Get Certified for

Financial Planning & Wealth Management Professional (FPWMP®)

Learn financial analysis & planning, portfolio management, and risk assessment.

A credit card perk where the cardholder earns a percentage of eligible spending

Cashback is a credit card perk where a percentage of eligible purchases made on the credit card is paid back to the cardholder. The concept of cashback gained mainstream traction in 1986 when Discover Financial Services, a division of Morgan Stanley, launched a credit card with no annual fees, a higher-than-normal credit limit, and a cashback bonus on certain purchases.

Cashback, effectively a reward or incentive, is primarily used by credit card companies to encourage consumers to make purchases on credit more often. A cashback feature on a credit card allows the cardholder to earn a percentage (typically ranging from 0.25%-5%) of eligible spend. For example, American Express’ SimplyCashTM Preferred Card offers 2% cash back on all purchases.

The following are the most common forms of cashback:

In a few instances, the cashback amount is subject to an annual cap. It is important to read the fine print on your credit card.

Readers should note that some cashback credit cards require a minimum redemption threshold. Again, it is important to read the fine print behind your credit card. Depending on the credit card terms, the cashback is generally redeemed through the following:

Without a doubt, cashback provides cost savings for consumers when they make eligible purchases. However, how does cashback benefit the credit card company?

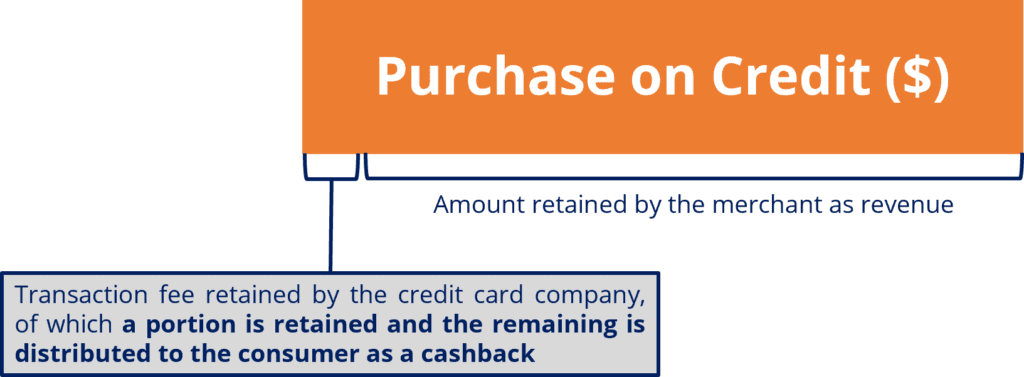

In a cashback transaction, the credit card company would share a portion of the transaction fee (typically around 2%) generated from the merchant with the consumer. This is illustrated below:

Although it may appear that the credit card company is losing money on a cashback transaction, that is not necessarily true. First, it is useful to recall the business model of credit card companies. Credit card companies generate a small transaction fee from merchants when consumers use their credit cards.

As a result, credit card companies provide cashback on their credit cards to incentivize consumers to use their credit card (which generates fees for the company) more often over cash or a debit card (which does not generate fees for the company).

Furthermore, consumers may overspend on their credit cards due to the attractiveness of the cashback, providing greater interest payments for credit card companies from overdue payments. Lastly, credit cards with cashback may have an annual fee, providing additional revenue for credit card companies.

Background Information: Tim is an individual who predominantly pays via debit card or cash over credit card to avoid having to remember to pay off the outstanding credit card balance each month. Recently, He signed up for a credit card solely for the cashback, which is 2% and eligible on all purchases.

Question 1: Over a one-year period, Tim made $15,000 in purchases on the credit card. Assuming a 3% transaction fee charged by the credit card company to merchants, what is the net revenue generated by the credit card company?

Answer: With $15,000 in purchases on the credit card, the transaction fees collected from merchants by the credit card company total $450 ($15,000 x 3%). With a 2% cashback, the credit card company shares $300 ($15,000 x 2%) with Tim, resulting in a net revenue of $150.

Question 2: How has the credit card company benefited from offering Tim cashback on credit card purchases?

Answer: Tim predominantly pays via debit card or cash. As such, by offering a credit card with cashback, the credit card company has incentivized Tim to purchase more on the credit card. As a result, the $15,000 in purchases that would have been made on a debit card or with cash is now on the credit card, generating net revenue of $150 for the credit card company.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

To keep learning and developing your knowledge base, please explore the additional relevant resources below: