Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The first set of international banking regulations defined by the Basel Committee on Bank Supervision

Basel I refers to a set of international banking regulations created by the Basel Committee on Bank Supervision (BCBS), which is based in Basel, Switzerland. The committee defines the minimum capital requirements for financial institutions, with the primary goal of minimizing credit risk. Basel I is the first set of regulations defined by the BCBS and is a part of what is known as the Basel Accords, which now includes Basel II and Basel III. The accords’ essential purpose is to standardize banking practices all over the world.

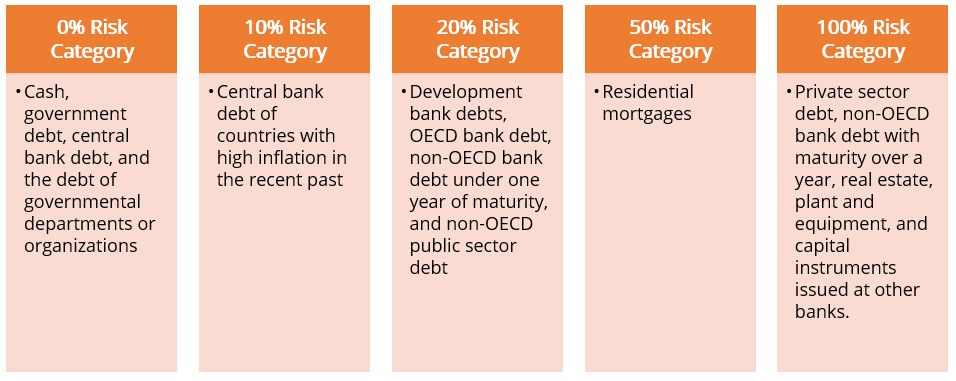

The Bank Asset Classification System classifies a bank’s assets into five risk categories on the basis of a risk percentage: 0%, 10%, 20%, 50%, and 100%. The assets are classified into different categories based on the nature of the debtor, as shown below:

Basel I primarily focuses on credit risk and risk-weighted assets (RWA). It classifies an asset according to the level of risk associated with it. Classifications range from risk-free assets at 0% to risk assessed assets at 100%. The framework requires the minimum capital ratio of capital to RWA for all banks to be at 8%.

Tier 1 capital refers to capital of more permanent nature. It should make up at least 50% of the bank’s total capital base. Tier 2 capital is temporary or fluctuating in nature.

CFI is the official provider of the Financial Modeling and Valuation Analyst (FMVA)™ certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below: