Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

A short-term funding method that a business can draw on using its accounts receivables

Accounts receivable financing is a means of short-term funding that a business can draw on using its receivables. It is very useful if a timing mismatch exists between the cash inflows and outflows of the business. AR financing can take various forms, but the three major types are:

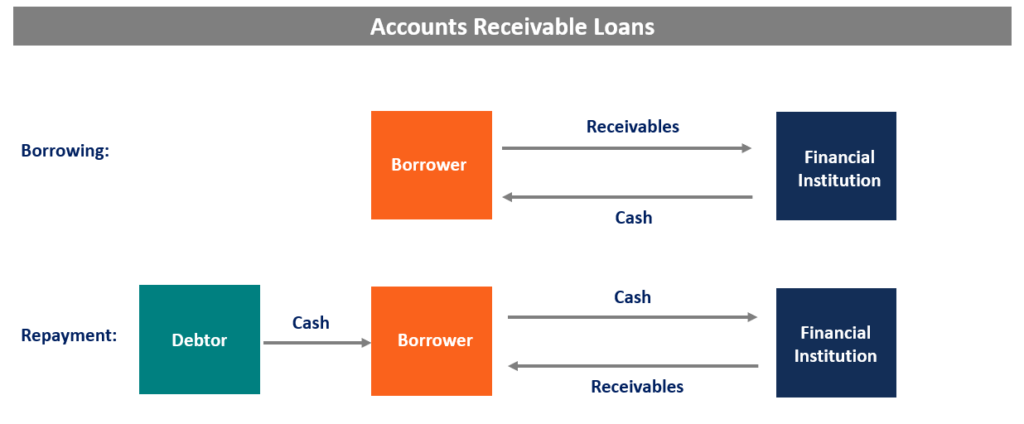

Accounts receivable loans are a source of short-term funding, where the borrower can use their accounts receivables as collateral to raise funds from a bank. The bank would typically lend a fraction – e.g., 80% – of the face value of the receivables. The fraction varies depending on the quality of receivables – the better the quality, the higher the fraction.

The borrower still owns the receivables and is responsible for collecting from their debtors. A business should only use AR loans if it keeps a good relationship with its debtors and is sure of the payments. Otherwise, there is a chance that a business might get squeezed between the bank and the debtor.

Factoring is the most common form of accounts receivable financing for smaller businesses. Under the factoring approach, the borrower sells its receivables to a factoring institution. The receivables are sold at a discount, where the discount depends on the quality of the receivables.

Since it is an outright sale of receivables, the borrower is no longer responsible for the collection process, and the amounts are collected by the factoring organization. Factoring can be expensive, as it typically involves several fees alongside interest expense. Also, if a business wishes to maintain good relationships with its debtors, then it should use factoring sparingly.

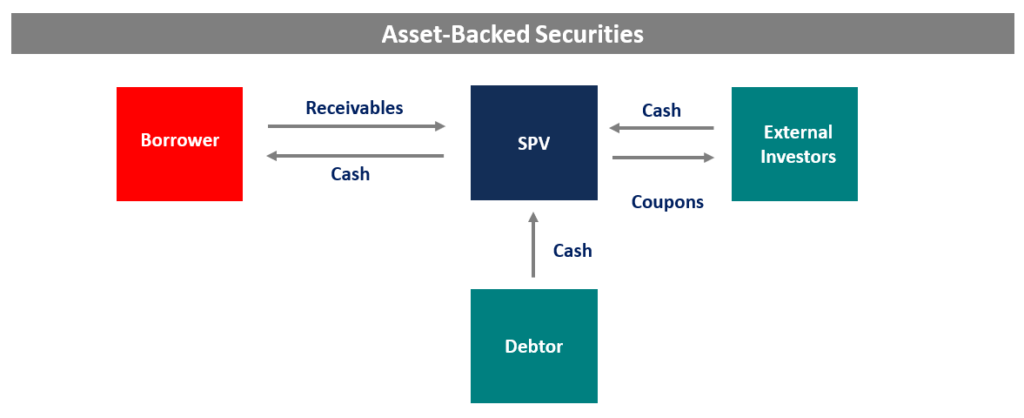

Asset-backed securities (ABS) are a form of financing available to larger organizations. An ABS is a fixed-income instrument that makes coupon payments to its investors by deriving its cash flows from a pool of underlying assets. The most common example is that of mortgage-backed securities that use mortgages as their underlying assets.

A large company can securitize some or all of its receivables in a special purpose vehicle (SPV); the instrument holds the receivables, collects payments, and passes them through to the investors.

On the other hand, the borrowing company gets money from the investors via the SPV. Again, as in the case of AR loans and factoring, the credit rating of the ABS depends on the quality and diversification level of the receivables.

As discussed in the previous sections, the quality of receivables is key in making financing decisions. Below are a few key factors that decide the quality of a basket of receivables:

The credit quality of the debtor is essential, as it is ultimately the debtor who makes the payment. So, a debtor with a poor credit rating reduces the quality of the basket and increases the cost of borrowing in terms of interest or reduction of the amount being lent.

The duration, or age, of receivables is the number of days they are outstanding. Long-duration receivables are considered to be of lower quality because the probability of the receivables being paid goes down.

Typically, if a receivable is outstanding for more than 90 days, it is treated as a default. Hence, the shorter the duration of the basket, the lower the cost of financing.

The industry to which the original debtor belongs is important, as the macro trends within that industry affect the ability of the debtor to make good on their obligations. It is also important because financial institutions may want to restrict their exposure to certain industries.

The quality of documentation that is associated with the account is also very important, as better documentation quality provides clarity of contracts. It also provides the basis for legal recourse in case of a default. Thus, good and clear documentation improves the quality of the receivables basket.

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover:

Learn accounting fundamentals and how to read financial statements with CFI’s online accounting classes.

These courses will give you the confidence to perform world-class financial analyst work. Start now!

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.