Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

A type of mortgage loan where the interest rate remains the same throughout the loan term

A fixed-rate mortgage loan is a type of credit that’s secured by real property; it can be a residential or commercial property. If a mortgage is a fixed-rate mortgage, it means that the borrower (the debtor) and the lender (the creditor) agree to the interest rate ahead of loan disbursement, and that rate will remain the same (hence a fixed-rate) for the duration of the loan term.

When a reducing (or amortizing) loan is extended to a borrower, the expectation is that it will be repaid to zero at some point in the future, after all the payments have been made. The period over which those payments are made is what’s called the amortization period. For example, a mortgage loan might amortize (or reduce) over the course of 25 or 30 years.

A loan’s term can be quite different from a loan’s amortization. For instance, a borrower could take a 25-year mortgage (amortization) but a 5-year or 10-year term. Listed below are some important things to know about a loan term:

Using our 25-year amortization/10-year term example, upon maturity (the end of year 10), the remaining credit outstanding would become a 15-year mortgage loan, but new terms (rate, payment frequency, time to maturity, etc.) would be negotiated based on prevailing market conditions and other competitive forces.

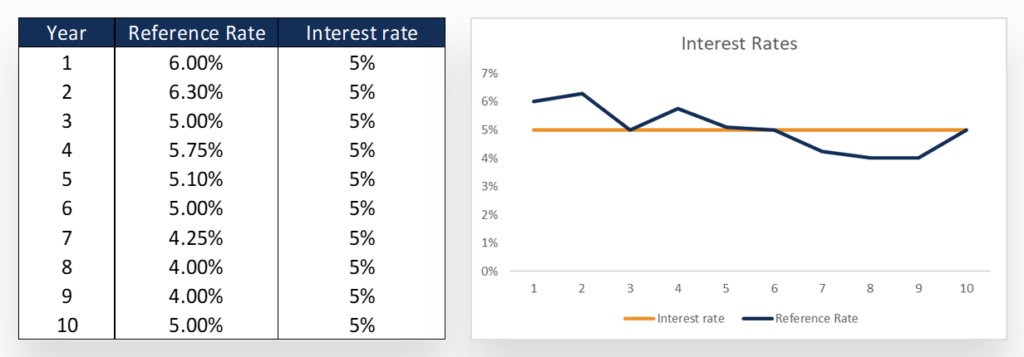

A fixed-rate mortgage loan is one where the interest rate remains fixed for the duration of the loan term, regardless of what goes on in the macroeconomic environment or with a lender’s “reference rates.”

Example: 10-Year Fixed Rate

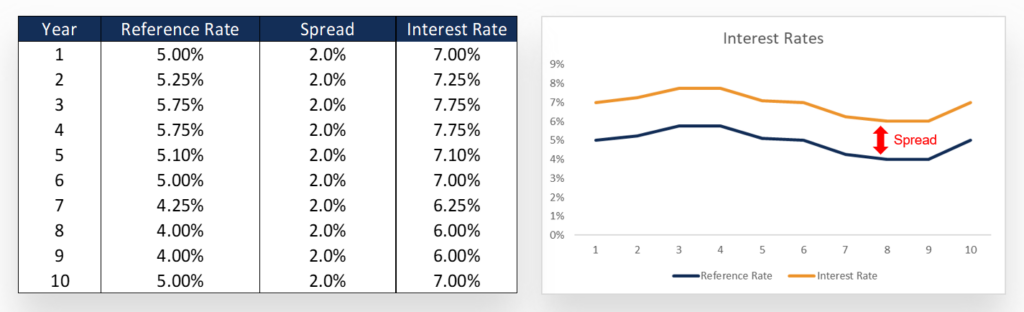

With a variable (sometimes called floating or adjustable) rate loan, the borrower is quoted a spread over a “reference rate” (often called bank “prime”). The borrower’s spread will remain the same throughout the loan term; however, the reference rate is subject to change. The reference rate plus the spread equals a borrower’s “all-in” interest rate.

Example: 10-Year Variable Rate

Reference rates are typically informed by macroeconomic forces and central bank policy; they can change a lot over the course of a 5-year or 10-year loan term.

In all instances, loan structure and pricing (mortgage or otherwise) is a function of two main factors:

All things being equal, a lower-risk borrower is going to get better pricing and will often be permitted to take a longer fixed-rate mortgage term.

Consider two example borrowers, borrower A and borrower B:

Borrower A is an inherently less attractive borrower (from the creditor’s perspective) – students have no income, they tend to be younger (therefore shorter credit history), and in this case, there’s no underlying asset to secure as collateral.

Borrower B is (likely) a high earner, is certainly older (should have a longer credit history), and there is a property to take as collateral. Borrower B is a much more attractive borrower and will likely command a longer fixed-rate mortgage term with better pricing.

Fixed-rate mortgages offer a number of benefits and advantages from a borrower’s perspective. These include, but are not limited to:

However, fixed-rate mortgages also come with some drawbacks. These include:

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to Fixed-Rate Mortgage. To keep learning and developing your knowledge of financial analysis, we highly recommend the additional resources below: