Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

A derivative contract that gives the buyer the right but not the obligation to buy or sell currencies at a given exchange rate and within a specified time frame

A currency option refers to a derivative contract that gives the buyer the right but not the obligation to sell or buy currencies at a specified exchange rate within a specified time frame. They are useful for investors to hedge against unfavorable movements in exchange rates.

The spot rate is the current exchange rate.

The strike price is the exchange rate at which the contract can be exercised.

A call option provides the buyer with the right to buy a currency at the strike price.

A put option provides the buyer with the right to sell a currency at the strike price.

Buying a call on USD is the same as buying a put on the CAD because in both cases, the buyer is selling CAD for USD.

An expiration date provides the time frame in which the option contract is valid.

The contract size is an essential element that determines how much currency is being settled.

American options can be exercised by the buyer at any point prior to and on the expiration date.

European options are limited only to be exercised on the expiration date.

In-the-money occurs when the option can be exercised, allowing the buyer to buy at the strike price that is better than the spot rate.

Out-of-the-money occurs when the option will not be exercised because it is more expensive than buying at the spot rate.

The premium is the amount paid by the buyer to the seller for the options contract. The premium amount is determined by supply and demand, as well as if the strike price is in-the-money or out-of-the-money.

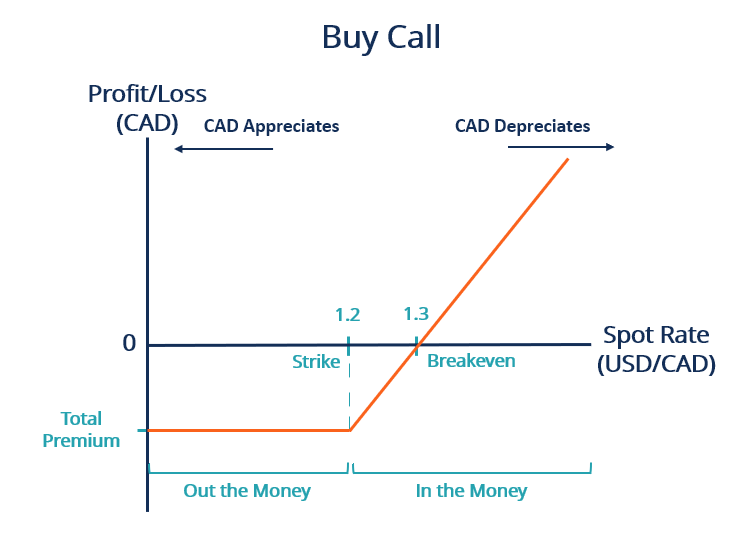

The diagram above represents the profit/loss based on the spot rate at the option’s expiration or time of exercise.

In the example above, the buyer wants to sell CAD and buy USD but expects the CAD to depreciate relative to the USD in the future. To hedge against the depreciation of the CAD (or vice versa, the appreciation of the USD), the buyer purchases a call on the USD.

The strike price is set at 1.2 USD/CAD, giving the buyer the right to sell CAD at 1.2 USD/CAD before expiration. If the CAD depreciates more than 1.2 USD/CAD to the right, the buyer will exercise the option because it is in-the-money. At the strike price, the buyer is indifferent between exercising or not, ignoring any potential exercising fees. However, if the CAD appreciates against the USD to the left of the strike, the option is worthless because it is out-the-money, and the buyer incurs a loss of the total premium paid for the option.

The total premium is calculated as the premium multiplied by the contract size. With a contract size of 50,000 USD and a premium of 0.1 CAD, the total premium paid is 0.1*50,000 = 5,000 CAD. This amount also represents the maximum loss on the contract.

The breakeven spot rate is calculated as the strike price + the premium. In this example, the breakeven = 1.2 + 0.1 = 1.3 USD/CAD. We can think of this breakeven rate as the spot rate needed to earn back the total premium paid.

At the breakeven, the buyer will exercise the call and sell CAD at 1.2 USD/CAD while the market is at 1.3 USD/CAD. The gain is the difference between the strike price and spot rate, multiplied by the contract size. The buyer gains (1.3-1.2)*50,000 = 5,000 CAD. The gain is the exact amount to offset the total premium incurred for the contract.

Any spot rate between the strike and breakeven still incurs an overall loss because the gains are not enough to offset the total premium. Consequently, for the buyer to make money from the contract, they must expect that the CAD will depreciate past the breakeven of 1.3 USD/CAD.

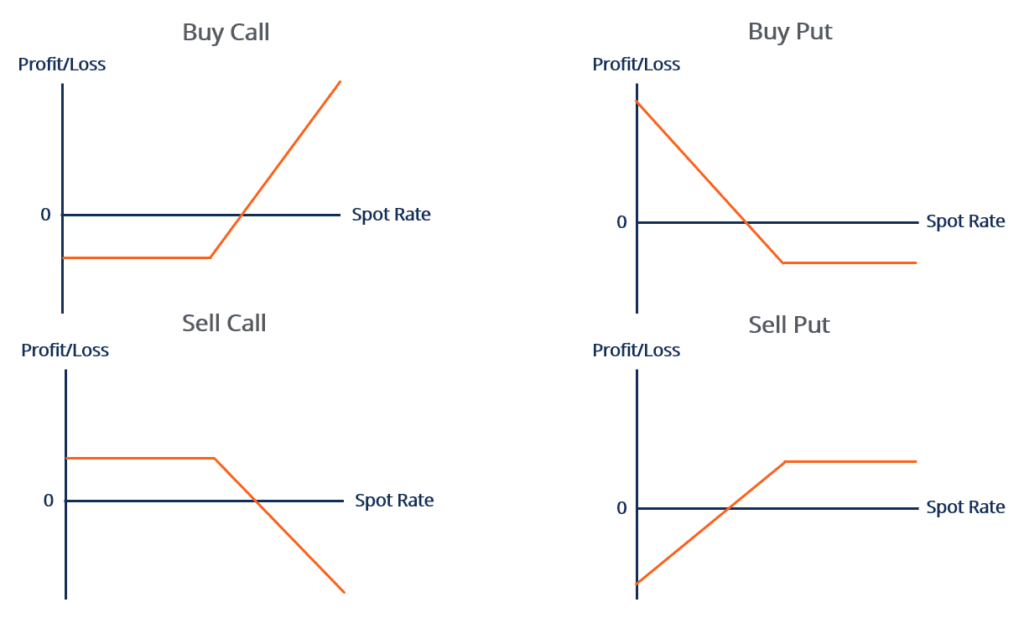

The same concept applies to other currency options, as shown above.

Option contracts are a zero-sum game. When the buyer exercises their in-the-money option, their profits come from the losses of the seller. If the buyer does not exercise their out-the-money option, the seller makes profits from the premium paid by the buyer. While the buyer can choose whether or not to exercise the option, the seller is left with no choice and is obligated to honor the buyer’s choice.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI is the official provider of the global Capital Markets & Securities Analyst (CMSA)® certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful: