Get In-Demand Finance Certifications

A discrete and uniform span of time for reporting (and analyzing) a company's financial performance and financial position

A reporting period, also known as an accounting period, is a discrete and uniform span of time for which the financial performance and financial position of a company are reported and analyzed. In other words, the data contained in the financial statements are generated by the company’s finance professionals from operations during the reporting period.

A company usually engages in many continuous activities. The activities can be broken down into specific, distinct, and short intervals for the purpose of financial reporting. Without a reporting period, accountants wouldn’t know the start and ending date to create financial reports.

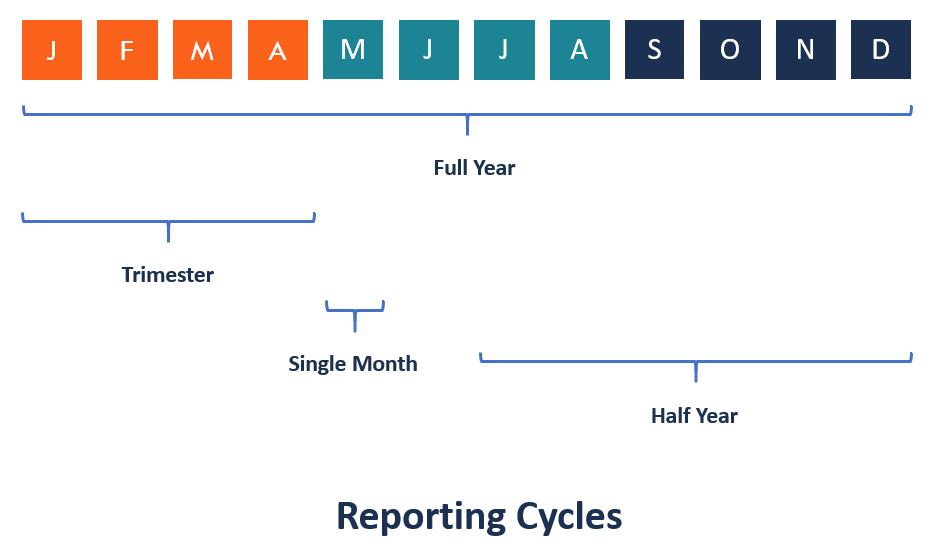

Depending on the interested audience’s requirements, the reporting period can be for a month, quarterly, semi-annually, or annually. If the accounting period of a company is for a 12-month period but ends on a date other than December 31, it is referred to as a fiscal year or financial year, as opposed to a calendar year.

A fiscal year sets the start of the reporting period to any date, and financial data is aggregated for a year after said date. For example, a fiscal year beginning November 1 would end October 31 of the following year. The fiscal year should ideally end on a date when there is a low business activity. At this point, there are usually fewer assets and liabilities to be audited.

A reporting period can also be for a shorter period of time, such as a month, a week or a few days. It usually happens when a business just started operating or when it is ending its operations before the end of the usual accounting period. Such a period can also be used when a company is being taken over by a new corporate parent.

The preparation of internal documents (for internal financial reporting), such as employee tax records, duplicate purchase orders, and inventory reports, can depend on monthly or quarterly accounting periods. External accounts, like income statements, usually depend on annual accounting periods.

Time plays a significant role in accounting and financial reporting. The reporting period helps the company to organize its financial reporting for users who are interested in the financial status of the business. Users of the company’s financial statements need to have reliable and current financial information to assess the performance and position of the company. It helps them to make important business decisions and take proper action in a timely manner. The users include employees, internal management, investors, creditors, government agencies, etc.

The company’s internal management needs to see financial reports more than once a year to be able to forecast future sales, expenses, and staffing accurately. Employees are usually interested in the company’s financial status because it can affect their job security. They may also take part in the profit-sharing. It means that the better the company performs, the more money they will build for retirement.

Current and potential creditors, as well as investors, need to see how well the business is performing in comparison to previous accounting periods. With this information, they will be able to decide whether they want to enter into or continue with business relations with the company.

The following are the financial statements that are usually prepared for a reporting period. The relevant accounting period is normally stated in the header of the financial reports.

The income statement/profit and loss statement shows interested parties how profitably the company carried out its operations during the reporting period. It includes revenues, expenses, losses, and gains.

The balance sheet/statement of financial position shows the financial position of the company at the end of the reporting period. It includes the company’s assets, liabilities, and stockholder’s equity.

The cash flow statement discloses how well an entity generated cash to fund its operating expenses, settle its debt obligations, and fund its investments during the reporting period.

The statement of retained earnings shows the portion of the company’s profit that’s been distributed among its owners and the portion kept in the company for future growth.

To make comparisons between the current financial statements and those from previous years, organizations will use the same reporting periods year-to-year. An entity that experiences consistency in growth in year-to-year accounting periods displays stability and a stance of long-term profitability. The uniformity of customer reporting periods also enables a different company to perform comparative analysis.

Thank you for reading CFI’s guide to Reporting Period. To keep learning and developing your knowledge base, please explore the additional relevant resources below:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: