Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The cost of debt is the return that a company provides to its debt holders and creditors

The cost of debt is the return that a company provides to its debtholders and creditors. These capital providers need to be compensated for any risk exposure that comes with lending to a company.

Since observable interest rates play a big role in quantifying the cost of debt, it is relatively more straightforward to calculate the cost of debt than the cost of equity. Not only does the cost of debt reflect the default risk of a company, but it also reflects the level of interest rates in the market. In addition, it is an integral part of calculating a company’s Weighted Average Cost of Capital or WACC.

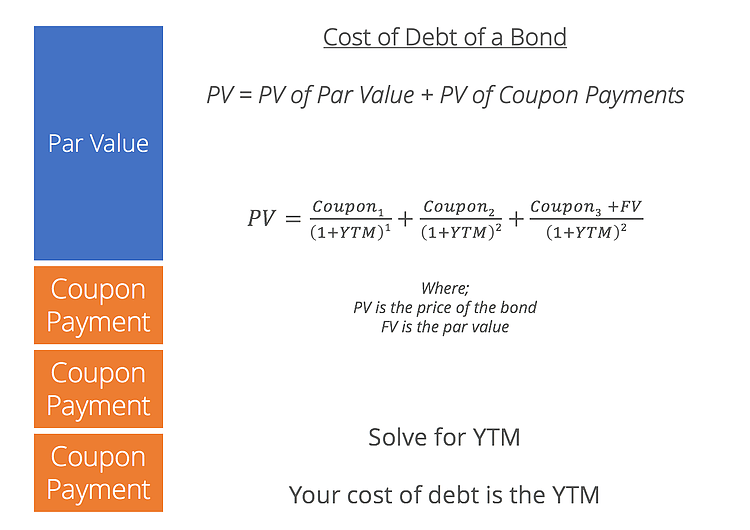

There are two common ways of estimating the cost of debt. The first approach is to look at the current yield to maturity or YTM of a company’s debt. If a company is public, it can have observable debt in the market. An example would be a straight bond that makes regular interest payments and pays back the principal at maturity.

This approach is widely used when the company being analyzed has a simple capital structure, where it does not have multiple tranches of debt, including subordinated debt or senior debt, for example, with each having significantly different interest rates.

Click the button below to download our free Cost of Debt template!

The other approach is to look at the credit rating of the firm found from credit rating agencies such as S&P, Moody’s, and Fitch. A yield spread over US treasuries can be determined based on that given rating. That yield spread can then be added to the risk-free rate to find the cost of debt of the company. This approach is particularly useful for private companies that don’t have a directly observable cost of debt in the market.

Simply put, a company with no current market data will have to look at its current or implied credit rating and comparable debts to estimate its cost of debt. When comparing, the capital structure of the company should be in line with its peers.

When neither the YTM nor the debt-rating approach works, the analyst can estimate a rating for the company. This happens in situations where the company doesn’t have a bond or credit rating or where it has multiple ratings. We would look at the leverage ratios of the company, in particular, its interest coverage ratio. A higher number for this ratio means a safer borrower. The yield spread can then be estimated from that rating.

When obtaining external financing, the issuance of debt is usually considered to be a cheaper source of financing than the issuance of equity. One reason is that debt, such as a corporate bond, has fixed interest payments. In equity financing, however, there are claims on earnings. The larger the ownership stake of a shareholder in the business, the greater he or she participates in the potential upside of those earnings.

Another reason is the tax benefit of interest expense. The income tax paid by a business will be lower because the interest component of debt will be deducted from taxable income, whereas the dividends received by equity holders are not tax-deductible. The marginal tax rate is used when calculating the after-tax rate.

The true cost of debt is expressed by the formula:

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to calculating the cost of debt for a business. To learn more, check out the free CFI resources below: