Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Journal entries to close off the year

A closing entry is a journal entry that is made at the end of an accounting period to transfer balances from a temporary account to a permanent account.

Companies use closing entries to reset the balances of temporary accounts − accounts that show balances over a single accounting period − to zero. By doing so, the company moves these balances into permanent accounts on the balance sheet. These permanent accounts show a company’s long-standing financials.

Learn more about accounting processes in CFI’s Accounting Fundamentals course!

Temporary accounts are accounts in the general ledger that are used to accumulate transactions over a single accounting period. The balances of these accounts are eventually used to construct the income statement at the end of the fiscal year.

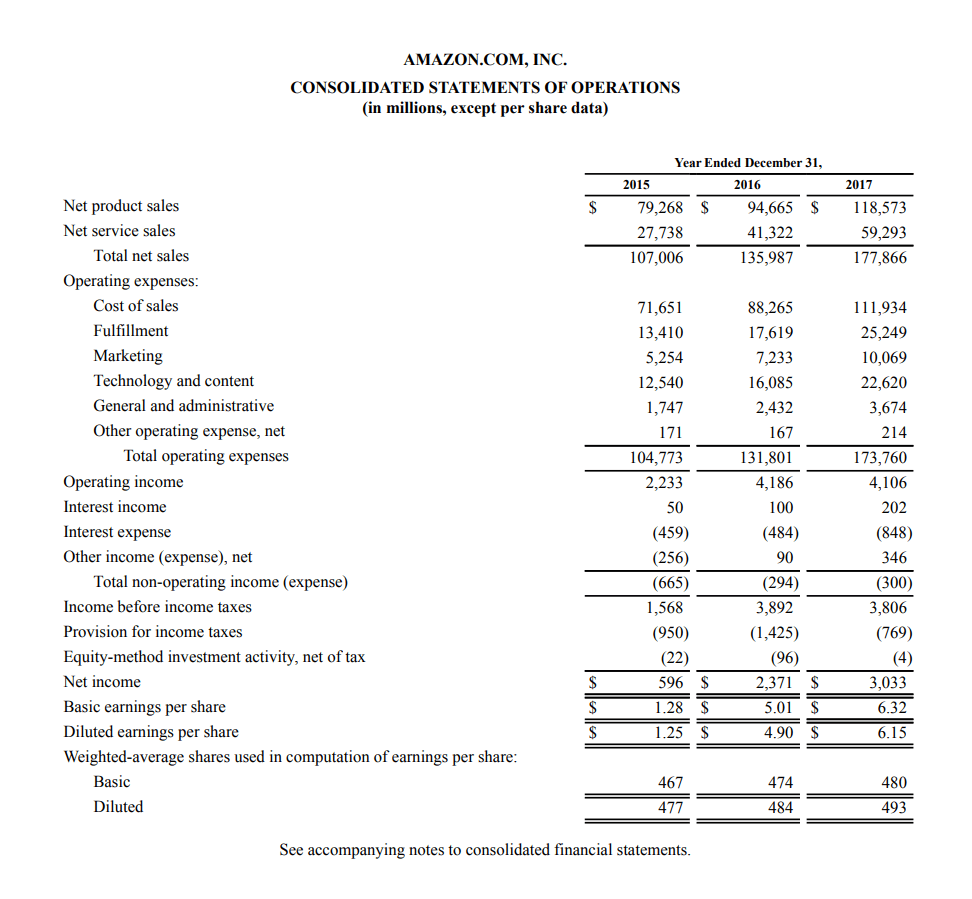

The income statement is a financial statement that is used to portray a company’s financial performance and activities over a single fiscal year. It is for this reason that the date line in the annual income statement is written as “Year ended.”

Below is an example of Amazon’s 2017 annual income statement. You can see that the date is written as “Year ended December 31, YYYY”.

Learn to read financial statements in CFI’s free reading financial statements course!

As mentioned, temporary accounts in the general ledger consist of income statement accounts such as sales or expense accounts. When the income statement is published at the end of the year, the balances of these accounts are transferred to the income summary, which is also a temporary account.

The income summary is used to transfer the balances of temporary accounts to retained earnings, which is a permanent account on the balance sheet.

The income summary is a temporary account used to make closing entries.

All temporary accounts must be reset to zero at the end of the accounting period. To do this, their balances are emptied into the income summary account. The income summary account then transfers the net balance of all the temporary accounts to retained earnings, which is a permanent account on the balance sheet.

Permanent accounts are accounts that show the long-standing financial position of a company. Balance sheet accounts are permanent accounts. These accounts carry forward their balances throughout multiple accounting periods.

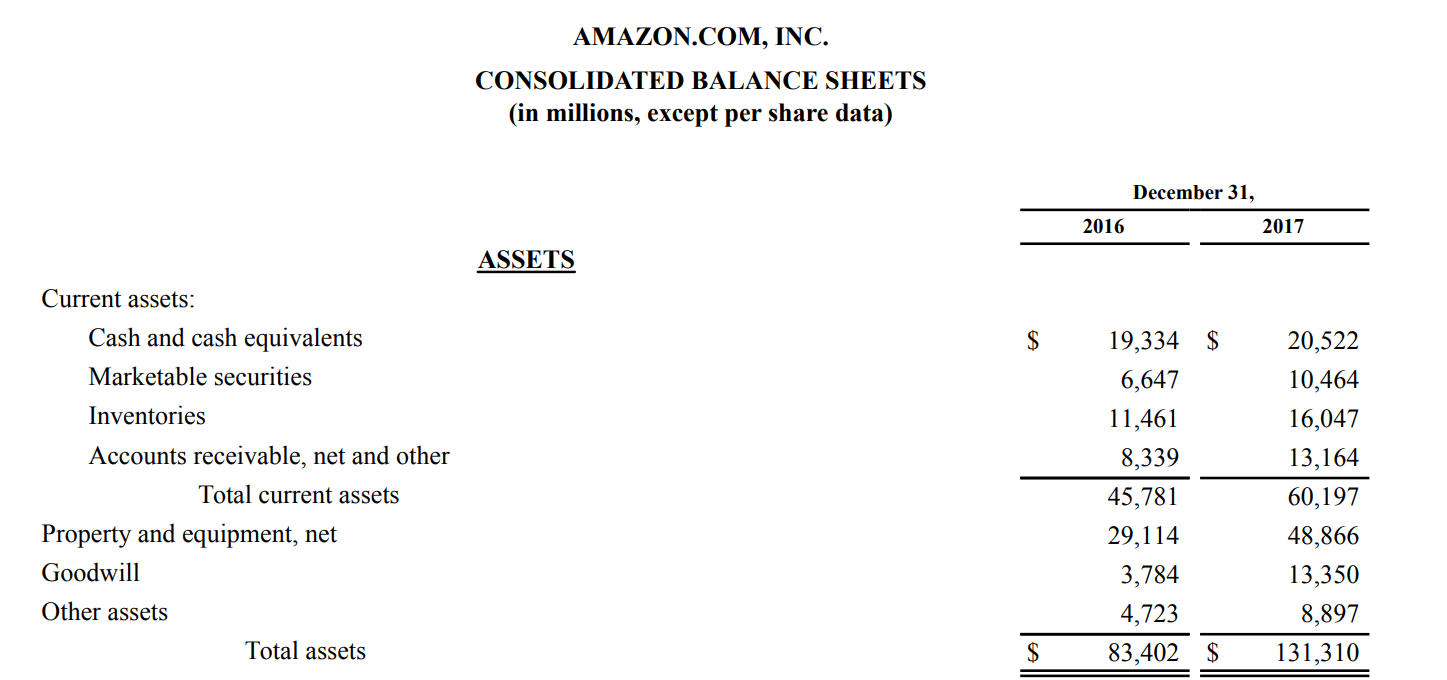

To understand this better, we can look at an account such as inventory. Below is an excerpt from Amazon’s 2017 annual balance sheet.

Learn to read financial statements in CFI’s free reading financial statements course!

The balance sheet captures a snapshot of a company at a given point in time. By looking at this balance sheet, we can observe the following:

Looking at it this way, we can see that Inventory is a permanent account that carries forward balances across multiple accounting periods.

Below are examples of closing entries that zero the temporary accounts in the income statement and transfer the balances to the permanent retained earnings account. This is done using the income summary account.

Clear the balance of the revenue account by debiting revenue and crediting income summary.

Clear the balance of the expense accounts by debiting the income summary and crediting the corresponding expenses.

Close the income summary account by debiting income summary and crediting retained earnings.

Close the dividends account by debiting retained earnings and crediting dividends.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thanks for reading CFI’s closing entry guide. Corporate Finance Institute has other resources that will help you expand your knowledge and advance your career! Check out the links below: