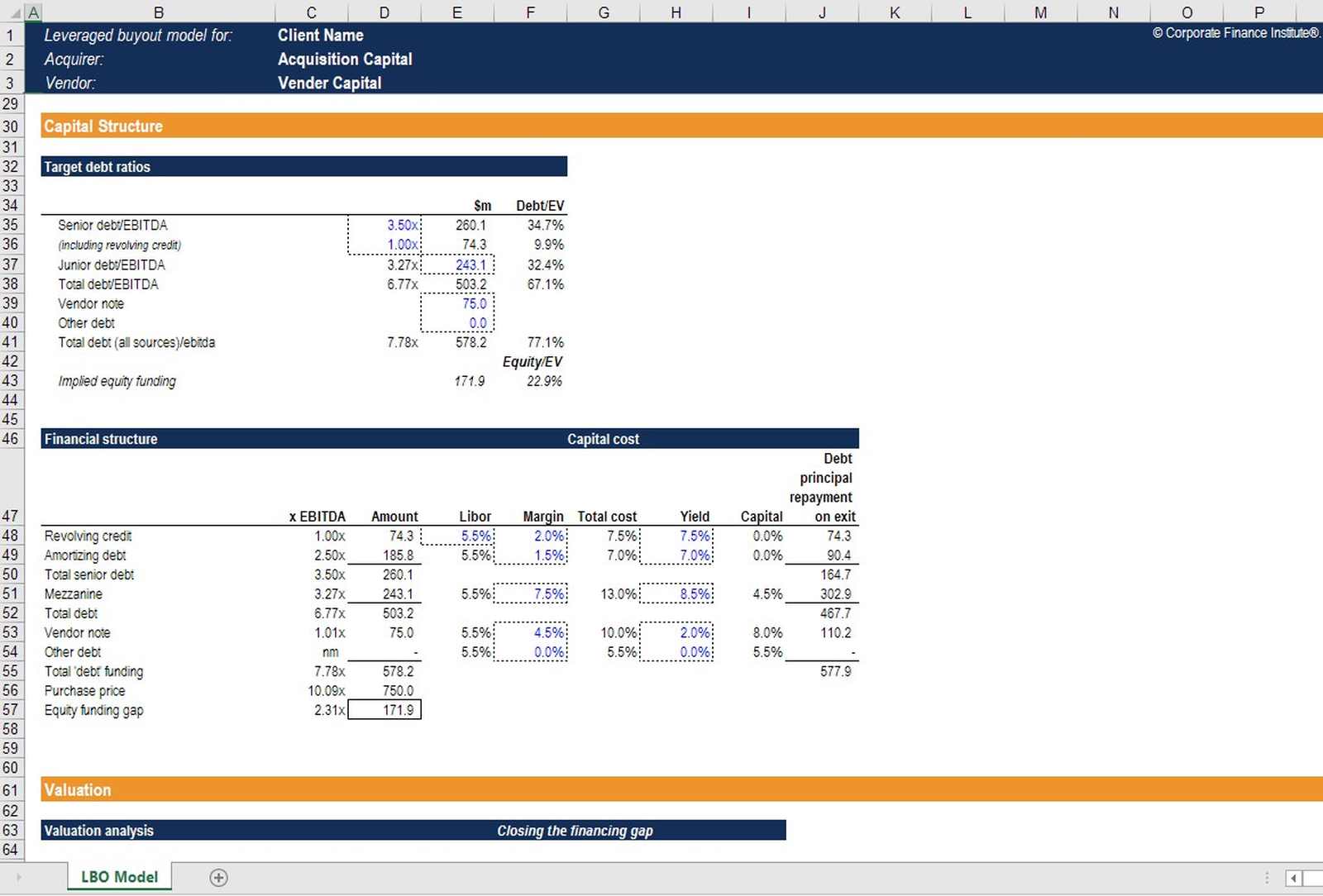

Below is a screenshot of an LBO model in Excel. This is one of many financial modeling templates offered in CFI courses.

To learn more about the above model with step-by-step instructions, launch CFI’s LBO Modeling Course now!

Thank you for reading CFI’s guide to Leveraged Buyout (LBO). To further your education, see the following CFI resources: