Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

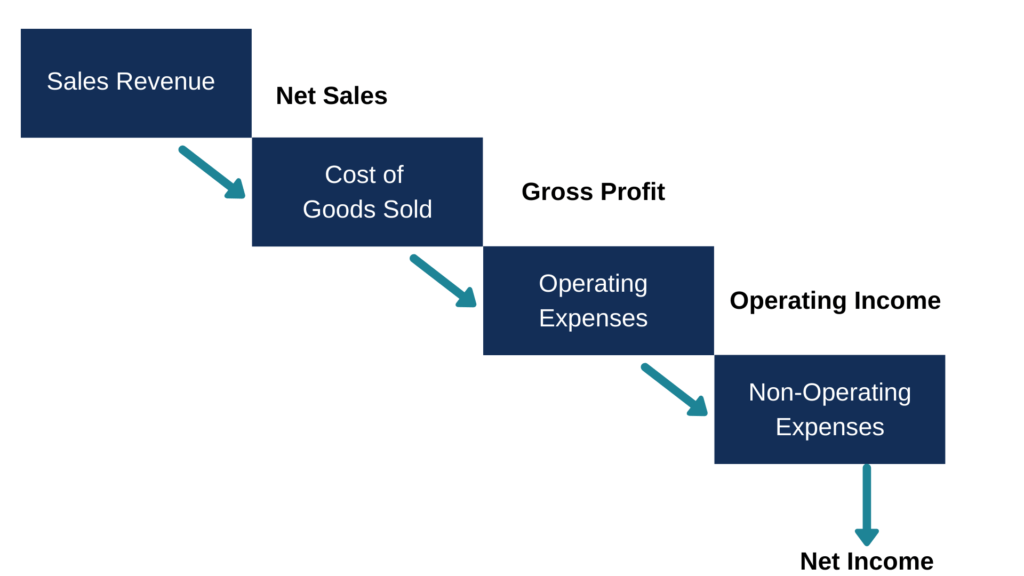

An income statement that segregates total revenue and expenses into operating and non-operating heads

A multi-step income statement is an income statement that segregates total revenue and expenses into operating and non-operating heads. It offers an in-depth analysis of the business’s financial performance in a specific reporting period. It lists items in different categories to make it convenient for users of the income statement to better understand the core operations of the business.

Users can gain insights into how a company’s primary business activities generate revenue and affect costs compared to the performance of the non-primary business activities. A multi-step income statement is an alternative to the single-step income statement.

The following are the key components of a multi-step income statement:

Gross profit is the first section of a multi-step income statement, and it is obtained by deducting the cost of goods sold from the total sales. It shows how profitable a company is in manufacturing or selling its products. Gross profit is used by creditors to show the company’s ability to meet arising debt obligations and to pay back outstanding credit.

Investors also use the gross profit to determine the profitability of primary business activities and the general health of the company. When calculating gross profit, no other expenditures are included apart from the cash inflow from the sale of goods and cash outflow from the purchase of goods.

Gross Profit= Net Sales – Cost of Goods Sold

The selling and administration expenses from operating activities are captured in the second section of a multi-step income statement. The selling expenses are the costs incurred when selling goods to consumers and may include marketing expenses, the salary of sales personnel, and freight charges.

Administrative expenses are costs that are indirectly related to the sale of goods and may include the salary of the office personnel, rental expenses, etc. The total operating expenses are obtained by adding both selling expenses and administrative expenses. The operating income is then calculated as follows:

Operating Income = Gross Profit – Operating Expenses

The third section is the non-operating head, which lists all business incomes and expenses that are not related to the principal activities of the business. An example of a non-operating expense is a lawsuit claim paid by the company as compensation to an aggrieved party after losing in a court case. Also, a non-operating income can be an insurance compensation paid by an insurance firm to the company’s account as settlement proceeds for damage or loss of a company’s asset.

For an expense or income to be treated as non-operating, the loss, interest, or gain should be from an extraordinary item that is not part of the company’s ordinary business. Once the items in the non-operating head are summed up, the net income for the particular period is computed as follows:

Net Income = Operating Income + Non-Operating Items

The multi-step income statement helps users analyze the performance of the business. Investors, lenders, and other key stakeholders monitor the gross margin of the business, which is calculated as a percentage of net sales. The gross margin is then compared to the company’s past gross margins and other comparable entities’ gross margins to determine how efficiently the company is performing.

The multi-step income statement categorizes operating and non-operating incomes and expenses. It helps users evaluate the financial performance of the organization. The users will know the profit earned from the primary activities of buying and selling goods and how it differs from the non-operating activities.

The income statement shows the total revenue attributable to the primary activities of the business, excluding revenues from non-merchandise-related sales.

A multi-step income statement is ideal for large, complex businesses that use a long list of incomes and expenses. For example, large manufacturing companies with multiple sources of revenue should prepare a multi-step income statement so that the incomes and expenses from primary business activities are differentiated from non-essential activities.

Publicly traded companies are also required to create multi-step income statements since they are under greater scrutiny from both regulators and the public, and they must present detailed financial reports that distinguish between primary and non-primary business activities.

A single-step income statement uses a single equation to compute the net income of the business, and it is a more simplified report compared to a multi-step income statement. It presents the revenue, expenses, and profit or loss generated by the business during a particular period, but it uses a single equation to calculate profits. The equation is as follows:

Net Income = (Revenue + Gains) – (Expenses + Losses)

On the other hand, a multi-step income statement follows a three-step process to calculate the net income, and it segregates operating incomes and expenses from the non-operating incomes. It separates revenues and expenses from activities that are directly related to the business operations from activities that are not directly tied to the operations.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to Multi-Step Income Statement. To keep learning and advancing your career, the following resources will be helpful: