Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

A framework to represent forward interest rates using an existing term structure of interest rates

The Heath-Jarrow-Morton Model – also known as the HJM Model – is a framework to represent forward interest rates using an existing term structure of interest rates. The model was created based on the work developed by David Heath, Robert A. Jarrow, and Andrew Morton during the late 1980s. Their research papers led to the establishment of the model that we know today.

The purpose of using the HJM Model is to predict forward interest rates so that the predictions can be used to calculate the prices of securities affected by interest rate movements, including securities such as bonds and options.

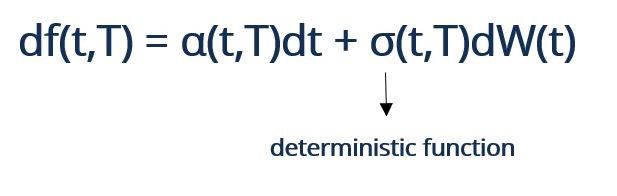

The model can be mathematically represented by the following general formula:

Where:

There are several assumptions presented by the Heath-Jarrow-Morton Model, such as:

Investors use the Heath-Jarrow-Morton Model to determine the prices of securities that are impacted by interest rate fluctuations. By being able to price securities, investors can identify arbitrage opportunities to earn a riskless profit when there are differences between the market price of a security and its price calculated using the Heath-Jarrow-Morton Model.

In particular, the model can be used to price financial derivatives because the value of derivatives depends on the term structure of underlying assets. For example, the underlying asset for credit derivatives is the price of risky zero-coupon bonds. In addition to arbitrage seekers, it can also be used by asset-liability management.

When the drift and volatility of the instantaneous forward rate are assumed to be deterministic, it is known as the Gaussian Heath-Jarrow-Morton Model. In the mathematical formula, it is when σ becomes a deterministic function.

The Heath-Jarrow-Morton Model is often compared with other models when investors assess different strategies to price financial derivatives. They are often compared with short-rate models, but they are different from each other. The HJM Model represents the entire forward rate curve, but short-rate models only demonstrate a specific point on the curve.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI offers the Capital Markets & Securities Analyst (CMSA)® certification program for those looking to take their careers to the next level. To keep learning and developing your knowledge base, please explore the additional relevant resources below: