Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Financial theory that claims that issuing dividends does not increase a company’s potential profitability or its stock price

Dividend Irrelevance Theory is a financial theory that claims that the issuing of dividends does not increase a company’s potential profitability or its stock price. It suggests that investors are not better off owning shares of companies that issue dividends than shares of those that do not.

As investors buy stocks of a company in hopes of earning profits, stock prices show how profitable investors believe a company will be.

Many internal and external factors affect a company’s stock price. They include:

Some investors believe that issuing dividends increases a company’s share price. However, the dividend irrelevance theory suggests that it is not true.

Conceptually, dividends are irrelevant to the value of a company because paying dividends does not increase a company’s ability to create profit.

When a company creates profit, it obtains more money to reinvest in itself. It can signal to investors that the company now possesses more capital/capability to create more profit and lead to an increase in the company stock price.

However, if the company issues dividends, the company gives money to shareholders that could’ve been reinvested into itself and thereby loses some potential in its profitability.

Implicitly, the company incurs a “cost” by issuing dividends.

Logically, the loss of potential profitability by issuing dividends is equal to the total amount of dividends paid out. Then, the share price of the company will decrease by the amount of the dividend issued.

From the perspective of an investor, issuing dividends doesn’t affect personal wealth.

If the company in which we hold stock issues dividends, an investor’s on-hand cash increases by the amount of the dividend, but the stocks the investor holds are now valued less by the amount of the dividends issued, effectively giving a net gain of $0.

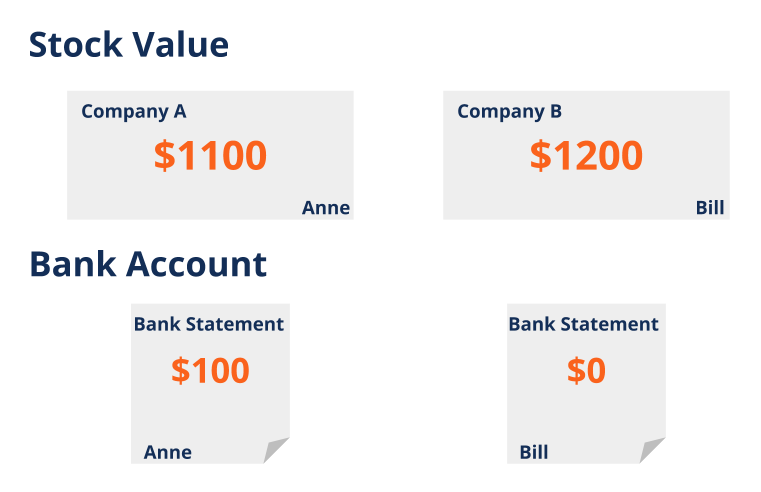

Let there be two identical companies, Company A and Company B. The only difference between them is that Company A issues dividends, and Company B does not.

Each company starts off with a stock price of $10, and one investor, Anne, holds 100 shares of Company A, while another investor, Bill, holds 100 shares of Company B.

Say the two companies perform equally well, and both companies’ share prices increase by $2 and become $12 per share. Anne’s and Bill’s stocks rise in value to $1200.

Now, Company A issues a dividend of $1 per share, whereas Company B does not issue dividends.

With the issue of dividends, Company A’s share price lowers, by the amount of dividend issued, to $11 per share.

With 100 shares, Anne receives a payment of $100.

It is clear that Anne’s total wealth from Company A is $1200 ($1100 in stocks and $100 received in dividends), and Bill’s total wealth from Company A is also $1200 ($1200 all in the form of stocks).

Note that if Bill needs cash on hand, he can opt to sell eight shares (at $12 per share) of Company B to liquidate $96 worth of stocks. Thus, from the investor’s perspective, there is no difference in whether or not a company issues dividends.

Because some investors may wish to receive cash rather than to hold shares (possibly due to a feeling of security from cash), there can be an intrinsic demand for stocks of such companies.

However, the demand does not reflect potential profitability. It simply shows that certain investors are predisposed to buy dividend-paying stocks for reasons unrelated to rigorous financial analysis.

Commitments to paying large dividends in the long term may decrease the potential profitability of a company. As a company continuously issues large dividends, it implicitly loses funds to create future profits.

Over time, dividends issued can add up, and the loss of a large sum of operational cash can compel the company to take on debt or be unable to implement a profitable strategy.

In turn, high proportions of corporate debt or failure to implement a good strategy when opportune can lower investor confidence, which then leads to lower share prices and ultimately decreases company profitability.

CFI offers the Financial Modeling & Valuation Analyst (FMVA®) certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following resources will be helpful: