Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

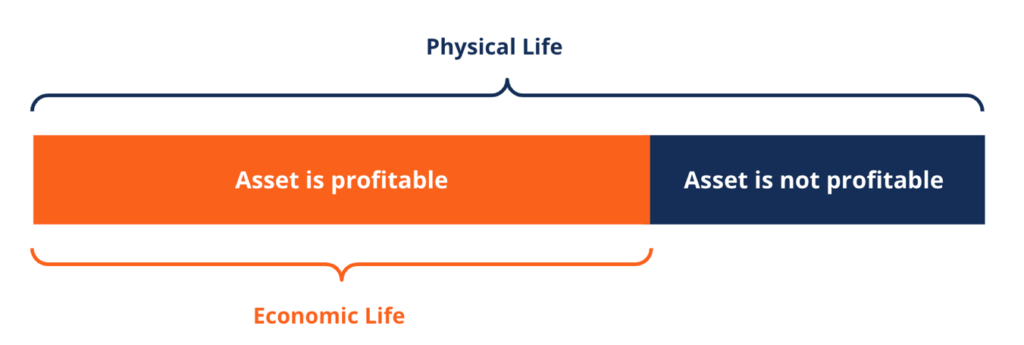

The length of time an asset is expected to be useful to the owner

Economic life refers to the length of time an asset is expected to be useful to the owner. It is also called useful life or depreciable life. The measure of an asset’s usefulness is how profitable it is to keep – in other words, how long an asset generates more income than it costs to maintain and operate.

When calculating economic life, it is commonly assumed that the asset will be operated at a normal level of usage and with preventative maintenance. An asset’s economic life is not always the same length as its physical life. An asset could still be functioning as it is supposed to, but not considered economically useful. Because economic life is an estimation, an asset’s physical life can exceed its economic life or vice versa. This is also the case when new technological innovations make old technology obsolete.

In some cases, the owner or company will designate an arbitrary number of years to define an asset’s economic life. To estimate the number, owners must consider the asset’s net present value (NPV), internal rate of return (IRR), and return on investment (ROI).

An asset’s economic life can be reduced or ended by several factors. Asset wear, degradation, or damage reduces an asset’s economic life. It lowers asset performance and also raises the costs needed for maintenance and repair.

Asset obsolescence occurs when new innovations and technology replace current ones. It reduces economic life if it raises maintenance costs, and sometimes it ends an asset’s economic life because it renders the asset’s performance inefficient compared to current alternatives.

For example, the widespread use of email replaced faxing and ended the economic life of many fax machines. Lastly, changes in business operations or business models reduce economic life if it affects the value certain assets can deliver to a business.

The concept of economic life is useful for accountants of a company, operators of the asset, and company decision-makers. For accounting purposes, economic life is used as the time period in which depreciation is charged against an asset. Companies use it to allocate depreciation expenses charged for the use of the asset.

Effectively managing assets is the key to economic life. It is also one of the important considerations of a company’s decision-making process to purchase new assets or replace current assets.

By studying and determining when machines, equipment, and other technologies become less effective and uneconomic, companies can effectively plan to replace such assets with new ones at appropriate intervals. The right planning will reduce maintenance and other overhead costs.

For example, in farm businesses, machinery and equipment are major cost items. Owners who make smart decisions about how to acquire machinery, how to properly maintain the machinery, when to trade in old machinery, and how much capital to invest can help to maximize the benefit while reducing the total costs. The economic life of each machine will indicate the number of years over which costs will be allocated.

In such a case, it is usually shorter than the machine’s actual period of usefulness, as most farmers trade machines for newer ones before the old machine is completely worn out. For most farm machines, a 10- to 12-year economic life is a good rule of thumb and 15 years for tractors. At the end of a machine’s economic life, the farmer can either trade it in, sell it, or dispose of it.

Salvage value, the estimate of the sale value of the machine at the end of its economic life, is also always specified. It is the monetary amount the farmer can expect to receive if they trade in the machine for a newer one or if they sell the machine outright at the end of its economic life. The salvage value can be zero if the machine is being kept until it’s worn out completely.

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA®) certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful: