Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Earnings Before Interest & Taxes

Operating income, also referred to as operating profit or Earnings Before Interest & Taxes (EBIT), is the amount of revenue left after deducting the operational direct and indirect costs from sales revenue. It can also be computed using gross income less depreciation, amortization, and operating expenses not directly attributable to the production of goods. Interest expense, interest income, and other non-operational revenue sources are not considered in computing operating income.

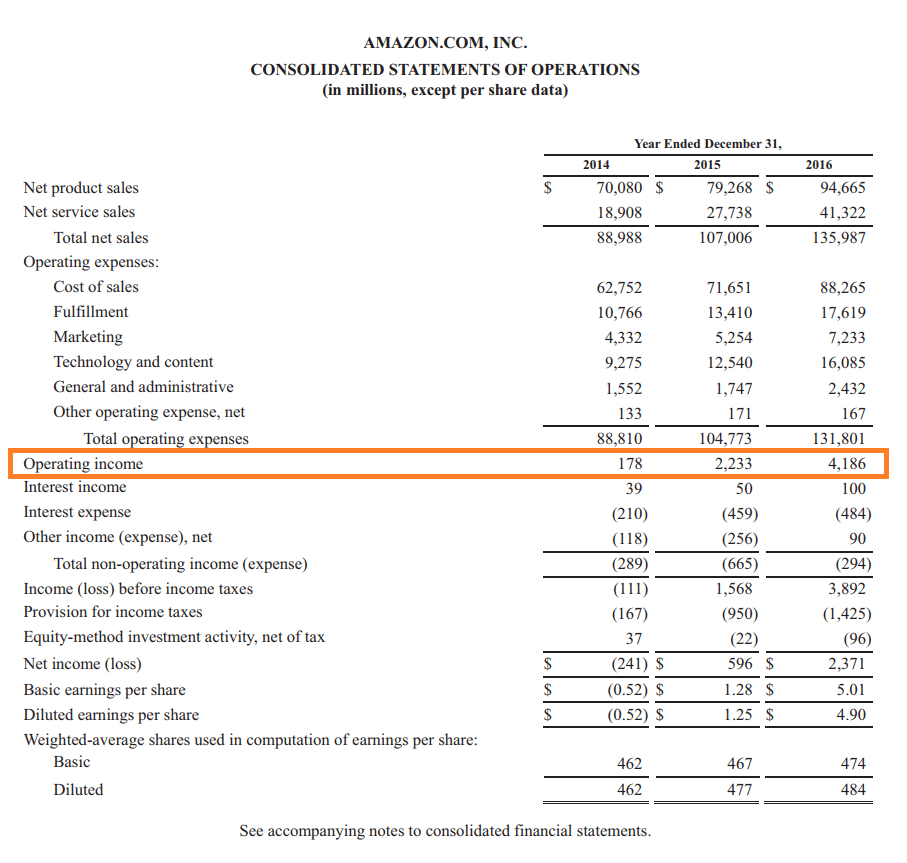

Below is an example of income from operations highlighted on Amazon.com Inc.’s 2016 income statement.

There are three formulas to calculate income from operations:

1. Operating income = Total Revenue – Direct Costs – Indirect Costs

OR

2. Operating income = Gross Profit – Operating Expenses – Depreciation – Amortization

OR

3. Operating income = Net Earnings + Interest Expense + Taxes

ABC Footwear Company earned total sales revenues of $25M for the second quarter of the current year. For that period, the cost of raw materials and supplies used for the sold products was $9M, labor costs directly applied were $2M, administrative and staff salaries totaled $4M, and depreciation and amortization totaled $1M. As a result, the income before taxes derived from operations gave a total amount of $9M in profits.

Sales revenue or net sales is the monetary amount obtained from selling goods and services to business customers, excluding merchandise returned and any allowances/discounts offered to customers. This can be realized either as cash sales or credit sales.

On the other hand, gross profit is the monetary result obtained after deducting the cost of goods sold and sales returns/allowances from total sales revenue.

Direct costs are expenses incurred and attributed to creating or purchasing a product or in offering services. Often regarded as the cost of goods sold or cost of sales, the expenses are specifically related to the cost of producing goods or services. The costs can be fixed or variable but are dependent on the quantity being produced and sold.

Examples of directs costs are:

Indirect costs are operating expenses that are not directly associated with the manufacturing or purchasing of goods for resale. These costs are frequently accumulated into a fixed or overhead cost and allocated to various operational activities.

Examples of indirect costs are:

Examples of selling and administrative indirect costs are:

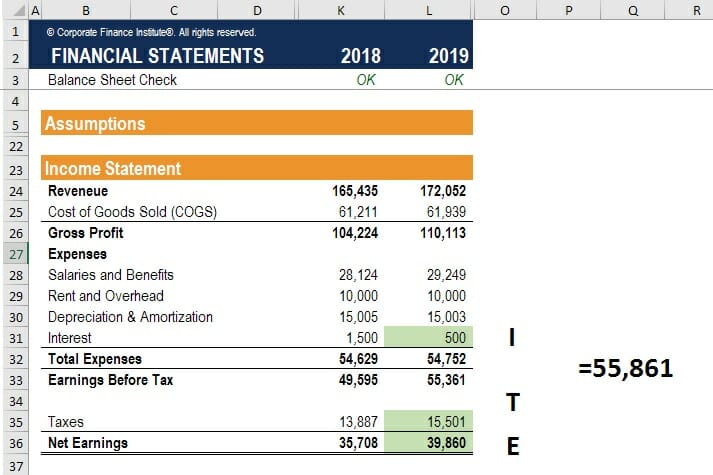

Another way to calculate income from operations is to start at the bottom of the income statement at Net Earnings and then add back interest expense and taxes. This is a common method used by analysts to calculate EBIT, which can then be used for valuation in the EV/EBIT ratio.

Below is an example calculation of EBIT:

Learn more about EBIT and EBITDA here.

Click the button below to download CFI’s free Operating Income template!

Operating income is considered a critical indicator of how efficiently a business is operating. It is an indirect measure of productivity and a company’s ability to generate more earnings, which can then be used to further expand the business. Investors closely monitor operating profit in order to assess the trend of a company’s efficiency over a period of time.

Operating profit, like gross profit and net profit, is a key financial metric used to determine the company’s worth for a potential buyout. The higher the operating profit as time goes by, the more effectively a company’s core business is being carried out.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to Operating Income. If you’re interested in advancing your career in corporate finance, these CFI articles will help you on your way: