Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

A method of calculating the depreciation of certain types of assets in special circumstances

The Alternative Depreciation System (ADS) is a method of calculating the depreciation of certain types of assets in special circumstances. The ADS system is required by the Internal Revenue Service (IRS), and it typically increases the number of years over which the asset is depreciated. Therefore, it reduces the depreciation expense recorded each year.

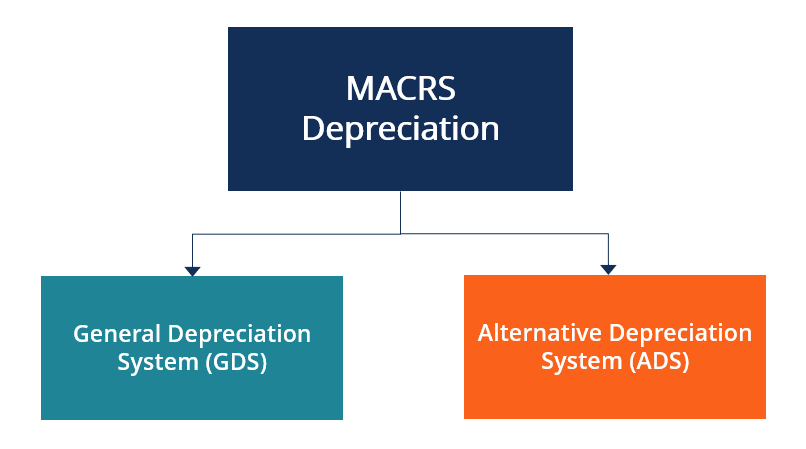

Under the Internal Revenue Service (IRS), any business assets that are acquired after 1986 must be depreciated using MACRS. MACRS is used for depreciation for federal income tax purposes and is a popular system in the United States. It is normally used if businesses wish to accelerate the depreciation of their assets. Under the MACRS method, a larger depreciation expense can be recorded in earlier years and lower depreciation in later years of asset ownership.

There are two depreciation systems under MACRS: the General Depreciation System (GDS) and the Alternative Depreciation System (ADS). GDS is normally used in practice; however, in certain circumstances (which will be outlined later), ADS is used. Once a company uses the ADS method, it cannot shift back to GDS.

The General Depreciation System (GDS) is the most commonly used MACRS depreciation system and uses a declining balance to depreciate assets. Under GDS, the depreciation rate is applied to the non-depreciated balance. Relative to ADS, GDS uses shorter recovery periods. The asset classes under the IRS can be subject to different recovery periods for GDS and ADS methods.

The ADS method calculates depreciation using a straight-line method over a longer period of time relative to GDS. There are certain situations where businesses can choose to use ADS instead of GDS, and for that, they need to use the IRS Form 4562 – Depreciation and Amortization, which allows them to select which system to use (made on an asset class basis). Once a system is chosen, it cannot be changed for that asset class in the given tax year.

ADS is generally used by small companies or those with high growth who do not possess enough immediate taxable income. Using the ADS method would provide benefits to such companies over using the GDS method, as they can record lower depreciation in the earlier years, resulting in higher profitability. ADS provides for equal yearly deductions, except for the first and last years.

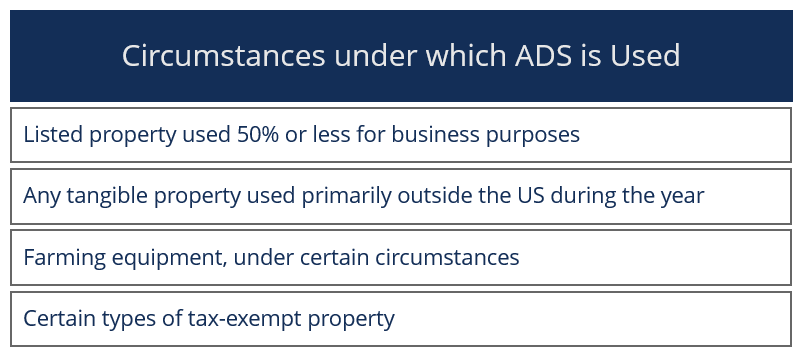

The list below shows circumstances where a company may use ADS. The list, however, is not exhaustive, as there are several other conditions where ADS can be used.

In certain cases, depreciation is required to be recalculated for Alternative Minimum Tax (AMT) purposes. AMT is a separate tax that reduces the deductions of taxpayers. The ADS method must be used when making AMT adjustments. ADS is also used to compute depreciation for earnings and profits purposes.

IRS Publication 946 mentions recovery periods for different asset classes under the GDS and ADS methods. Some prominent asset recovery periods are mentioned below as examples:

Accelerated depreciation is used by many companies, and looking at historic corporate data, the depreciation method creates proportionally large corporate tax expenditures. The companies must prepare schedules to determine the depreciation rate of various assets, and the effective tax rates on these investments will vary.

An advantage of accelerated depreciation is that it provides tax benefits to certain asset classes because the higher deduction reduces taxes payable.

On the other hand, a disadvantage of accelerated depreciation is that it may distort business decisions, as companies may seek to replace depreciated assets even when they still have useful lives.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s explanation of the Alternative Depreciation System. To keep advancing your career, the additional resources below will be useful: